Lex20/iStock via Getty Images

The effects of climate change can be seen in many different ways and to name a few, it affects our food supply through extreme weather and leads to power outages. Generac Holdings Inc. (NYSE:GNRC) can use this catalyst as an opportunity to grow further, making it well-positioned to capitalize on today’s mega-trend in climate change.

I wrote about GNRC in April 2021 when the stock was just trading around $320 and materialized to hit an all-time high of $524ish that year. Upon revisiting this stock, GNRC is heavily beaten by the market, but the good thing is that it remains fundamentally strong, which unlocks a good buy opportunity today.

Pressured Residential Products

One of the problems I see is fear from GNRC’s slowing residential products growth.

GNRC: Slowing Growth On Its Residential Product (Source: Company Filings. Prepared by InvestOhTrader. Amounts are in millions)

Considering today’s tightening consumer budget due to rising inflation and no material government stimulus check to spend, this could explain GNRC’s slowing growth. However, as shown in the image above, it has improved sequentially for the third consecutive quarter, indicating some recovery, making this stock more appealing.

Pressured Margin

GNRC: Pressured Operating Margin Trend (Source: Data from SeekingAlpha. Prepared by InvestOhTrader)

GNRC was beaten up due to its slowing margin; inflationary pressures and shortages snowballed into 5 consecutive quarters of declining operating margin from Q1 2021 to Q1 2022. However, this quarter, it generated a better figure on a quarter-over-quarter basis, making this stock attractive again in light of its continued margin recovery, as shown in the image above.

Powering a Smarter World

After a few months since my last analysis on GNRC, it has since entered into numerous acquisitions. To name a few, the company acquired a controller manufacturer, Deep Sea, in June 2022; Chilicon, a leading grid-interactive microinverter, in July 2021; Off Grid Energy in September 2021; ecobee Inc., a leading smart home solutions provider, in December 2021; and recently, Electronic Environments Co. LLC, an industrial generator provider and expert in telecom and IT infrastructure, in June 2022.

These acquisitions helped GNRC grow its top line, as mentioned before. However, on top of the supply shortages and inflationary pressure, the company seems to have a problem integrating its acquisition, as shown in its slowing operating margin. This is visible in its rising total operating expense ratio, as shown in the image below.

GNRC: Rising Total Expense Ratio (Source: Data from SeekingAlpha. Prepared by InvestOhTrader)

This is probably an aggressive move for the company, especially with today’s uncertainties; however, these acquisitions and continued capacity expansion make me believe that GNRC is still well-positioned for a positive recovery in the next few years.

Additionally, it continues to seek opportunities in natural gas generators and control systems through partnerships, enhancing its Commercial & Industrial capabilities. As part of “Powering a Smarter World,” GNRC has robust human resource growth. According to the management, they have around 10,000 employees globally with 8,200 residential dealer partners, which can support its growing demand. Lastly, despite the aggressive acquisition, the company maintained a healthy capital structure and produced an improving debt-to-equity ratio of 0.62x, which is lower than its 5-year average of 0.93x.

Growing SAM

GNRC has been growing steadily over the years, and thanks to its multiple acquisitions, it now has a growing addressable market estimated to grow to $72 billion in 2025. According to the management, the growth comes mainly from clean energy and the continued trend toward electrification of everything.

The management also saw continued growth from its home standby generator. According to them, in 2021, their penetration rate is just about 5.5% of the total addressable market of homes in the US.

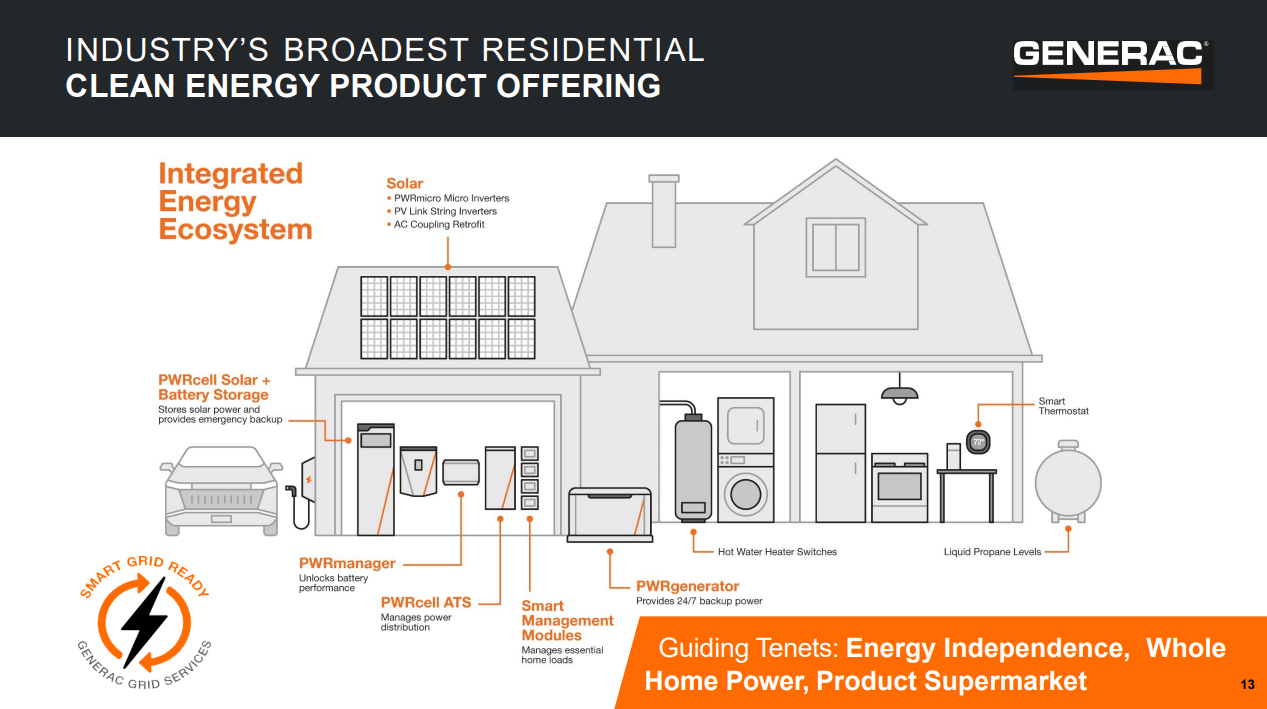

I believe the company can drive penetration further, especially with its improving capacity and boosts from the Inflation Reduction Act, where U.S. residents can be eligible for solar tax credits for installing solar panels. In fact, according to the management, GNRC has the industry’s broadest residential clean energy portfolio.

GNRC: Residential Clean Energy Product Portfolio (Source: Company’s Investor Presentation)

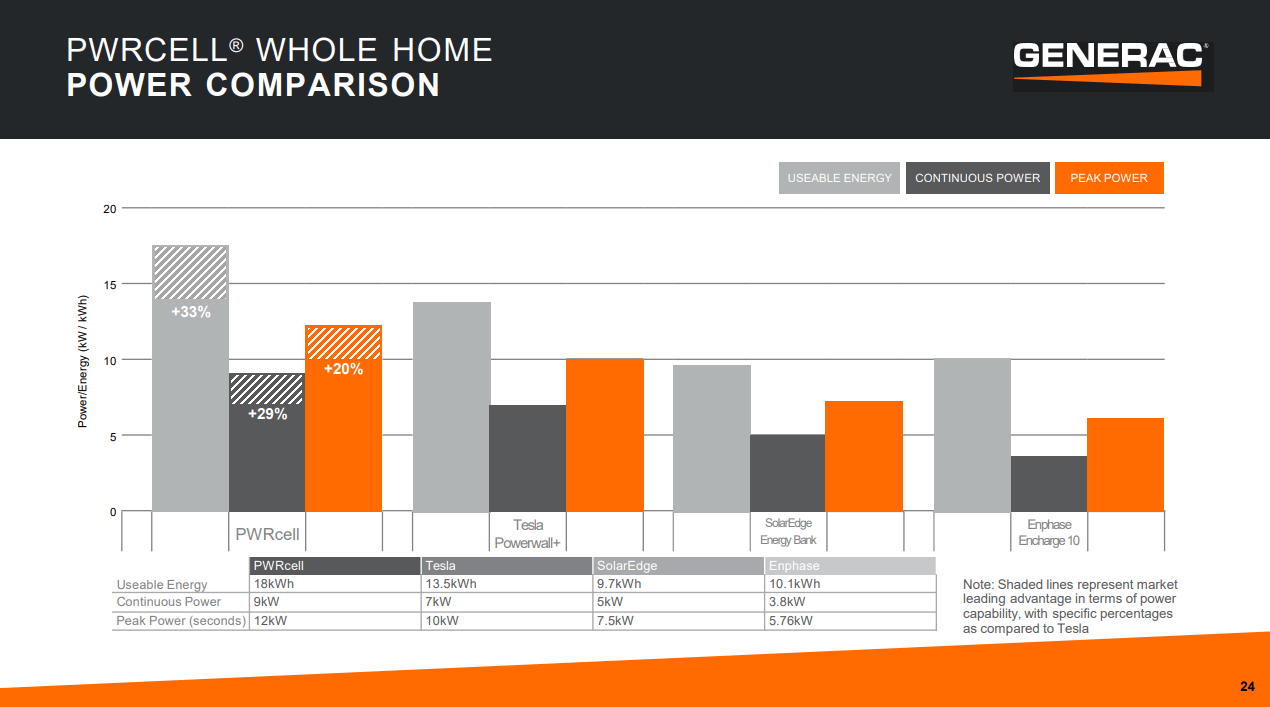

In fact, according to the management, they have more capacity and are more efficient than their peers.

GNRC: Better PWRCELL (Source: Company’s Investor Presentation)

Tesla, Inc. (NASDAQ:TSLA), SolarEdge Technologies, Inc. (NASDAQ:SEDG), Enphase Energy, Inc. (NASDAQ:ENPH).

Undervalued

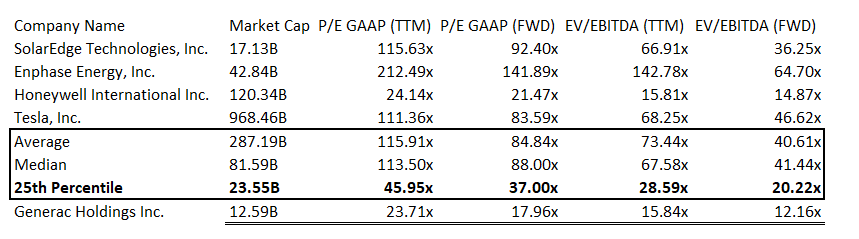

GNRC: Relative Valuation (Source: Data from SeekingAlpha. Prepared by InvestOhTrader)

Tesla, Inc., SolarEdge Technologies, Inc., Enphase Energy, Inc., Honeywell International Inc. (HON).

GNRC remains undervalued and trades at an improving P/E multiple of 23.71x, which is now below its 31.22x 5 year average. By excluding GNRC from the first quartile computation to arrive at a more conservative figure, as shown in the image above, we can see that it is undervalued compared to its peers in the residential power space. GNRC trades at appealing earnings multiples that are undervalued in comparison to its historical figure of 31.22x and its peers’ multiple of 45.95x.

GNRC is currently trading below the low target price of $256 set by the Street. I believe this is still conservative in light of its improving SAM outlook and analysts’ projection of $18.11 EPS in FY25.

Trading At Support

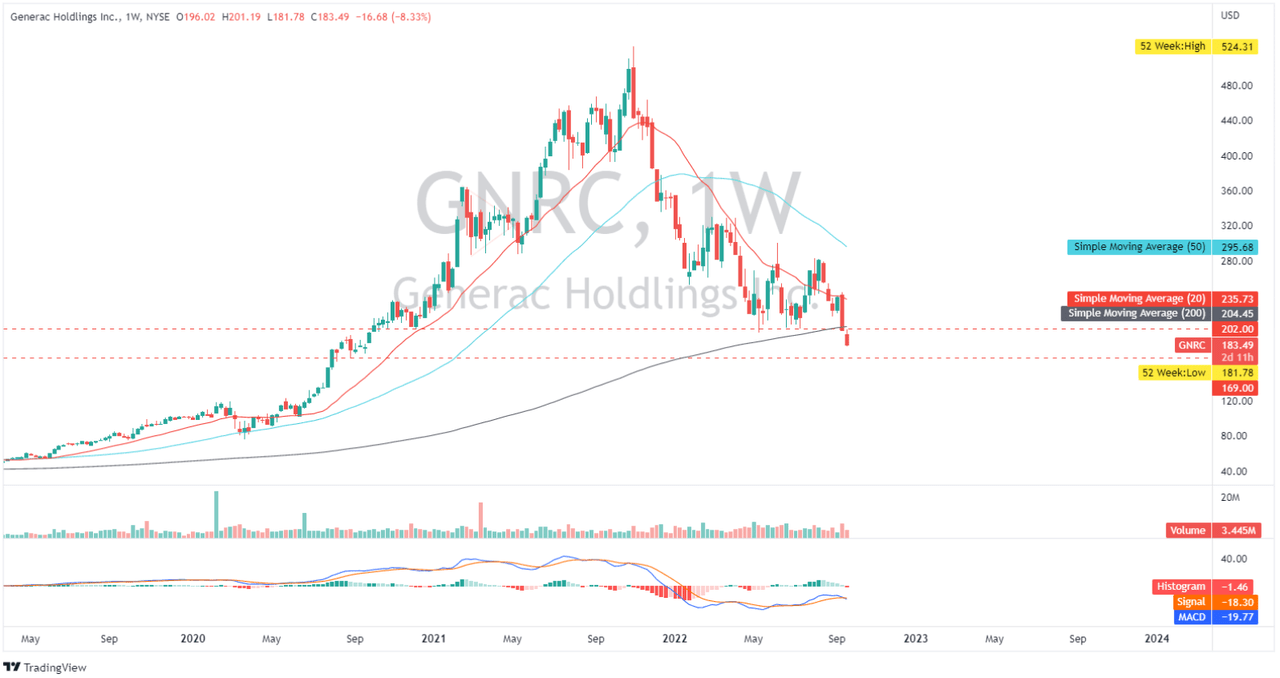

GNRC: Weekly Chart (Source: TradingView.com)

GNRC recently broke its 200-day simple moving average, which serves as supposedly a strong support, in conjunction with its bearish sentiment from its MACD indicator, which crossed below its signal line. As a result, we may see continued bearish pressure, forcing the stock to retest its next support level around $140.

However, I believe that with its improving margins and SAM outlook, we may see a reduction in bearish pressure in the coming quarter. As a result, consolidation in this area in the coming weeks may provide a good entry point.

Conclusive Thoughts

GNRC ended its 2nd quarter with robust top-line Y/Y growth of 40.37% to $1,291.4 million, up from $920 million. As quoted below, its gross margin is starting to improve, especially considering the outlook from the management for 2022.

But as our prepared comments said, if — we posted 35.4% gross margin in Q2. Expect them to get closer to 40% by the end of the year. As we ramp that, what is that, 4% to 5% increase, about half of that sequential increase will be about — half of that will be pricing, price realization continuing to come through, the other half being moderation of input costs.

When you look at commodities starting to roll over, we’ll start — we’ll see the lagging impact of that. There’s always a lag in our realization. As commodities move, there’s always a lag. We’ll start seeing some of that here in the latter part of the year. We’re seeing inbound freight costs come down. Some of our expediting costs are coming down. Just getting our plants’ absorption improve. We do have a number of just cost-out projects. We’re working on our build and material of our products that will materialize in the second half. Source: Q2 Earnings Call Transcript

Even though inflationary pressures may strain GNRC’s residential product demand and disrupt its margin recovery, I believe H2 2022 will be interesting if they can convert their anticipated moderating input cost into margin recovery. To summarize, I believe GNRC is still fundamentally sound, and the recent fear-driven drop improves the risk/reward ratio, making this stock a good buy today.

Good Luck!

Be the first to comment