josefkubes

Introduction

GE HealthCare (NASDAQ:GEHC) is a leading supplier of equipment, tools, and services for the healthcare industry. In fact, the company holds a moat over the medical imaging and ultrasound markets, a sort of oligopoly with Siemens Healthineers (OTCPK:SMMNY) and Philips (PHG). Due to market leadership, GEHC sees high profitability and organic growth, despite the lack of TAM expansion. One factor investors must consider is that the industry is only just rebounding after pandemic headwinds, and valuations are rising. However, it is expected for growth to remain strong even if a recessionary environment forms.

With the IPO on Jan 4th, 2023, the shares rose 8% reaching a $27.5 billion market cap, or 1.5x sales. Some may call that overvalued, others not, but more on the financials later. For now, I believe GEHC is a great company worthy of consideration, but patience is a viable strategy for investors with or without currently owning shares. If anything, I would only make small purchases on a recurring basis, but hesitate to make a full lump sum investment. However, that depends on the investment expectations of each investor. Instead, this article will summarize the key qualitative and quantitative factors of GEHC, compare recent performance to peers, and share my expectations for the coming years.

Four Strong Revenue Segments

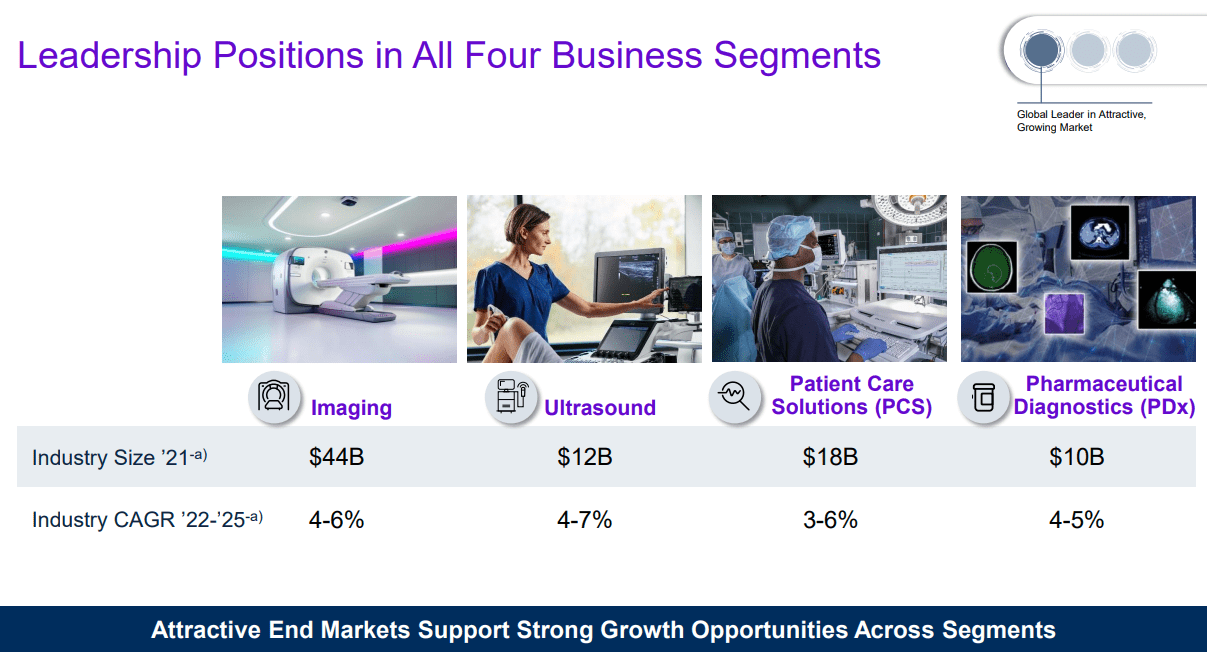

For any multi-billion company, having diverse revenue segments is the key to providing long-term success. For GEHC, this relies on four main business segments: Imaging, products and services related to MRI, CT, PET, and other large imaging machines; Ultrasound, products and services related to sonic imaging equipment, services, and software; Patient Care Solutions, products and services related to patient monitoring such as surgical visualization instruments, vital sign monitors, and anesthesia delivery; and Pharmaceutical Diagnostics (PDx), the development, sale, and manufacture of the imaging agents required for the three other segments.

Due to saturation of the market, organic growth relies on the underlying growth trend of each sub-industry. The segments are set to grow in the mid-single digits thanks to trends in aging populations, access to healthcare, and rising disease incidence. Also, investors should consider the fact that healthcare revenues are typically quite recession agnostic, and this limits the downside growth potential. Per the University of Illinois Chicago press:

‘A lot of this differential employment response likely occurs because many health needs are not tied to economic conditions and because the federal government pays for a lot of health care,’ said SPH’s Marcus Dillender, PhD, assistant professor of health policy and administration and a co-author on the study. ‘This helps compensate for any decrease in demand that might occur from people losing health insurance through an employer during a recession.’

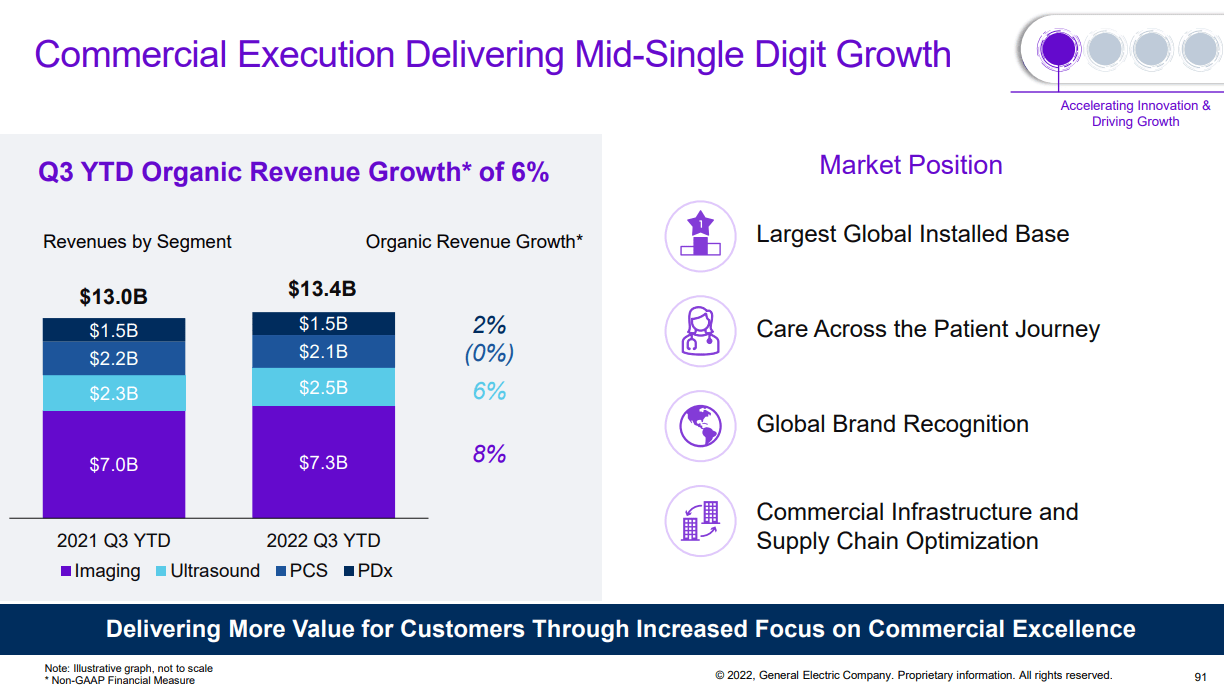

For the pandemic environment, the main issues are that labor shortages (either due to staff taking care of COVID patients or general staffing shortages) have led to reduced growth in GEHC segments. Thankfully, almost 50% of all GEHC revenues are recurring or service based, and this provides stability despite headwinds.

The pandemic issues are reflected as ~3% organic revenue growth between 2019 and 2021. This is quite low, particularly when comparing to GE historical data, and I expect a rebound over the coming years However, temporary issues with a strong USD will continue to hamper overall growth of this US-based globally operating company. Do not be surprised if baseline revenue growth is negative or in the low-single digits over the coming quarters (although inorganic growth through acquisitions and investments can lead to my expectations to be beat). Just be sure to note these issues as temporary.

GEHC Investor Presentation GEHC Investor Presentation

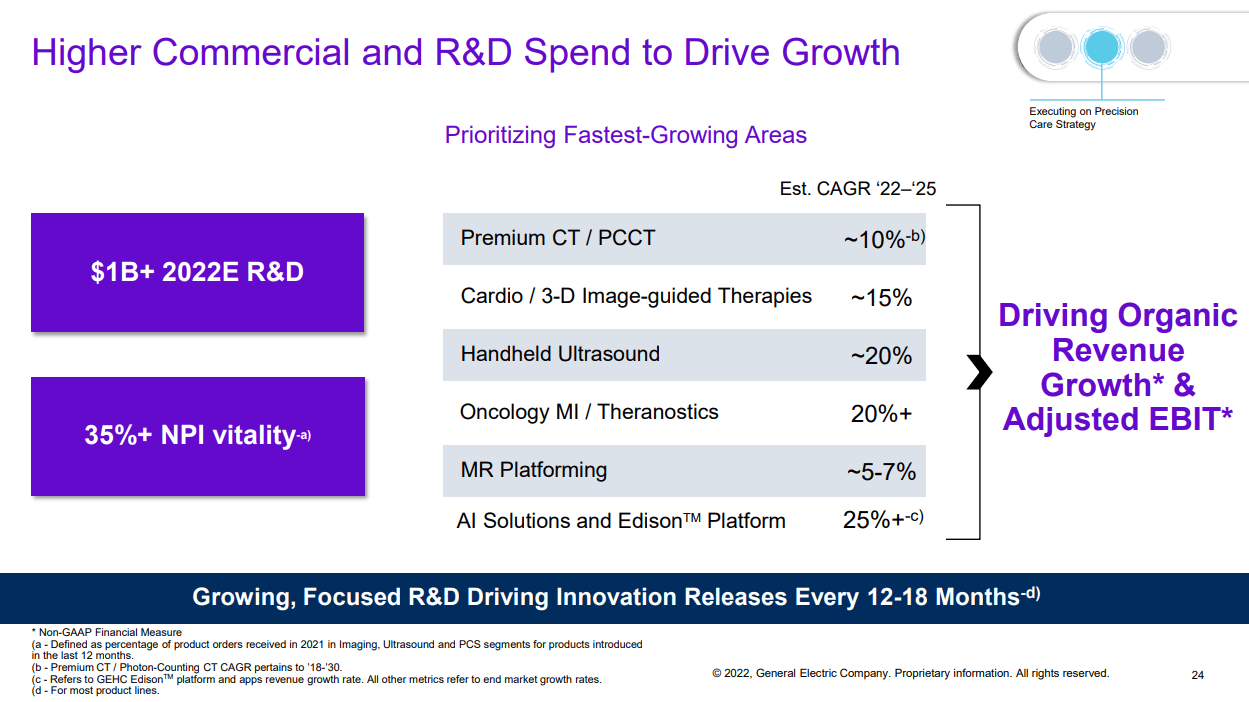

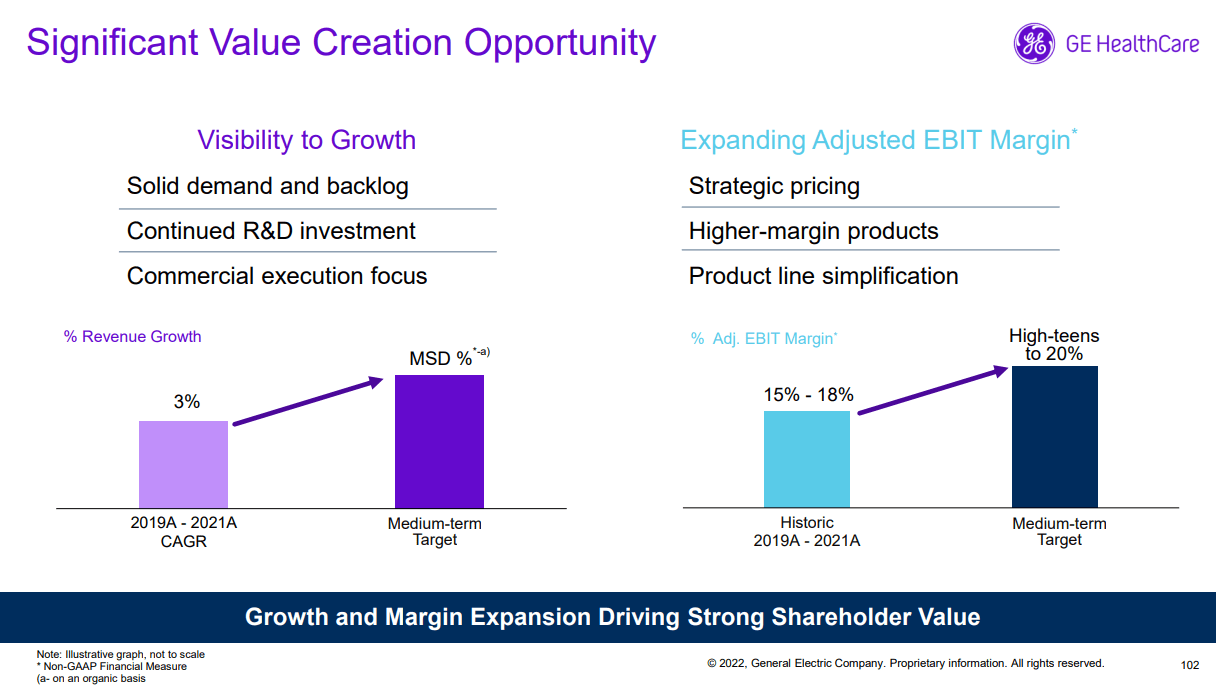

One of the benefits of being a mature company is strong profitability. By generating large amounts of cash, a strong management team should be able to invest heavily in R&D to drive growth. Between 2019 and 2021, GEHC had an average Adjusted EBIT margin of 15-18% and the company invested over $3 billion in R&D. Over the past 12 months, total R&D spending totaled 5.4% of revenues. As discussed in the image below, these profits are being pushed into significant growth markets and this is the key reason why I believe organic growth will be maintained over the coming years.

Some intriguing growth opportunities lie in the development of AI/ML-based software integrations for the medical equipment to increase the efficacy, quality, and usability of the products. This will have a positive feedback effect on sales across all segments as the usage of imaging, ultrasound, and patient care devices increases. Also, outside factors such as the growth in oncology treatments and diagnostics supports increased device usage, as long as the devices are accurate enough. If healthcare enters a strong enough bull market, I expect total returns in the next cycle will be strong thanks to rapid earnings growth. The question now is whether GE HealthCare can outperform peers.

GEHC Investor Presentation

GEHC Investor Presentation

Competitors

As discussed previously, Phillips and Siemens are the dominant players in GEHC’s segments. Other smaller competitors include Canon (CAJ), FujiFilm (OTCPK:FUJIY), and Samsung (OTCPK:SSNLF). Below, I summarize the financials of each competitor to determine whether GEHC offers any advantage. It is also important to note that not all competitors overlap all business segments, and names such as Canon and FujiFilm have diversification in other areas of the market. Also, Philips is facing some issues from a respirator recall that is causing delays in shipments as they resend non-defective equipment back to customers.

GEHC

-

YoY Revenue Growth (%): 1.53

-

TTM EBIT Margin (%): 13.8

-

R&D/Revenues (%): 5.4

-

TTM P/S: 1.52

Siemens Healthineers

-

YoY Revenue Growth (%): 20.65

-

TTM EBIT Margin (%): 13.47

-

R&D/Revenues (%): 8.79

-

TTM P/S: 2.62

Philips

-

YoY Revenue Growth (%): -11.8

-

TTM EBIT Margin (%): 0.40

-

R&D/Revenues (%): 13.7

-

TTM P/S: 0.81

FujiFilm

-

YoY Revenue Growth (%): 17.1

-

TTM EBIT Margin (%): 13.9

-

R&D/Revenues (%): 5.6

-

TTM P/S: 1.10x

Canon

-

YoY Revenue Growth (%): 9.31

-

TTM EBIT (%): 6.1%

-

R&D/Revenues (%): 7.77

-

TTM P/S: 0.85

As shown, GE is trading at a fair valuation right now based on growth and R&D investments. GE is also just as profitable as the top peers Siemens and FujiFilm. The variation in revenue performance and valuation can be attributed to forex rates suppressing headline numbers, but not constant currency growth. However, this means that FujiFilm looks like the best value of the group if considering an investment right now, especially when combined with their higher growth CDMO business. Therefore, I prefer FujiFilm as a current investment but GE HealthCare will remain on my watchlist. But, not all investors favor a growth orientation, so a more defensive bet into GEHC may perform well.

Conclusion

While GEHC is facing some headwinds due to lingering pandemic effects and unfavorable foreign exchange rates, the business fundamentals are solid. The problem is that the current valuation is a little full, and I would rather take two paths: 1.) either believe that GEHC is fairly valued and slowly begin adding shares, or 2.) wait for the valuation to fall. For me, it is the latter as I wait for the USD to weaken. But for many, this may be a great time to add a stalwart.

Before 2023, I would have believed it possible to wait for shares to fall, but as I discussed in an article on spinoffs, strong SpinCos still have a chance to outperform. With GEHC strong fundamentally, and the healthcare industry currently acting like a safe haven for investors, I expect downward pressure is weak. I will remain on the sidelines and provide updates as necessary.

Thanks for reading.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment