piranka

GDS Holdings (NASDAQ:GDS), the market leader in China’s carrier-neutral data center market, suffered a major drawdown in 2022 alongside the rest of the Chinese equity universe. Things are looking up this year, though, as tailwinds from the post-COVID reopening in China and an accelerated expansion into Southeast Asia leave GDS well-positioned for future beat-and-raise quarters.

Over the mid to long-term, the thesis on GDS remains intact, in my view. The company continues to have a massive footprint and pipeline in key cities, having built relationships with all the major Chinese cloud players (e.g., Alibaba (BABA) and Tencent (OTCPK:TCEHY)). Ongoing diversification efforts beyond China and the customer mix shift away from the public cloud service provider vertical should yield earnings upside as well.

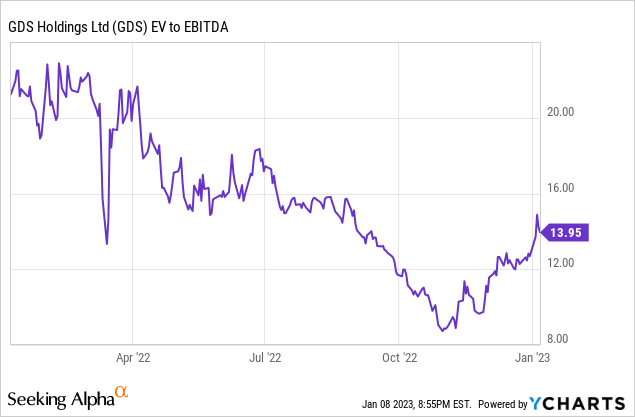

That said, the valuation is a hurdle – following the re-rating from last year’s lows, the stock now trades at ~14x EV/EBITDA despite still being a long way from breakeven. Net, I am neutral at these levels.

China Reopening to Catalyze a Recovery

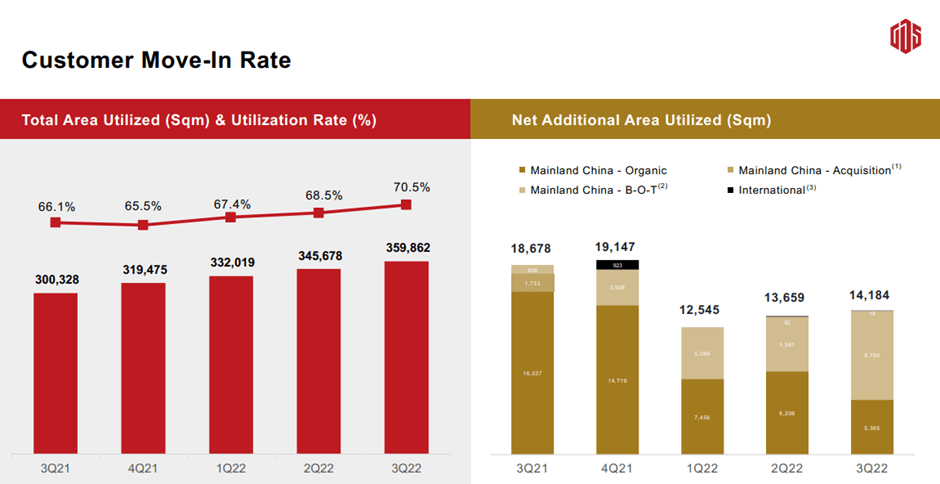

The reopening in China over the last month or so is set to be a game-changer for data usage, not only for general use but also at the enterprise level. For GDS, business as usual means a re-acceleration in cloud computation and enterprise digitalization initiatives, in turn driving data center capacity demand. The good news is that GDS has enough existing capacity to capitalize on a demand recovery – per management, the current utilization rate is running at ~70%, which implies >100k sqm available for move-in (vs. the ~70k sqm FY22 target). With Chinese New Year promotions offering an additional tailwind this month, all signs point toward a ramp-up in capacity demand sooner rather than later.

GDS Holdings

While the prospect of a demand recovery is a key positive, GDS isn’t entirely out of the woods yet. For one, reports indicate COVID cases in China are at record levels, which could mean unforeseen near-term disruptions before the sector gets back on track. So while the stock has reacted positively to the reopening news, a more realistic timing for an earnings recovery is in the back half of the year. That said, positive announcements in the meantime could catalyze upside; for instance, a reversal from GDS’ prior decision in Q3 to delay ~59k sqm of capacity (previously scheduled for 2022/2023 delivery).

Accelerating the South-East Asia Expansion

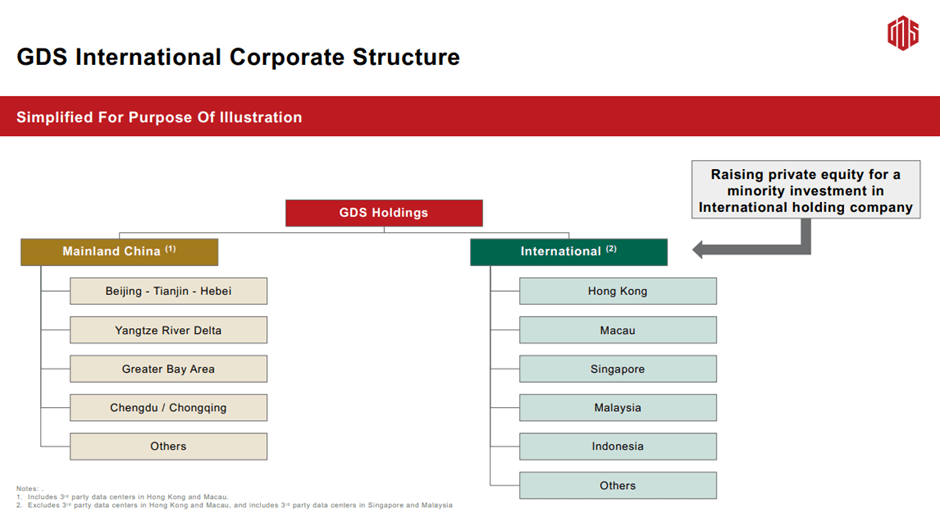

The Chinese data center market is not as attractive as it used to be amid rising competition and weaker growth from the major cloud service customers. As a result, GDS has refocused its expansion efforts away from its dependence on the China public cloud space. One key initiative is its accelerated venture into the higher-growth South-East Asia market.

To capitalize on the regional expansion opportunity, GDS plans to raise private equity funding via a new holding company, which will house all the ex-China data center assets. Thus far, the company has closed on a subscription agreement with a key sovereign wealth fund backer but has yet to clear antitrust approval in China. While the complexity of this deal could mean a post-Q1 2023 close (as guided by management) as various agreements still need to be finalized, a successful outcome bodes well for the long-term growth outlook.

GDS Holdings

In the meantime, GDS has already taken a significant step to building out capacity in the region via Nusajaya Tech Park in Malaysia following a major ~64MW order win from a Chinese hyperscaler. Equinix (EQIX) subsequently followed up with its entry into the market via capacity in Nusajaya Tech Park as well, so the regional ramp-up won’t be straightforward from a competition standpoint.

Given its recently raised capex guidance for the international business at RMB4bn in FY23 (double the RMB2bn in FY22), though, management clearly sees an in-line (if not better) return potential for South-East Asia data center projects vs. China. GDS’ ability to leverage its Chinese relationships is a key strength, as it continues to serve as the first port of call for the growing number of China customers taking up capacity in the region.

GDS Holdings

Managing the Near-Term Churn is Key

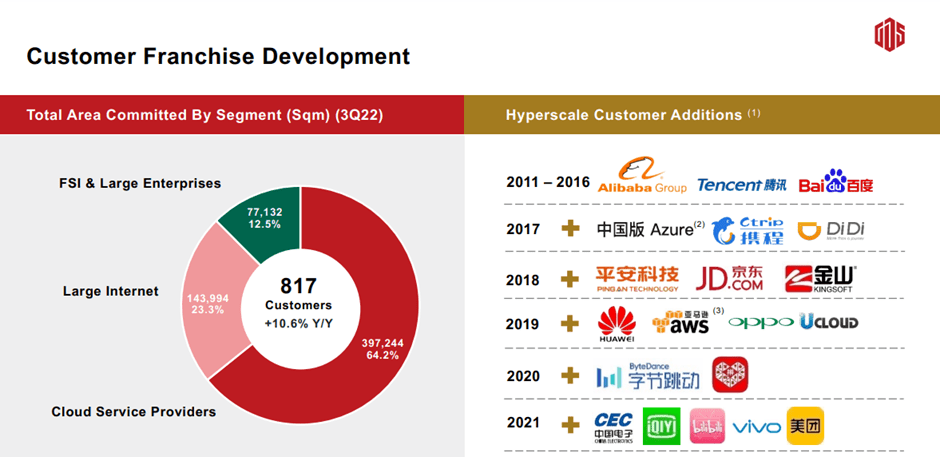

In the upcoming quarters, GDS will need to manage ~80k sqm coming up for renewal. Of the total, ~17k sqm is to be incurred in Q4 2022/H1 2023 across tier-1 locations related to a data center migration from a major tech customer. On an annualized basis, the revenue impact is sized at ~RMB450m, which at 4-5% of FY22 guidance, isn’t a game-changer. Instead, management cited the churn as temporary on the Q3 call and expects financial institution deals to fill up capacity in the coming months. As for the remaining space, the majority of the churn capacity (around half) is slated for relocation to GDS’ other sites, so I see minimal impact beyond the near term.

More importantly, the upcoming churn event gives GDS an opportunity to rebalance its customer profile. Relative to the >60% of capacity currently committed to cloud service providers, a shift toward financial institutions and other large enterprises (currently in the low-teens %) would be positive for the P&L.

GDS Holdings

Reopening Tailwind Likely Priced In

Fundamentally, there is a lot to like about GDS. The company’s footprint and pipeline in key Chinese cities represent key competitive advantages, along with its relationships with all the major cloud players in China. While demand headwinds from cloud services clients (currently GDS’ biggest client share) have weighed over the last year, efforts to diversify the base across higher-growth/margin verticals like financial institutions and other enterprises should cover any shortfall.

In the near term, the China reopening will be a key catalyst, along with progress on the planned expansion into South-East Asia. With the stock already up to ~14x EBITDA, though, much of the positives have likely been priced in; I see a balanced risk/reward for GDS at these levels.

Be the first to comment