VeselovaElena/iStock via Getty Images

By Rob Isbitts

Strategy

Alpha Architect Gdsdn Dynmc Mlt-Asst ETF (BATS:GDMA) is an actively-managed asset allocation ETF. As its name suggests, it allocates “dynamically” to a wide variety of other ETFs. That is, it will not sit still when its managers believe that the portfolio can benefit from rotating from one market segment to another. The fund has no benchmark, as its objective is essentially to make money and manage risk.

Proprietary ETF Grades

-

Offense/Defense:Offense

-

Segment:Tactical

-

Sub-Segment:Allocation

- Risk (vs. S&P 500): Low

Proprietary Technical Ratings

-

Short-Term (next 3 months): Sell

-

Long-Term (next 12 months): Sell

Holding Analysis

GDMA holds about 15-20 ETFs at a time, and will supplement those ETFs with small positions in individual stocks. The current stock positions are focused in the energy sector, and each position is around 1% of the portfolio. Among the main ETF holdings, which comprise 80% of more of the ETF, GDMA currently owns a very large position in a T-Bill ETF, and decent-sized holdings in a TIPS ETF and several inverse equity ETFs. There is a decided cash-commodities-stock bear market bent. However, as is the case with a fund like this that turns its holdings over at a rate of more than 200% a year (which implies an average holding period of 4 months), the next time we visit GDMA, the holdings allocation will likely be quite different.

Strengths

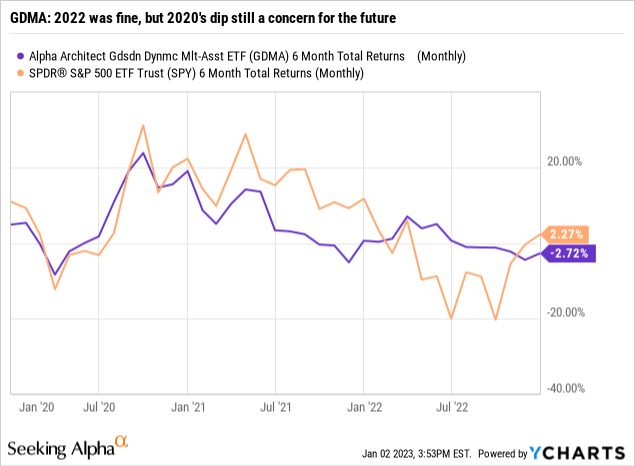

When I first started to look at this ETF, I was on my way to making a strong case for it. Frankly, I was excited. GDMA has a lot going for it. Unlike most ETFs that “allocate” assets, this one throws shade to the traditional stock-bond paradigm. It allocates via ETFs to whatever market segment it darn pleases. I like that flexibility and willingness to rotate tactically with rapidly-changing market conditions. That’s why GDMA was able to post a total return of about -2.1% in 2022. That’s “rockstar” level performance for an actively managed ETF, and I applaud them for it.

If it sounds like I know a bit about what they are trying to do with GDMA, it is because I did it, and continue to, albeit in a different form. I managed one of the first “alternative” mutual funds back in 2008, survived that chaos, and again sat in the lead-fund-manager’s seat in 2016 for a few years. In both cases, the approach I used to run those mutual funds is philosophically similar to GDMA. So naturally, I am enamored with the broad approach here.

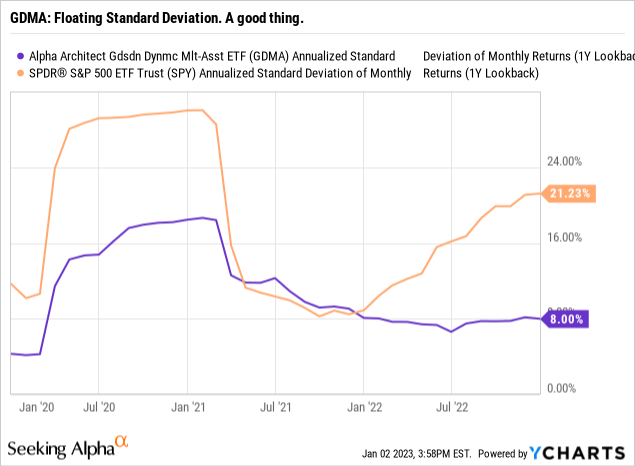

The chart above shows what that flexibility can do for an ETF at a time of high market volatility and a changing regime in the bond market. Standard Deviation is a valuable way to look at active ETFs for 2 primary reasons:

1. It captures the past range of returns in a single statistic

2. That standard deviation, plus this historical annual return over the same period, can be extrapolated to estimate what the security might do looking forward. Nothing can tell us precisely how an ETF will perform. But if you know that the manager can proactively drop its Standard Deviation from about 18% to just 8%, it indicates that they are attempting to control risk. As you can see, the SPY ETF’s Standard Deviation dipped as well, but since that is an unmanaged index, when that index caved in during 2022, the range of returns and Standard Deviation exploded higher once again. Bottom line to me: risk-management is a valuable tool in this market climate, and GDMA appears willing to do that.

Weaknesses

Oh, but there are cons to those pros on GDMA, much to my temporary disappointment. I say temporary for 2 reasons: the assumptions I make below are based on my research, and while I think my facts and opinions are well-founded, I am the first to admit if I was wrong. After all, when you’ve managed money professionally for decades, you get used to being wrong a lot! The key is to use each situation to get better.

GDMA has only been around for 4 years. Thus, it has not been stress-tested as much as some other ETFs we might compare it to. I looked through the fund’s site as well as the prospectus for the ETF, hoping to find a track record for the strategy used in GDMA, but from before it was an ETF. This was exactly what I went through twice, as noted above, when I managed mutual funds. My firm had a documented past performance record using live accounts we had managed (in what is referred to as a “performance composite”). And, while that record was not for the managed fund itself, it was a close enough clone, strategically-speaking, so that prospective fund investors could see what we’d done in the past, before the existence of the fund, and make their own judgements as to whether that extended track record was useful.

GDMA might have a composite track record for this approach from before the ETF’s 11/14/2018 inception date. But if it does, it is hard to find. So we do have a 4-year record for GDMA. That means that we have to focus on what happened during 2020’s market debacle, as the S&P 500 fell 33% in 5 weeks. Sure, it recovered quickly, but to assume that will happen each time, or even the next time, is foolish and dangerous.

During the 5-week stock market mess from 2/19/20 through 3/23/20, GDMA fell by about 16%. That is certainly better than the S&P 500 by quite a margin. However, it was not much different from a 40/60 (40% stock/60% bond) allocation during that time. And most importantly, 16% is beyond what many risk-intolerant investors can reasonably take before making emotional decisions. Thus, GDMA has some proving to do.

It did a lot of that in 2022, when its return spent the entire year within a few percent either side of zero return. That’s an outstanding accomplishment, and I suspect that the energy exposure and short-stock market exposure were the drivers. The question is: was 2022 about the managers learning from what happened in 2020, or something else? My conclusion: this ETF has a lot of potential. But the sample size to evaluate whether these active managers can truly manage risk is small. So, the jury’s still out, so to speak.

Opportunities

GDMA could very well be the right ETF at the right time. The managers have the flexibility to use inverse ETFs, one of my long-time favorite tools. They don’t use leverage and don’t mind piling a chunk of assets into cash at a time like now, when T-Bills offer a great reward/risk tradeoff relative to the stock and bond markets. It all shapes up to 2023 being a key year for GDMA.

Threats

OK, now for some esoteric, but real concerns about GDMA. These have nothing to do with strategy and manager execution of that strategy. Rather, they deal with some pesky issues that, as a former long time licensed investment advisor representative and fiduciary (27 years), irk me a bit. They may not irk most investors. But I can’t heap all of the praise above without at least mentioning these.

The first one is, admittedly, a bit nit-picky. The ETFs’ prospectus states that “The Fund is actively managed and does not seek to replicate a specified index. The Fund returns may not match the return of the respective index.” Maybe it is my decades of scouring information sources like this, but an ETF that doesn’t have an index should not have a prospectus that refers to an index. I like the benchmark-less nature of GDMA, but that no one has caught that inconsistent language opens the door to the question, “is this ETF being run carefully enough.” Recall that GDMA did not protect capital in 2020 the way one would hope from an ETF that has all the flexibility this one does.

The ETF’s website also indicates that it has a “Factsheet” but when you click on the link, it says it is “coming soon.” This ETF is more than 4 years old. So that just adds to the nagging issues I spotted in my research.

Finally, the big one, at least to me. This is from the Form ADV of the investment advisory firm (Almanack) that works with individual investors as an advisor, but also is the manager of GDMA.

“Almanack and its affiliate have a conflict of interest in selecting the Affiliated Fund for client portfolios because Almanack’s affiliate earns compensation for advisory services provided to the Affiliated Fund. This compensation is in addition to the asset-based fee that you pay to Almanack resulting in the receipt of “two levels of fees.” Almanack addresses the conflict associated with investing accounts in the Affiliated Fund in multiple ways, including disclosing the conflict of interest in this Disclosure Brochure and providing you with detailed information about your account’s allocation to individual positions. These additional fees may be significant, both in absolute dollar amounts and relative to Almanack’s net income, and the receipt and retention by Almanack and its affiliate of these fees create an incentive for Almanack to select and continue to retain an Affiliated Fund over unaffiliated funds.”

Here’s a short summary of what that says in italics above: the advisor charges an advisory client an advisory fee to manage assets. If some of those assets happen to be invested in GDMA, the investor will indirectly pay the additional management fee that GDMA charges inside the ETF. That makes sense, as one can’t carve out the ETF expenses. However, Almanack ultimately receives both the advisory fee and the management fee. They refer to it as “two levels of fees.” Others in the industry might call it “double-dipping.”

As someone who, years ago, faced a similar situation and decided with no question not to double-dip (and in fact earn less in one case), this just does not sit well with me. This is fully-disclosed by the advisor and that’s all they are required to do, as I understand it. There is nothing preventing them from doing this. But it simply seems excessive to me personally. And that, in turn, raises the bar another couple of levels for strongly considering a positive recommendation on this still-new ETF with an active strategy, versus a passive index. It goes without saying, but I’ll say it, that GDMA itself has multiple layers of fees. GDMA’s Management Fee (0.59%) is one level and the underlying ETF fees for the fund’s holdings (about 0.28%) are another. My assumption is that the 0.59% Management fee is earned by the advisor in addition to their regular advisory fee.

Conclusions

ETF Quality Opinion

This is usually a straightforward section of our ETF profile reports to fill out. “Quality” is a split-decision here. The strategy is intriguing, though I want to see more of a tenure before really getting behind it. But those other issues currently cloud the picture.

ETF Investment Opinion

GDMA might end up being one of my favorite ETFs some time in the future. But for now, I have relegated my analysis of it to what you read above, accounting for the positives and negatives. And, while this is an ETF very much worth tracking in 2023, the weight of the evidence, so to speak, concludes with a Sell rating.

Be the first to comment