CHUNYIP WONG

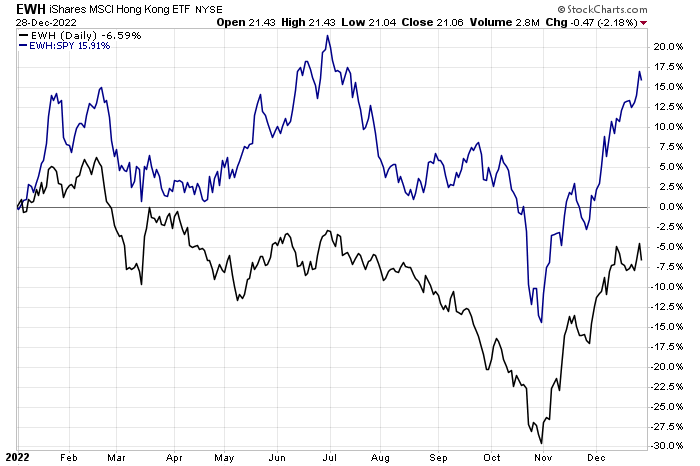

Despite some turmoil in Southeast Asia over the last two years, the iShares Hong Kong ETF (EWH) is not far from the flat line in 2022. The fund has outpaced the S&P 500 by more than 15% year-to-date with a massive rally just in the last two months as geopolitical fears turn to some growth optimism in a world that could face many macro challenges in 2023.

One name has been even more volatile lately but features robust growth ahead. Is there upside ahead in shares of FUTU? Let’s take a look.

Hong Kong Ringing the Bell on Gains Lately

Stockcharts.com

According to Bank of America Global Research, Futu Holdings (NASDAQ:FUTU) is a well-rounded online financial services platform, providing trading, wealth management, market data and information, social collaboration, and corporate services. It mainly serves mainland China/HK population’s investment demand in HK/US and is expanding globally. It had 11.9mn users, 1.42mn registered clients, and 517k paying clients by 2020. Mr. Leaf Li, the founder, Chairman and CEO of Futu, is the largest shareholder. Tencent is a strategic partner and the second largest shareholder.

The Hong Kong-based $9.6 billion market cap Capital Markets industry company within the Financials sector trades at a high 27.0 trailing 12-month GAAP price-to-earnings ratio and does not pay a dividend, according to The Wall Street Journal. The stock has a high short interest of 13.6%.

Futu beat Q3 earnings estimates back in November as it navigates a challenging market. BofA sees a few tailwinds including positive news in the internet/new economy space, misunderstood China regulation risk, and stable U.S. de-listing risk. With high operating leverage, a more open Southeast Asia region could be a boon. Still, ongoing China/US tensions are a risk along with uncertainty around how China’s re-opening goes. Moreover, the Fed’s tightening cycle could be a challenge for emerging markets writ large.

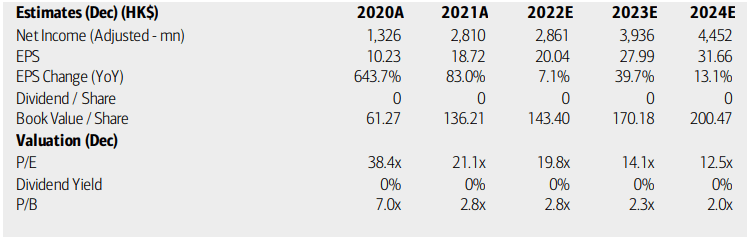

On valuation, analysts at BofA see earnings having risen more than 7% in 2022 with very strong EPS growth coming in 2023. Per-share profits should then moderate at a still-strong 13.1% in 2024. Despite strong earnings, dividends are not expected in this name. Book value per share, key for a Financials company, is forecast to rise big through the next two years. That growth should lead to a more attractive P/E and a falling price-to-book ratio. Seeking Alpha rates the stock with a decent B- valuation rating but with A+ growth. Shares trade at a low 0.5 forward PEG ratio when combining the P/E with the growth rate.

Futu Holdings: Earnings, Valuation, Growth Outlook

BofA Global Research

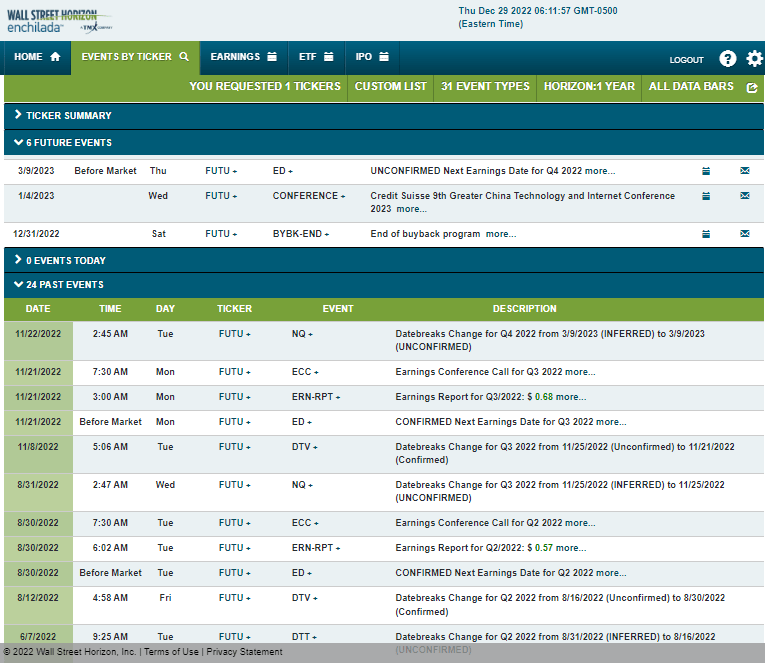

Looking ahead, data from corporate event data provided by Wall Street Horizon shows an unconfirmed Q4 2022 earnings date of Thursday, March 9 before market open. Before that, the management team is expected to speak at the Credit Suisse 9th Greater China Technology and Internet Conference 2023 on Wednesday, January 4 through Friday the 6th. FUTU’s buyback program also ends at the turn of the year.

Corporate Event Calendar

Wall Street Horizon

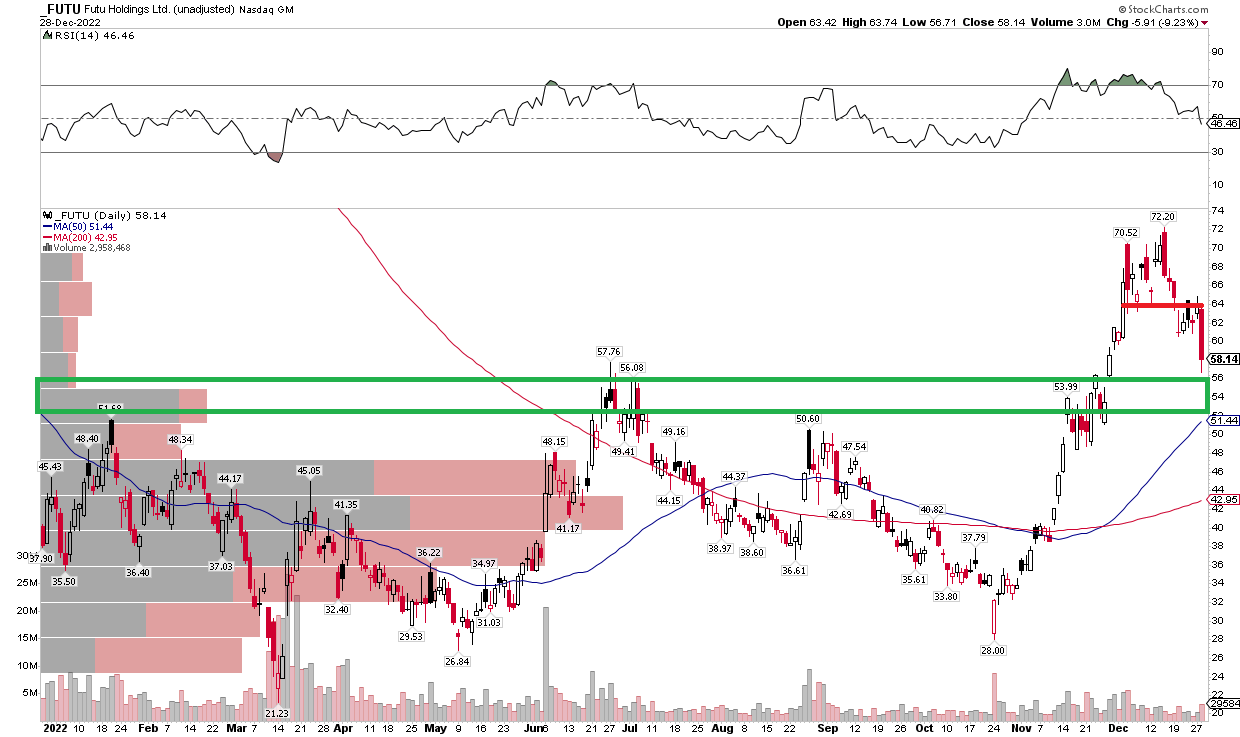

The Technical Take

FUTU has had a wild round trip from a low near $27 just over two years ago to a high in early 2021 of $204. The stock retreated to $21 this past March. A summer rally to $58 swiftly got cut in half by late October before yet another meteoric rise to $72 earlier this month. Now shares trade under $60. I see an important support zone in the $54 to $58 range. That’s also where the rising 50-day moving average could come into play. Also notice in the chart below that the 200-day moving average has turned positive – indicative of an improving broader trend. I think this is a buy-the-dip play with a stop under $50. There could be some minor resistance near $64.

FUTU: Shares Falling Near Support

Stockcharts.com

The Bottom Line

FUTU is a volatile foreign stock that should just be a small part of a portfolio. I think a long stake here makes sense but watch the chart. The valuation looks solid given the growth rate in the years ahead.

Be the first to comment