Nikolay_Popov/iStock via Getty Images

Investment Thesis

Fresnillo (OTCPK:FNLPF) is the world’s largest silver mining company with 53.1 Moz of silver production in 2021. The company has 7 operating assets in Mexico and several exploration & development projects. The company is listed in Mexico, the UK, and available OTC in the U.S.

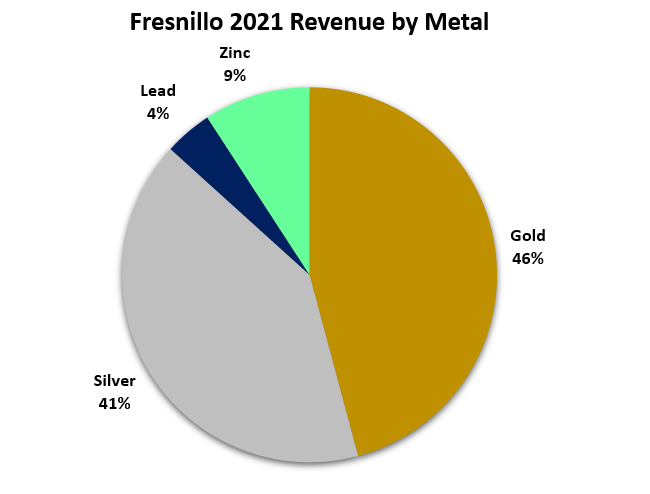

Like many other silver mining companies, it also produces a significant amount of gold, and smaller amounts of the base metals, zinc, and lead. The below chart illustrates the 2021 revenue breakdown by metal.

Figure 1 – Source: 2021 Annual Report

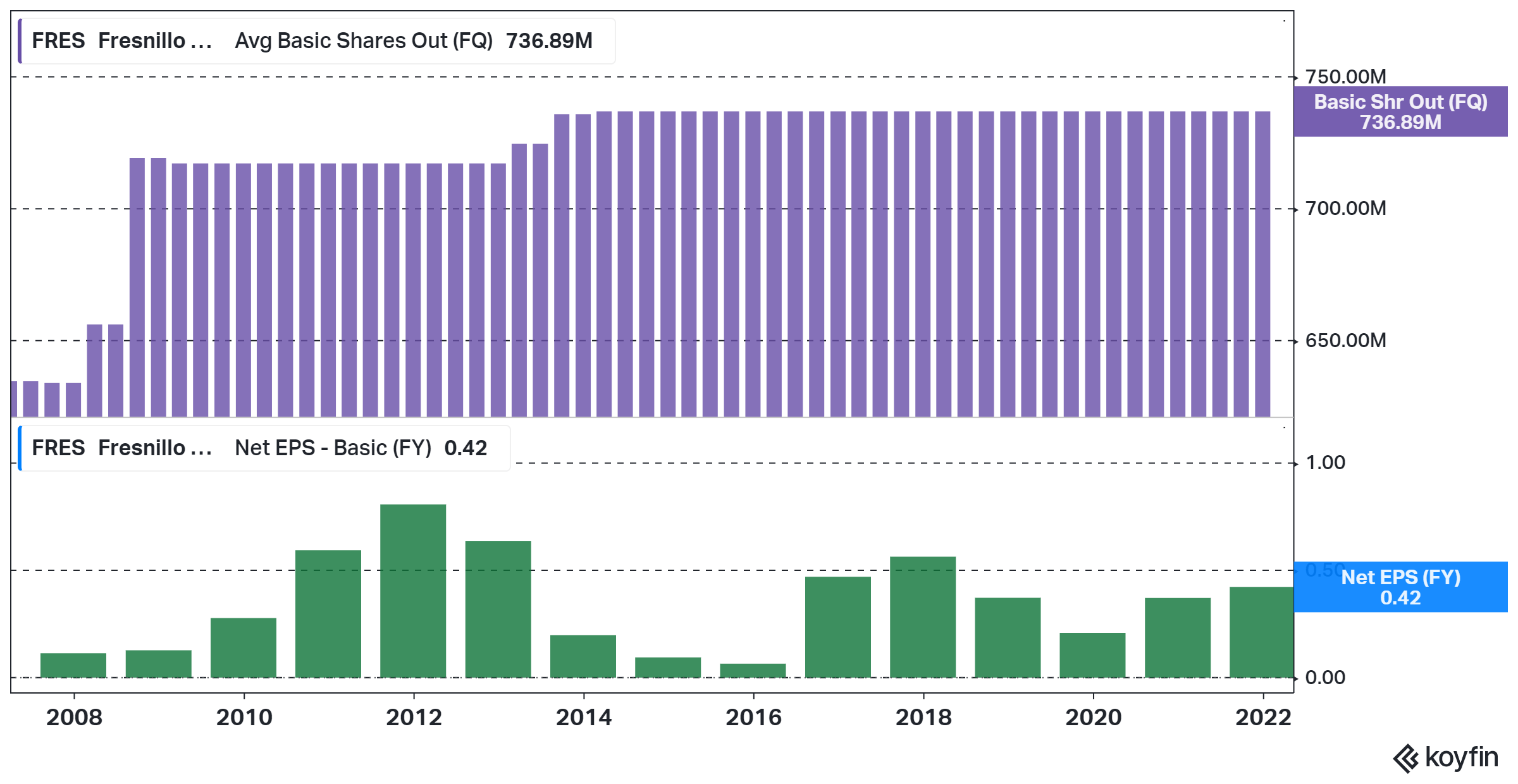

Fresnillo has a long history of being able to profitable produce precious metals and growing production without diluting shareholders. However, the production volume has been declining over the last few years. The company is guiding for an increase in base metal production in 2022 and silver production primarily in 2023, but gold production which accounts for a large portion of revenues is expected to continue to decline.

Figure 2 – Source: Koyfin

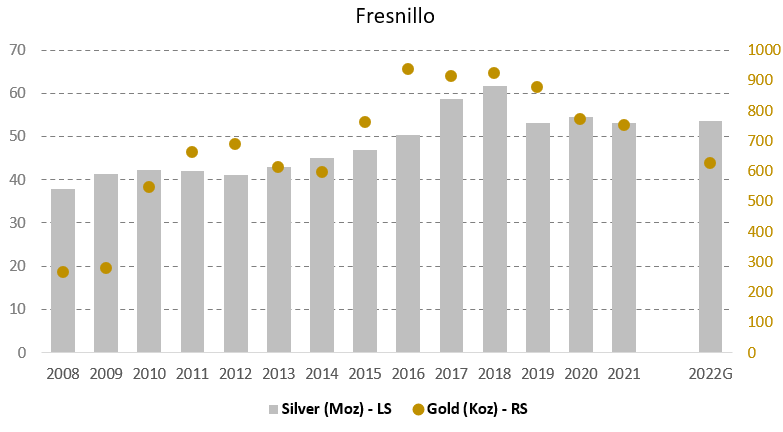

Figure 3 – Source: Annual Reports

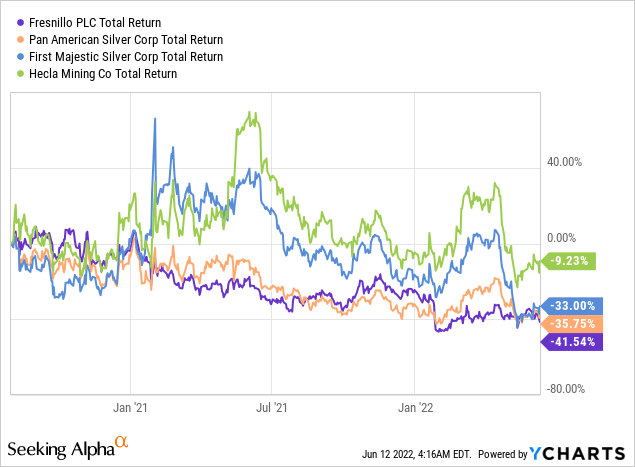

The stock has like many silver miners performed poorly since the peak in 2020 and the valuation is now reasonably attractive at this level following the decline in the stock price.

Guidance & Juanicipio

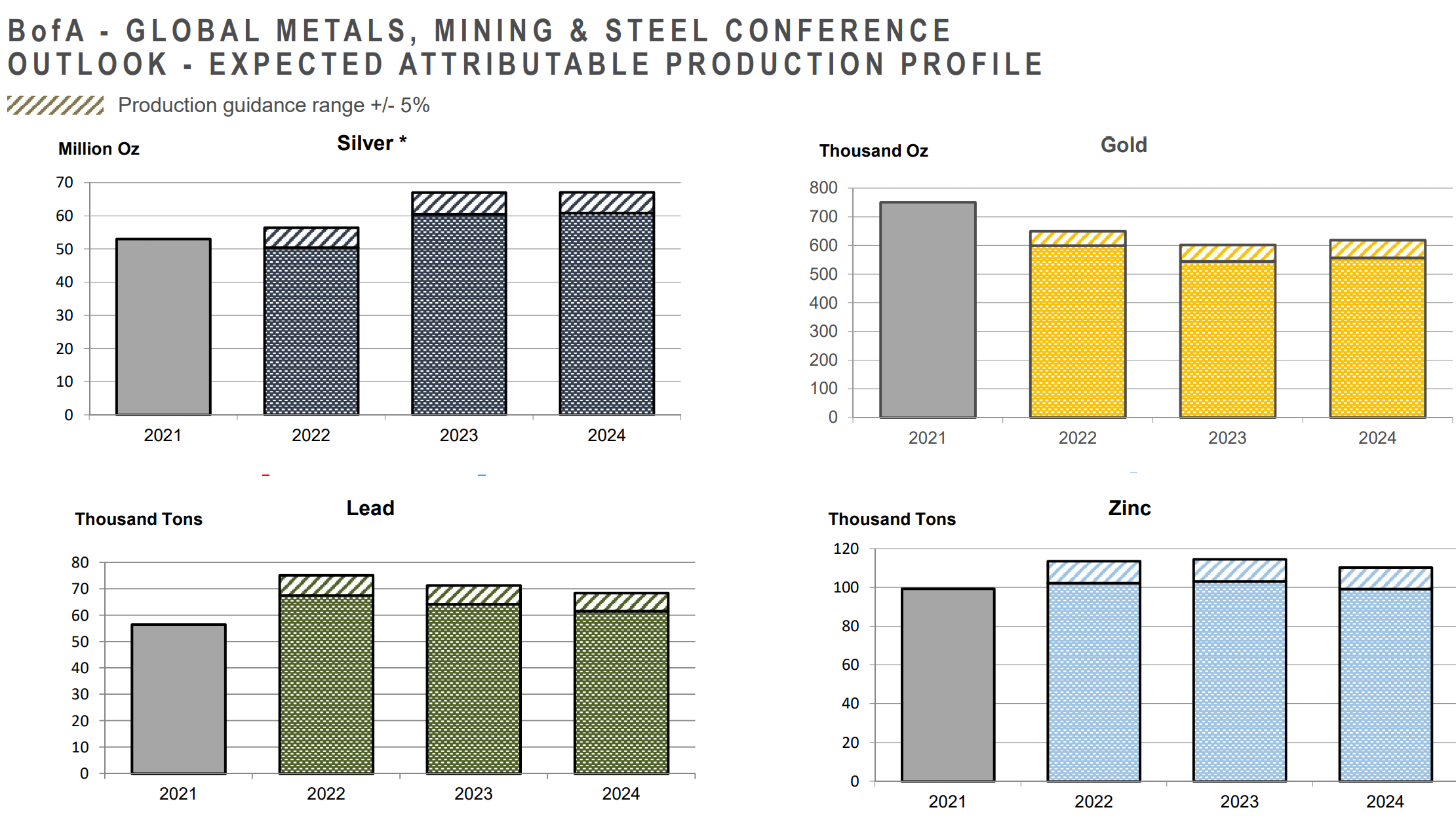

Fresnillo is guiding for an increase in silver and base metal production in 2022 and beyond, while gold production is expected to decline. The expected increase in silver and base metal production is primarily related to the high-grade development project Juanicipio that Fresnillo owns together with MAG Silver (MAG).

The construction of the Juanicipio plant was delivered on time and on budget in late 2021. However, the project has still gotten pushed out with delays getting it connected to the power grid, which is now planned by mid-2022. The company has during the delay been able to process some of the Juanicipio material at the Fresnillo and Saucito plants, but we are talking about more marginal amounts compared to the Juanicipio plant capacity.

Provided the updated timeline holds, the commissioning of the Juanicipio plant has the potential to be a nice catalyst for Fresnillo and MAG Silver.

Figure 5 – Source: BofA Conference 2022 Presentation

Valuation

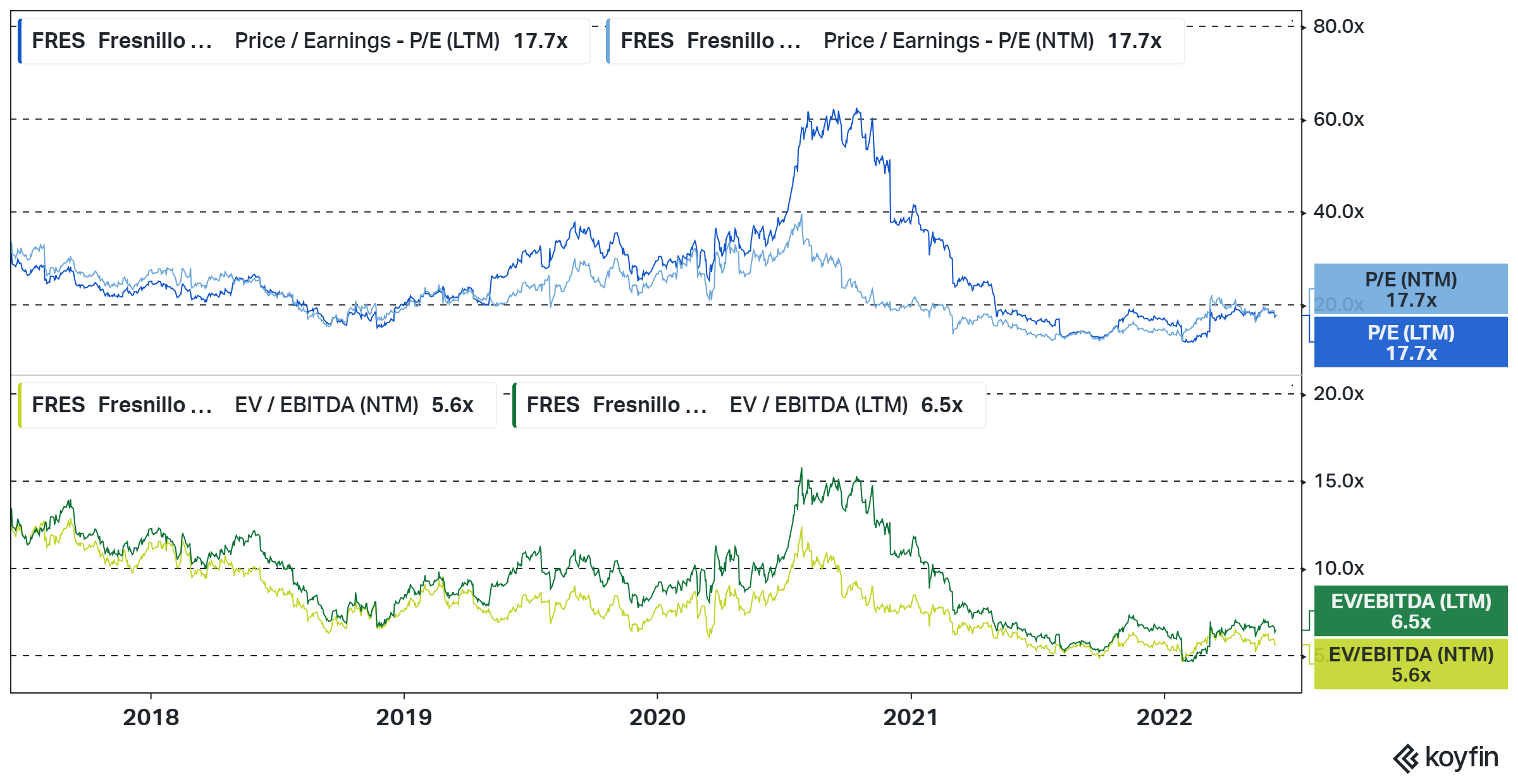

The valuation is rather attractive for Fresnillo. Both the forward and historical price to earnings ratios are around 18, which is far from expensive for a silver miner. It has traded lower earlier this year and during last year, but if we look further back in history, the price to earnings ratio is at the lower end of the historical range.

Figure 6 – Source: Koyfin

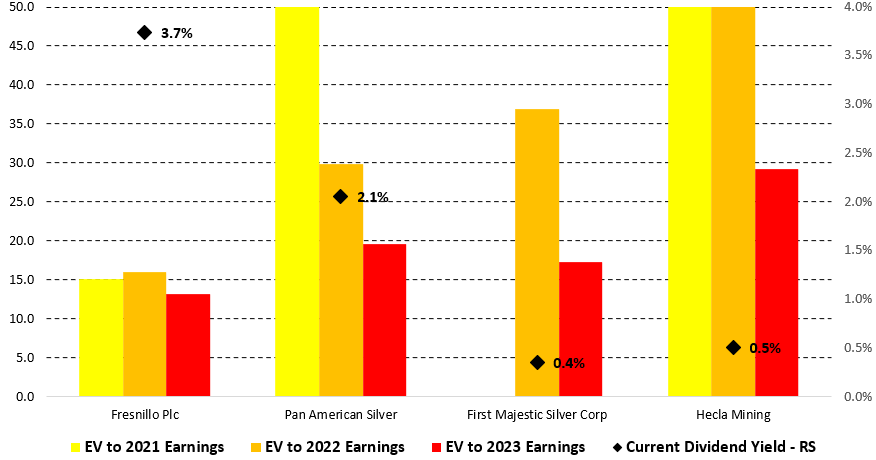

In the below chart I have included a few select silver miners in the industry. Where we can see that the valuation is definitely more attractive for Fresnillo than the peers, even though the difference will decrease in 2023 if all the companies can deliver on the projections.

Figure 7 – Source: Data from Koyfin & Quarterly Reports

We can also see that the dividend yield for Fresnillo is much higher than the peers. However, note that the H1 dividend has already been paid for 2022 even though here will be a smaller dividend payment in H2 2022 as well.

Conclusion

Purely based on valuations, Fresnillo looks quite attractive at this level, both compared to peers and history. You add the potential catalyst of the Juanicipio plant commissioning, the future looks bright for Fresnillo.

It is worth pointing out that Fresnillo has 100% of its production in Mexico though, while the peers have more diversified operations or all of the production in a tier 1 location like Hecla Mining. While at least I still consider Mexico a relatively good country for precious metals mining, there have been some challenges there lately.

We have seen permitting delays or outright refusals in Mexico, without clear reasons for the decision on projects despite excellent local support. There have been many Covid related delays in general. The labor reform in Mexico restricting the ability to subcontract labor that went into effect during 2021 has also caused some production issues and inflation for Fresnillo and other miners in the country.

Another minor negative with Fresnillo is the communication. The company provides updates infrequently, it has also been quite late communicating information related to the Juanicipio delay, weaker than expected reserve replacements, and declining long-term production guidance. This is not ideal in the silver mining industry where stocks often trade on narrative and can have higher multiples than what might be justified by the valuations.

Overall, I still consider Fresnillo one of the most attractive silver producers today for anyone looking for that exposure. I am, however, not long the stock presently as I am invested more in the development part of the cycle, which is even more depressed than most producers at the moment.

Be the first to comment