Klubovy/E+ via Getty Images

Investment Thesis

Forestar Group Inc. (NYSE:FOR), as a majority-owned subsidiary of D.R. Horton, Inc. (DHI), benefits directly from D.R. Horton’s growing market share. I outlined D.R. Horton’s potential in a previous article, “D.R. Horton: Growing Market Share In A (Temporarily) Declining Market.” On top of that, Forestar will continue to grow its own share of the lots supplied to D.R. Horton relative to other suppliers.

Both companies should suffer from a housing market downturn in 2023, but Forestar’s additional growth potential will make it the stronger buy when the market turns back around. Below, I model Forestar’s future earnings to find out what the company is realistically worth and make the recommendation to look for a potential bottom in this stock’s share price.

Introduction

Forestar Group Inc. is strategically focused on being a pure-play residential lot supplier as well as taking advantage of its strong relationship with D.R. Horton (strategy and financial information taken from the 2022 annual report). The company makes virtually all its revenue from developed lot sales, with a small amount of revenue coming from lot banking and land banking—short-term strategic investments to utilize capital before putting it towards long-term projects.

As of 2017, Forestar Group became a majority-owned subsidiary of D.R. Horton, which purchased 75% of the shares and still owns 63% of the shares. The current CEO of Forestar Donald Tomnitz was formerly the CEO of D.R. Horton from 1998 to 2014. This close relationship provides built-in demand for developed lots, which is even protected by Master Supply, Shareholder and Shared Service Agreements.

Valuation

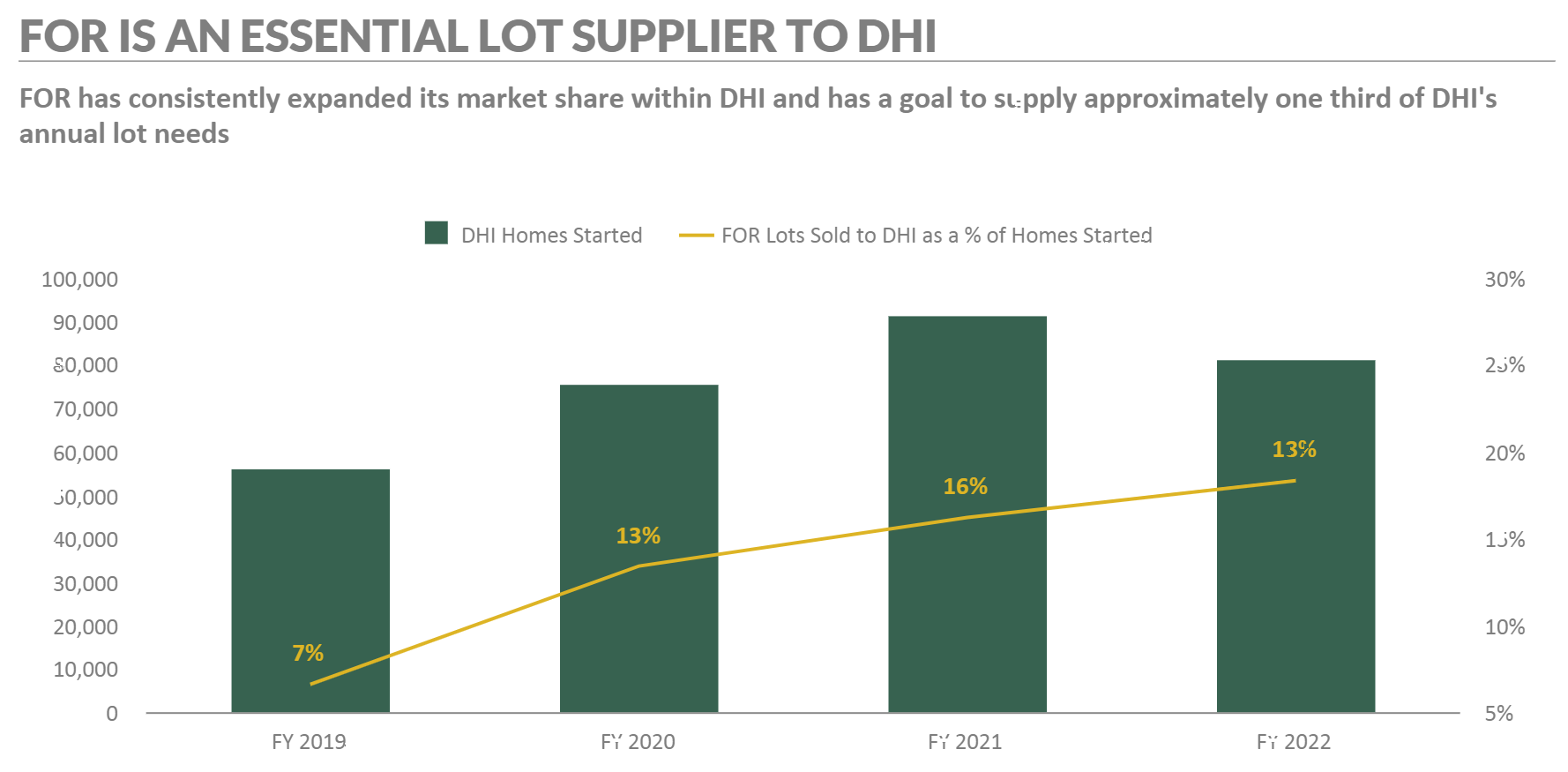

Forestar’s stated goal in its last earnings presentation is to supply lots for one-third of the new homes started by D.R. Horton. The number of lots as a percentage of homes started has more than doubled, from 7% in 2019 to 18% in 2022, as can be seen in the chart below.

Forestar Investor Relations Presentation

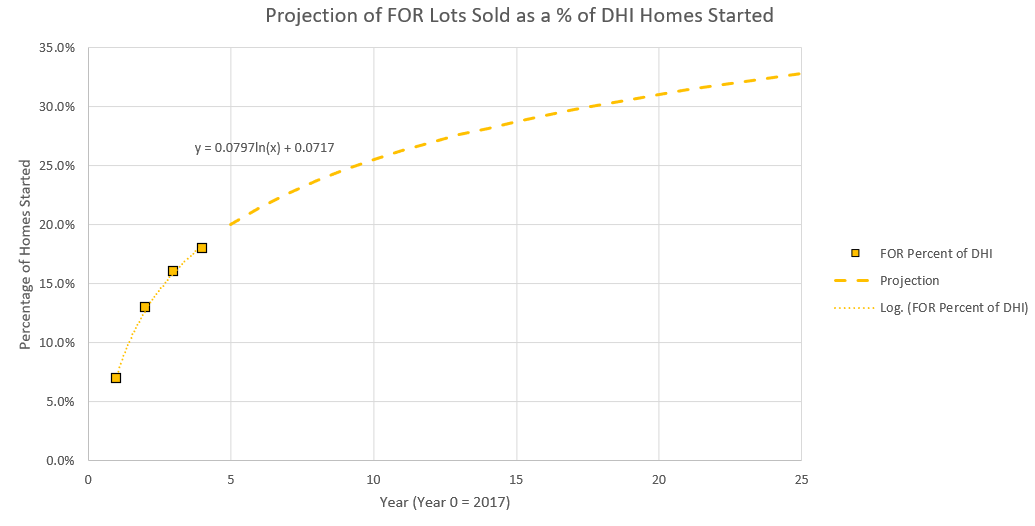

Using this data, I fit a logarithmic curve to project Forestar’s growing share.

Created by Author using data from FOR investor relations documents and the Author’s projections

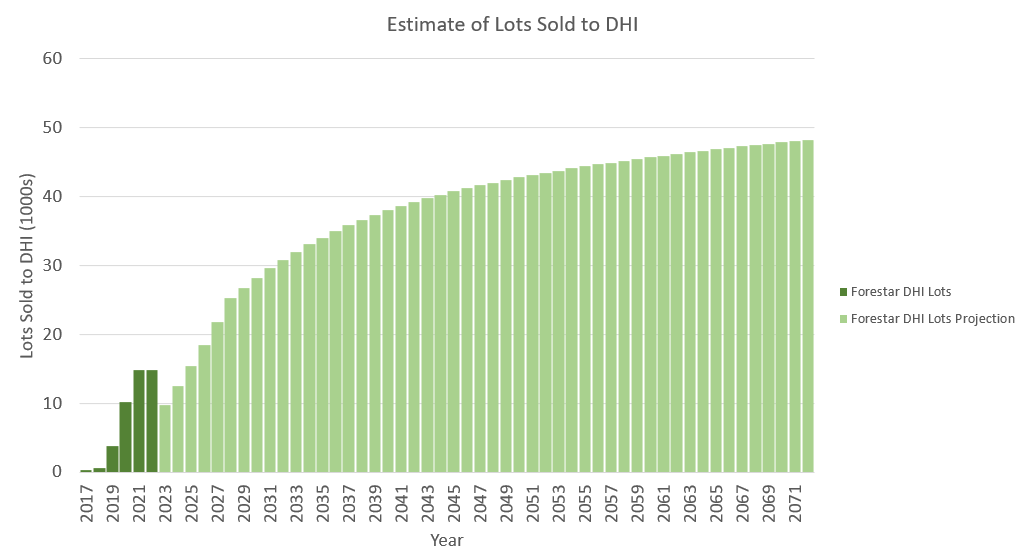

This would put the company on a track to meet its goal of 33% in just under 20 years. Using those percentages, the lots sold to D.R. Horton would be projected as shown.

Created by Author using data from FOR annual reports and the Author’s projections

While Forestar sells a vast majority of its lots to D.R. Horton, it has started increasing the number of lots it is selling to other builders as well. For instance, in 2021 it sold 14,839 lots to D.R. Horton and only 1,076 lots to other homebuilders, but in 2022 it sold 14,895 to D.R. Horton while the number of lots sold to other homebuilders increased to 2,796. For this model, I assumed Forestar would continue to sell around 15% of its lots to other homebuilders, though there is certainly room for upside here.

Next, I sought to figure out Forestar’s net margin. In 2017, 2018, and 2019 the company’s net income benefitted from the sale of non-core assets. To get a truer idea of the company’s net income from the sale of lots, I looked at Revenue minus Cost of Sales, SG&A expenses, and income tax (estimated at a rate of ~21%). In addition to ignoring gain on sale of assets, I ignored equity in earnings of unconsolidated ventures, interest and other income, and loss on extinguishment of debt which were small enough to be almost negligible and would be hard to project into the future. That gave me the following estimates of Forestar’s net margin:

While the company has greatly improved its net margin over time, I used 10% as a conservative estimate for projecting earnings rather than try to guess how much it could continue to be improved. The net margin will also likely come down a bit in 2023 due to a decrease in prices, so 10% seems reasonable.

Author Calculations using FOR Annual Reports

Using these assumptions I calculated the earnings per share and discounted those projected earnings over 50 years with the average real stock market rate of return of 7%. This gave a total value of $91.10 compared with a stock price today of around $16. At the current trailing EPS of $3.59, this valuation would put it at a P/E ratio of 25 as compared to the current P/E ratio of less than 5 and compared to the 15 P/E ratio valuation I developed for DHI. The details of this analysis are listed in the table below.

Author calculations

Risks

As with D.R. Horton, given the situation of the housing market in the short-term, I see too much risk in the FOR stock price to be able to recommend a buy. Forestar’s management has acknowledged the changing market conditions, stating in the last earnings call:

”During most of fiscal 2022, housing market conditions remained strong. In July, we began to see a moderation in demand for finished lots that has continued through today. We are facing a challenging macroeconomic environment with rising interest rates, persistent inflation and softening housing fundamentals. We expect demand for residential lots will continue to moderate in the coming months as homebuilders align starts to a new sales pace.”

However, if the price does drop, that could be a great opportunity to pick up shares. I recommend a “Hold” rating, and my biggest signal for buying would be the Federal Reserve pausing interest rate hikes or even starting to bring rates back down. That would facilitate a turnaround in the housing market from the decline that has just begun in recent months. Based on current probabilities, lower interest rates do not seem likely in 2023, but it is worth watching what the Federal Reserve does, since no one really knows what it will decide to do.

Forestar is well-positioned to handle the coming market conditions. The company has a strong balance sheet with low debt; it has a net debt to equity of 26.9%. It also has $264.8M in cash, and the CEO explained that the company has $620M in total liquidity.

There are also risks with my assumptions for this analysis. For instance, Forestar is clearly very dependent on the success of D.R. Horton. Therefore, this analysis is very dependent on the assumptions used for the previous analysis, including the housing market share and projections of market share.

Forestar itself may not achieve the smooth climb in share of Forestar lots. Also, the number of lots developed for other homebuilders could vary quite a bit, especially as this is not necessarily a core strategy for the company and it has set no specific goals regarding expanding its share with other homebuilders.

Conclusion

Based on my analysis, Forestar Group Inc. is a strong and growing company with built-in demand from its majority shareholder, D.R. Horton. Nominally, its earnings potential would justify a much higher share price and an even higher upside than DHI. However, the new house market is facing declining demand, even a possible collapse. As a result, earnings could fall and the stock price could fall with them.

Forestar Group Inc. is poised to not only survive such a market, but to continue its strong growth into the future. Investors paying attention to the housing market and to the Federal Reserve’s decisions to raise or lower rates could find great buying opportunities for Forestar Group Inc. stock in 2023.

Be the first to comment