gopixa

Thesis

Ford Motor Company (NYSE:F) shares dropped by as much as 10% in early hours of trading, after the company announced that it was facing supply challenges that will likely push up costs in Q3 by an incremental $1 billion. Notably, Ford is one more major U.S. company to warn on earnings, after Nvidia (NVDA), Walmart (WMT), and FedEx (FDX) – to name just a few.

In my opinion, the press release is not necessarily a game changer for an investment thesis relating to Ford stock. The company is still trading relatively cheap versus peers. And the “profit warning” does not give conclusive evidence about Ford-specific versus industry-wide challenges. Accordingly, risk-seeking investors could regard the share-price weakness as an enhanced buying opportunity.

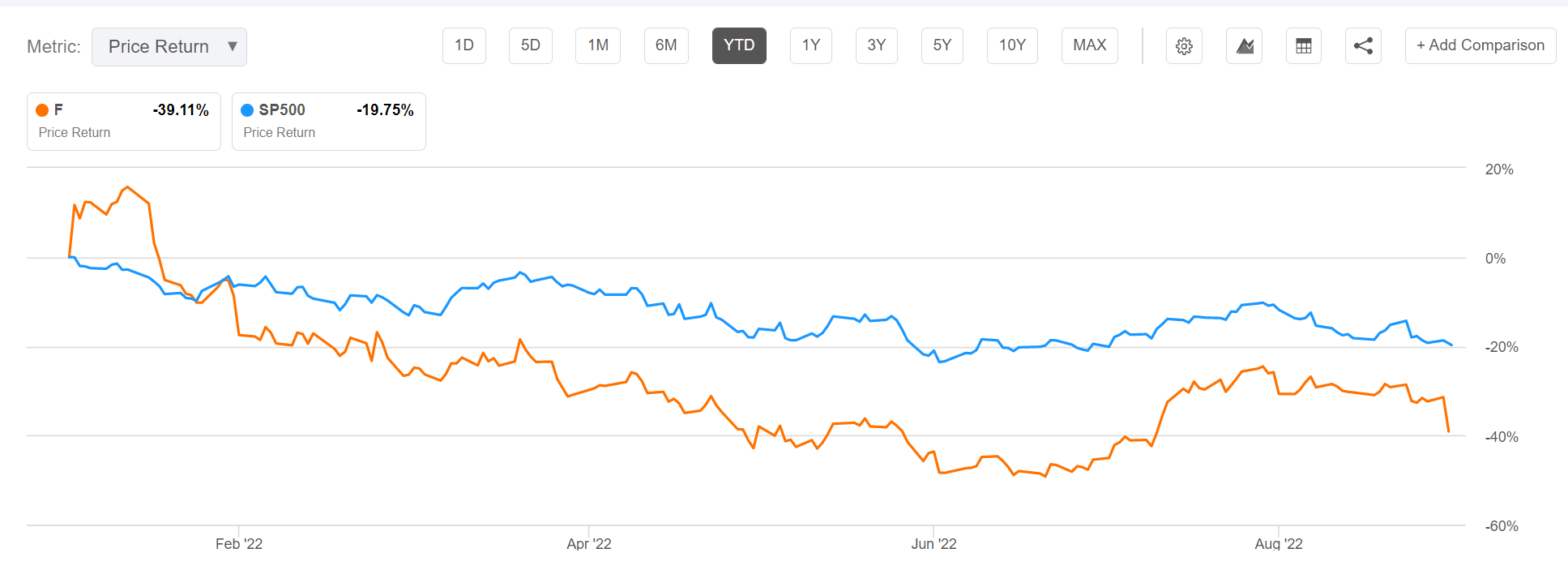

Notably, Ford shares are now down 39% year to date, versus a loss of only 19.8% for the S&P 500 (SPX).

Seeking Alpha

Ford’s Profit Warning

On September 19, after the market close, Ford issued a press release that could very well be viewed as a profit warning. Although Ford reaffirmed guidance for full-year earnings, the company clearly highlighted the challenges related to supply chain challenges and inflationary cost pressure. In fact, Ford warned that costs in Q3 are estimated to be about $1 billion higher than what has previously been expected. Moreover, the company said it expects the number of partially built vehicles to fall between 40,000 to 45,000 cars. The company defines partially build as “largely high-margin trucks and SUVs.”

Accumulating inventory levels will likely pressure the carmaker’s revenue in Q3, but management has highlighted that:

… completing such vehicles will shift some revenue and EBIT to Q4.

As a consequence to the headwinds, EBIT for the June quarter could likely fall $1.3 billion short of consensus estimates: EBIT preliminarily estimated at $1.4-$1.7, versus $3 billion consensus. Ford is expected to officially announce Q3 results on October 26.

Investor Implication

Ford’s weak preliminary results come at a very difficult time for stocks – given high inflation, rising interest rates, and recession risk looming. And as a consequence, already spooked investor sentiment will likely deteriorate further.

Specifically with regard to Ford, however, investors should consider that the press release does not give enough evidence to draw a conclusion about the news’ implications. In my opinion, there are three arguments to consider.

First, are Ford’s challenges company-specific or industry-specific? If the latter is the case, then Ford’s strong selloff should be a clear-cut buying opportunity – given that the dispersion versus peers is not justified. It will be interesting to see if other carmakers will issue similar profit warnings and/or report Q3 materially below consensus.

Secondly, are the challenges temporary or more structural? Although I would advise to remain cautious, I interpret the content of the press release as temporary. I anchor my argument on Ford’s affirmed expectation for full-year 2022 earnings between $11.5 billion to $12.5 billion, which would mean that the headwinds could potentially be corrected as early as Q4.

Third, are the challenges constrained to the supply side? Or, does the company also expect signs of a slowdown in demand? So far, Ford has not specifically mentioned any demand issues. But given the macro-challenges, it would not be surprising if the auto industry suffers the first signs of demand headwinds.

A Buying Opportunity?

Although I generally do not like to “buy the dips,” I feel Ford stock has for a long time traded too cheaply to ignore. And the additional 10% selloff today will provide investors with an enhanced risk/reward set-up.

Investors should consider that Ford stock is currently trading at a one-year forward P/E of x7.2, versus x12.8 for the sector median. This implies a 43% relative discount. Ford’s one-year forward P/S is 0.4, and the P/B is 1.3, which implies a sector discount of 53% and 48%, respectively.

Finally, Ford’s 3% dividend yield should cushion further downside risk.

However, risk-averse investors are arguably well-advised to wait to buy Ford stock until the questions mentioned in the previous section have been addressed (I recommend awaiting the analyst call on October 26, following the official Q3 earnings release).

Investor Recommendation

Macroeconomic pressures are well-noted by now, and there are good arguments to be made that Ford’s profit warning is both more temporary and industry-related than what the price action following the profit warning implies (Ford was down more than 10% after the announcement). Accordingly, risk-seeking investors could regard the share-price weakness as an enhanced risk/reward set-up. In general, however, I would advise to wait for more management guidance.

One interesting trade could be, for example, a dollar-for-dollar pair trade: long Ford, and short a basket of carmakers.

In addition, there could be an interesting trade opportunity for investors who are comfortable trading options and seeking to accumulate Ford stock despite the macroeconomic concerns. Specifically, given the elevated volatility levels (49.5% implied volatility), investors could write January 20th dated $12 Strike PUTs and collect an $0.92 premium (about 7.7%, and 22.5% annualized). Selling PUTs at a 10% OTM strike would lower the purchasing price and thus support investors with a margin of safety, which is strongly needed in light of the current market conditions.

Be the first to comment