gopixa

Ford Buy Thesis

I just bought back into Ford Motor Company (NYSE:F) for my Seeking Alpha Marketplace Service in our Quality Growth Portfolio at $13.27. The service is focused on building a solid retirement nest egg by allocating funds to both income and growth opportunities. Ford happens to fit in nicely with prospects for both. Ford pays a nice dividend coupled with substantial upside potential.

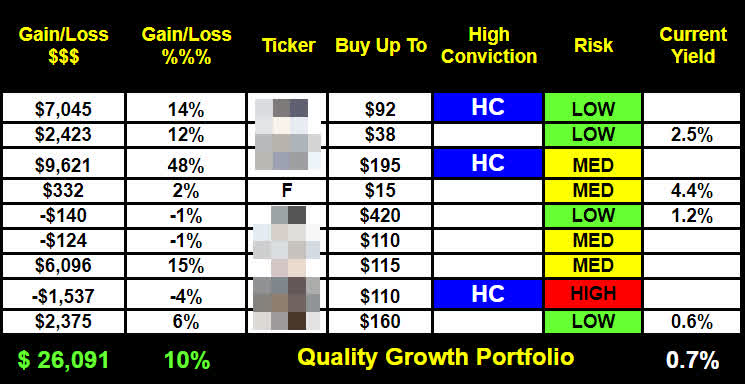

WWI Quality Growth Portfolio

WWI Core Portfolio

What’s more, I see this as an excellent “Buy at the point of maximum pessimism” contrarian play. Just about everyone has gone negative on the company after they surprised on revenues, yet missed on EPS.

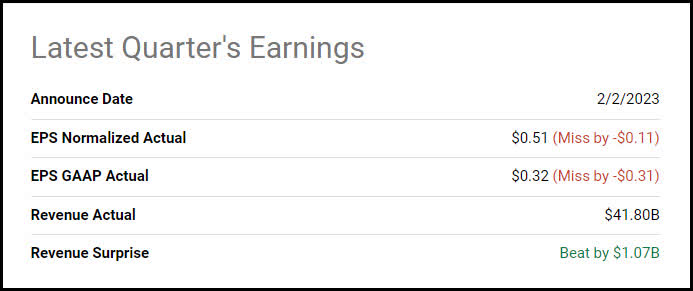

Ford Earnings review

Seeking Alpha

I see those selling out as “first-level” thinkers who have failed to see the silver lining. They are playing checkers rather than chess, so to speak. In the following piece, I make my case that now is exactly the time to buy, not sell Ford. Let’s get started!

First-level thinking

I want to start with a quick note on what I refer to as the “first-level” thinking mistake. Investing is a tough business. More often than not, in order to really come out on top you should be buying when others are selling and selling when others are buying. This is completely counterintuitive to human nature. Yet, having this contrarian mindset has served me well over the years. All the greats from Buffett to Templeton essentially state you should buy fear and sell greed. Nevertheless, that remains one of the hardest things to do.

Even so, I have learned over the years to look past the present and consider the future. For instance, many heard Ford’s CEO Jim Farley state the company left $2 billion dollars on the table. This was taken as a huge negative by most. Nevertheless, I see it as a major positive. Here is why.

$2 billion dollars is on the table

The fact the company beat on revenues, yet missed on EPS means Ford still has some work to do getting its operations streamlined. Farley said himself they left $2 billion on the table. According to Seeking Alpha news:

“The Dearborn-based automaker notched stronger than expected revenue for the fourth quarter at $44B, surpassing the consensus set at $40.73B. However, $0.51 in adjusted earnings per share missed estimates by $0.11. Management blamed “supply chain and production instability,” as well as inflationary impacts and foreign currency fluctuations for the performance.

“We should have done much better last year,” CEO Jim Farley admitted. “We left about $2 billion in profits on the table that were within our control, and we’re going to correct that with improved execution and performance.”

At the start of a call with analysts on Thursday, CFO John Lawler suggested the automaker has “more to do” on job cuts.”

What this says to me is Ford still has plenty of “meat on the bone” left to cut. Farley’s team has identified where the issues lie and are now on a mission to solve them. Substantial improvement to the earnings metrics in the coming quarters is in the cards if you ask me. What’s more, the company has a solid balance sheet and strong free cash flow at present. Chief Financial Officer John Lawler stated on the conference call:

“Our balance sheet remains strong, and we ended the year with $32 billion of cash and $48 million of liquidity. This, coupled with the improvement in free cash flow, provides us with ample flexibility to both fund our growth and return capital to our shareholders. In fact, today, we declared our first quarter regular dividend of $0.15 per share as well as a supplemental dividend of $0.65 per share, reflecting our strong free cash flow and the monetization of our Rivian stake, which is now nearly complete. Going forward, we intend to target distribution of 40% to 50% of free cash flow, consistent with our focus on total shareholder return.”

Lawler went on to say:

“About $1 billion of the $2 billion in lost profits was due to lower production and lost sales, the other $1 billion was in operational costs. He attributed about 60% of the production problem to the chip shortage, with the rest coming from parts suppliers who had trouble ramping up factories. “It’s something that we need to do a better job managing through,” he said, adding that it’s “hand-to-hand combat” securing chips.

To fix the problem, Ford will work with chip suppliers and brokers, as well as redesign car computers to use different chips that are more abundant. “It’s about being as flexible as we can,” he said. For this year, Lawler sees industry sales volumes in the U.S. rising to about 15 million vehicles, which should help Ford with increased sales, especially for its newer models, Lawler said.

Lawler also said Ford sees a mild recession in the U.S. this year and a moderate one in Europe.”

I like the fact they have identified the issues and are laser focused on remediating them. The next point I’d like to bring up is the fact the company just declared a supplemental dividend.

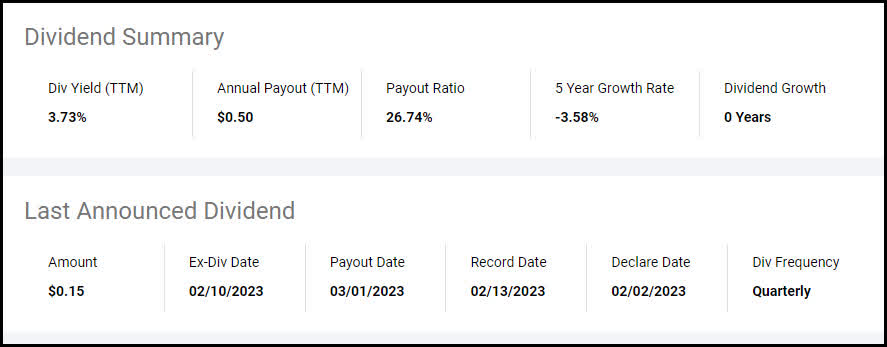

Rivian Supplemental dividend

Another reason I decided to start a position was the opportunity to collect the supplemental dividend of $0.65, ex-div date February 10th. For those of you who missed this opportunity, dividend stocks usually trade lower after their ex-div date so you may still get a chance to buy in at a better price in the coming days.

According to Seeking Alpha news:

- Ford Motor (NYSE:F) declares $0.15/share quarterly dividend, in line with previous.

- Forward yield 4.19%

- Payable March 1; for shareholders of record Feb. 13; ex-div Feb. 10.

- The automaker also declared a supplemental dividend of $0.65/share.

- Ford ((F)) said the supplemental dividend reflects strong cash flow and monetization of its stake in Rivian Automotive (RIVN), which is nearly complete.

Seeking Alpha Dividend summary

Seeking Alpha

Combined with the regular dividend of $0.15, this equated to collecting a 6% payout in one fell swoop. This is about 1.5 years’ worth of dividend income. The primary focus of my Seeking Alpha Marketplace service is retirement income with the opportunity for capital appreciation. Locking in a one time 6% dividend payout reduces downside risk substantially. The dividend provides a nice $0.80 cushion. This brings me to my next point. The stock didn’t really tank after all the bad news was announced. Let me explain.

Stock held up well after earnings

Another positive is the fact the stock didn’t really completely fall apart after the disastrous earnings results were announced. I was expecting the stock to crater and fall all the way to the $11 to $12 range. Remarkably, that didn’t happen.

Ford Post Earnings Chart

Finviz

The stock did not make a new lower low on the news. In fact, the stock didn’t even break through the 50 day SMA at $13.14. This tells me that this level may very well represent a tradable bottom in the stock. Ford CEO Farley and CFO Lawler did not sugarcoat the earnings miss what-so-ever. In fact, it sounded more like a “kitchen sink” quarter. That’s when management lays out all the negatives in one quarter to get all the bad news out there at one time clearing the state. I am 99% positive that was the strategy with the realignment of business units and change in reporting structure coming up next quarter. This major organizational overhaul is another tailwind for the stock, I surmise. Here is why.

Reorganization of business units and reporting structure

Ford didn’t release the typical slide show this time. They are going to start reporting earnings on the newly streamlined operations structure starting next quarter. zin fact, they are very optimistic about the prospects for 2023 under the newly minted regime. According to the press release:

“People, Plan, Products Position Ford Well for ‘Pivotal’ 2023 Despite Effect of Volume Shortfall on Q4

Full-Year 2022 Results

• Fourth-quarter revenue totaled $44.0 billion, net income $1.3 billion, adjusted earnings before interest and taxes $2.6 billion

• Full-year net loss of $2.0 billion attributable to special items; adjusted EBIT $10.4 billion • Operating cash flow $1.2 billion for the quarter, $6.9 billion for the year; adjusted FCF $2.4 billion in Q4 and $9.1 billion for all of 2022

• First-quarter regular dividend of 15 cents per share declared, plus supplemental dividend of 65 cents per share, enabled by strong FCF, nearly complete monetization of stake in Rivian

• Company anticipates full-year 2023 adjusted EBIT of $9 billion to $11 billion and adjusted free cash flow of about $6 billion

Ford’s fourth-quarter and full-year 2022 operating results were below its expectations, but the company is optimistic about what’s possible now with three distinct, customer-focused business segments: Ford Blue for iconic gas and hybrid vehicles, Ford Model e for breakthrough connected electric vehicles, and Ford Pro for products and services that help commercial customers transform and grow their organizations. “I’m excited about 2023, which is pivotal for us,” said President and CEO Jim Farley. “We’ve got clarity and ambition with the Ford+ plan, a strong team carrying it out, and a lineup of great products and customer experiences that’s getting even better.”

So Farley and company has identified the issues and is completely realigning the business units. As an auditor for EY, one of my areas of expertise was “Cost reduction and avoidance.” I can tell you without question a major part of the process when Ford realigns the business units will be a substantial reduction in headcount. I posit when these announcements are made the stock will react positively. The company is set to do a “teach in” in March for analysts regarding the new reporting structure. On top of all this, the company is trading at a significant discount to the market and on par with its historical 5 year average.

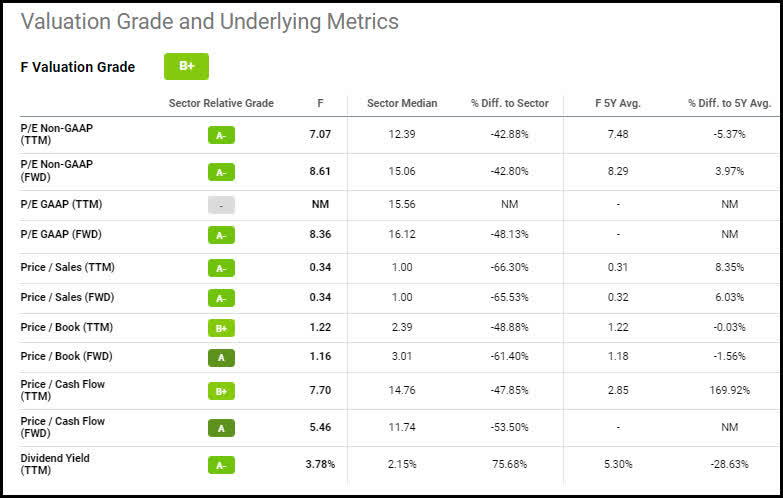

Valuation Analysis

Below are the valuation metrics provided by Seeking Alpha’s quant analysis.

Seeking Alpha Quant Valuation Metrics

Seeking Alpha

Ford stock is trading at a significant discount to its peers and on par with its five year average. This is nothing special for Ford. The stock has been stuck at these levels for quite some time. I have traded in and out of Ford several times over the years for substantial gains. I was actually on the EY audit team for Ford back in the 90s. I have seen this movie several times before. I expect Ford management to come through next quarter and the stock to rally higher. Now let’s wrap this up.

The Wrap-Up

Locking in the supplemental dividend

As I stated earlier, the primary focus of my service is to provide members with dividend income opportunities with a secondary objective of capital appreciation. Since I was already looking for a chance to initiate a new position in Ford, there was no way I was going to pass up a 6% payout in one fell swoop. It was a no-brainer buy with the supplemental dividend on the table as well.

Glass half full perspective

Ford has some issues to address. This was evidenced by the poor EPS results last quarter. Yet, looking at it from a “glass half full” point of view, this means there is a lot of meat on the bone left to cut. Farley said himself they left $2 billion dollars on the table. What that says to me is the is $2 billion reasons to buy Ford stock now.

Downside risk marginalized

The fact the stock did not break through support at the 50-day SMA leads me to believe that it was mostly retail weak hands that sold out. If the large institutional players would have sold out, it would most likely have made a new lower low. The strong support at the 50-day SMA coupled with the $0.65 supplemental dividend provides a substantial margin of safety at present.

A fresh start

What’s more, the streamlining of business units and restructuring of reporting metrics will provide the company the opportunity to make major cost cuts. I see this as being the next big positive catalyst for the stock.

Final Thought

Finally, Ford Motor Company has an excellent product lineup and is in the process of creating their own battery plants. All this bodes well for Ford in 2023. My 12-month price target is $18, implying 37% upside. Those are my thoughts on the matter. I look forward to reading yours. Thanks for your time and consideration!

Be the first to comment