ANNVIPS

Company description:

Foot Locker, Inc. (NYSE:FL) is an American sportswear and footwear retailer, selling athletic footwear, apparel, accessories, equipment, and team-licensed merchandise.

The company operates under several brands, including Foot Locker, Lady Foot Locker, Kids Foot Locker, Champs Sports, Eastbay, atmos, WSS, Footaction, and Sidestep.

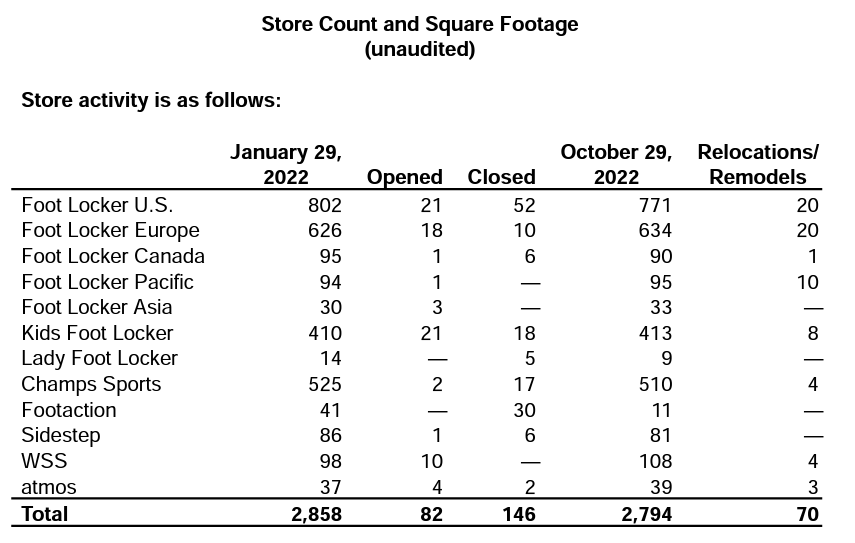

As of 2022, Foot Locker operated 2,858 retail stores in 28 countries across the United States, Canada, Europe, and Asia, as well as 142 franchises.

Foot Locker found itself in the news, not too long ago as NIKE, Inc. (NKE) decided to pull back on their relationship with the retailer, shifting focus to DTC. Foot Locker’s shares fell over 20% in response to this news, and many wrote the company off. Shares have increased 30% since then, but ended 2022 down 15%.

We love an underdog story, and Foot Locker may well fit into this. We will look to assess their commercial shift away from Nike and how the financials stack up, especially in recent months. We will also consider macroeconomic factors, and how this will impact the business in the near-term.

Commercial considerations of recent developments:

The Nike retreat:

With touchy subjects, it is best to just cut to the chase. Nike is the largest footwear brand in the world, with a market cap of $186BN. This alone is the reason for the negative sentiment towards Foot Locker, they have lost the biggest whale in the ocean.

The problems may not necessarily just come from the loss in Nike sales, however. Foot Locker is viewed as part of sneaker culture, less corporate than many of its competitors and a retailer who specializes in the area. This is very much the case in the U.S. and is driven by Foot Locker’s ability to stock the newest and most in-demand sneakers. This is an important differentiating factor, as retailers have little scope to differentiate themselves otherwise (price competition is high and dictated to an extent by brands). Many do not even seek to differentiate in sneakers specifically, as they sell a host of goods. For Foot Locker, their bread-and-butter is sneakers, with apparel very much a secondary offering. Therefore, to lose Nike and Air Jordan, Foot Locker loses credibility as being the retailer most in touch with the culture. Should Foot Locker fall out of favor, the knock-on effect will be a fall in sales across all lines.

The response:

Foot Locker has made several moves in order to mitigate the impact of Nike’s departure. The focus has been on a strategic shift away from reliance on brands, and towards online sales, customer service, and diversification of offerings.

Firstly, Foot Locker has reshuffled its management team. Mary Dillon has been recruited as CEO. Under her leadership, Ulta Beauty, Inc. (ULTA) grew revenue at a CAGR of 14% and impressively increased online sales several fold. This is a very shrewd hire, as online penetration has been poor from Foot Locker. Regardless, she has a strong track record and brings fresh ideas to the business. In addition to Mary, several senior promotions and hires were made, including appointing Neil Bansal as its new executive vice president and first chief strategy and transformation officer. Neil is a seasoned consultant, with experience in strategy and transformation. The impact of these hires has yet to be seen, but it is very positive to see Foot Locker acknowledge the crossroads the business is at and respond in-kind.

Furthermore, Foot Locker has looked to deepen its relationships with other big brands. Reebok has announced exclusive footwear will be sold through Foot Locker, allowing Foot Locker to differentiate itself and draw customers to stores. Foot Locker and Adidas are looking to triple sales through the retailer in a single year, with more product allocation and shared marketing spend. Foot Locker and Puma have also announced further exclusive designs will be sold through FL. This will be focused on sneakers aimed at a younger audience, an area weakened with the loss of Nike. These are all positive moves, as they are not just looking to plug the hole left by Nike. FL is investing in the long-term relationships with the brands, thus enabling greater long-term sales. This does put the onus on FL to deliver, however. These brands want to see hype and demand for their exclusives, which FL must contribute towards.

Finally, Foot Locker has made other notable strategic decisions. They have launched in the Philippines as part of a strategic partnership with an Indonesian retailer. As well as, they are opening new flagships in both London and Paris. Perception is key, and so showing the world expansion and continued development is a valuable part of brand development. They also purchased two businesses, WSS and atmos, which differentiates their offering and is an entry into the Japanese market.

Our overall assessment of Foot Locker’s response is positive. The business is not a $100BN behemoth that can throw money at the issue and is vulnerable to the whims of brands. With this factored in, the decision-making has been logical, and the partnerships secured are promising.

An unexpected Nike return

Nike is facing some issues following the decision to reduce retailer usage. It is holding record-high inventory levels (almost double 2019 – Source: Tikr Terminal) and is struggling to shift it. The reason for this is weakening economic conditions, something we will touch on later, and is a problem for all brands currently. In times like this, further developing retail partner relationships is key, as it provides a level of predictable sales and another channel to sell inventory. Nike likely believed COVID-19-driven demand would continue, otherwise they would have waited until current economic conditions improved before ditching FL.

Will Nike change their mind? Probably not. But this does send a message to the industry of what the risks are around focusing on DTC.

Macro-conditions

Macroeconomic conditions have deteriorated in 2022, and our belief is that this will continue into 2023.

The main reason for this stems from inflation. Inflation currently sits at 9.3% in the UK and 7.1% in the U.S., remaining unsustainably high for most of 2022. In response to this, Central Bankers have attempted to rein this in by increasing interest rates, which has yet to be successful. The net impact has been an almighty squeeze on households and consumers, with a cost-of-living crisis caused by both greater borrowing costs and price increases.

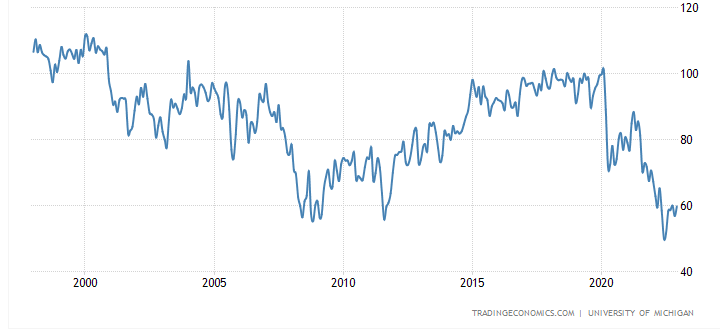

When we look at the consumer sentiment indicator, we observe a decline to levels last seen during the ’08 Crisis.

United States Michigan Consumer Sentiment (Trading Economics)

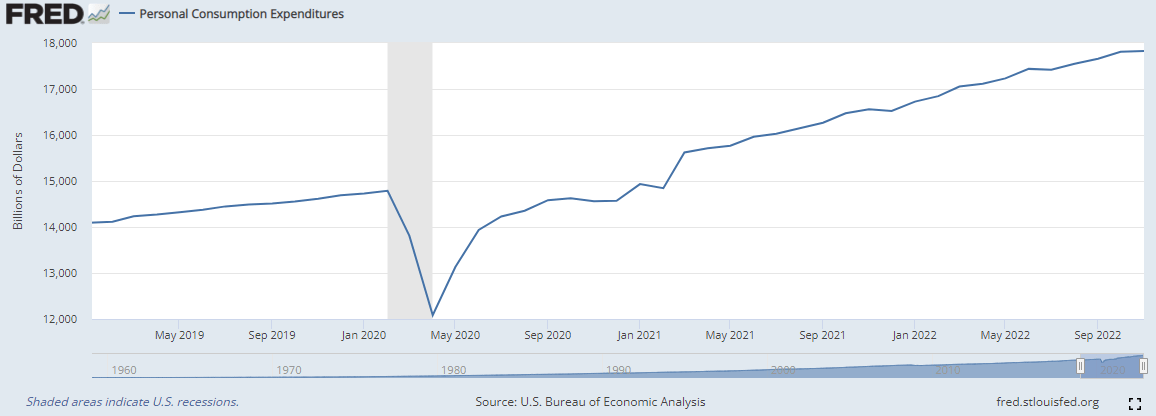

Consumer spending, a lagging indicator, has also slowed to a plateau.

Personal Consumption Expenditures (FRED)

The reality is consumers are struggling to meet their necessities. This is highly problematic for Foot Locker, as sneaker expenditure is seen as a luxury. Demand is elastic, and so will likely fall in the coming year.

Consideration must be made for when things will improve. Inflation expectations are falling around the world, which could mean late 2023, or early 2024, is when we may be able to see expansionary policy from governments.

Financials:

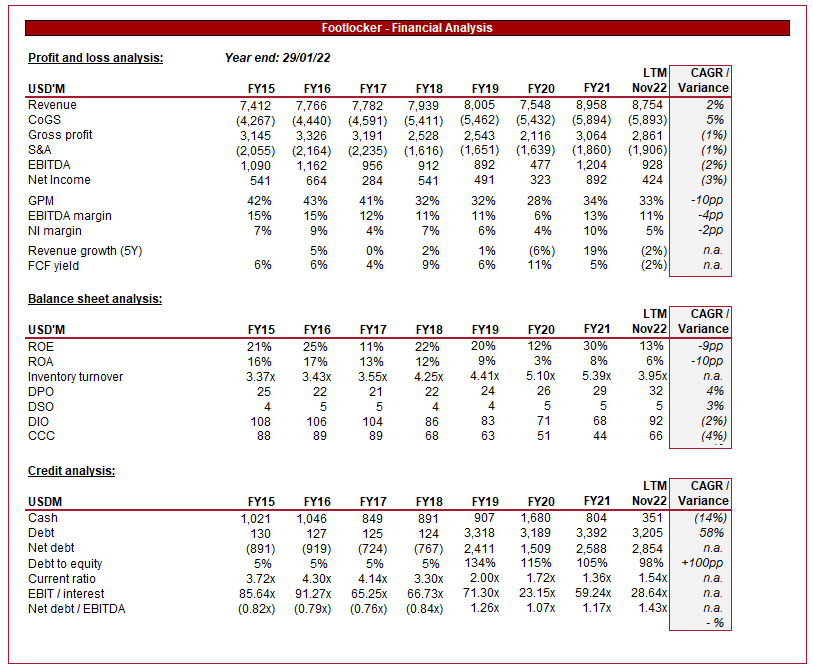

FL – Financial analysis (Tikr Terminal)

Foot Locker’s financial performance in the last few years can be summarized by the word stagnation. Revenue has grown at a measly CAGR of 2%, which is below inflation for the period, with CoGS increasing 5%. On the bottom line, this translates to a CAGR of -3%. FY15 also includes a one-off legal expense, and so the fall in NI is actually larger. Interestingly, S&A expenses have fallen overtime. One would expect FL to increase its marketing efforts in order to generate revenue, but we do not see this. There seems to be a glaring opportunity here to attempt growth through marketing.

Margins have steadily declined, as rising costs have eaten away at weak revenue growth. Foot Locker clearly has no bargaining power on the pricing side, and given the number of competitors in the retail space, this is unlikely to change.

From a Foot Locker balance sheet perspective, we observe improving efficiency regarding inventory. Inventory turnover has increased and contributed to a better cash conversion cycle. This a small highlight in an otherwise drab view.

What may be a concerning sign is that inventory currently held is well above the 7-year average ($1,695M v. $1,219M). Inventory at year-end has remained between $1,200-$1,300 for 6 of the last 7 years, suggesting strict inventory control. The c.$400M uptick suggests above average difficultly in shifting inventory.

Accounting debt has increased substantially due to the new lease standard in 2019. The value of loans has remained fairly flat over the historically period. FL generates positive CFO and funds share buybacks through this. The reduction in cash has been partially fueled by the purchase of WSS and atmos. Although it is too early to judge these acquisitions, they do make up around 5% of Foot Locker’s number of stores and gives Foot Locker access to Japan.

Store count (Q3 investor pack)

Overall, Foot Locker’s financials are disappointing. Management seems to have either neglected stagnating growth or failed to address it. Without looking at historical numbers, an 11% EBITDA margin and 5% free cash flow (“FCF”) yield (before the large increase in inventory in the LTM period) is objectively a good starting point. Management can certainly utilize these funds to turn the business around.

Outlook:

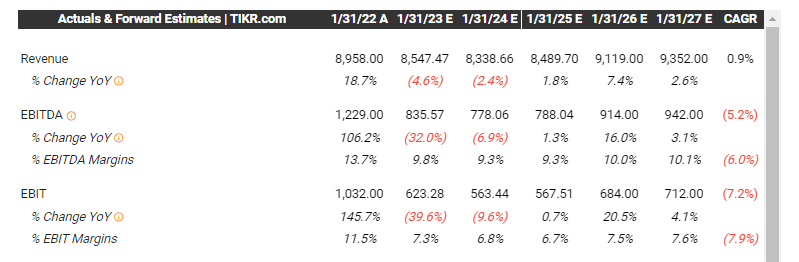

Analyst forecast (Tikr Terminal)

Analysts are forecasting a tough two years for Foot Locker, likely as a result of economic conditions and the current operational weaknesses. We concur with the view that 2023 will be tough, but it’s yet to be seen if the commercial / operational restructuring will yield benefits from 2024.

Valuation:

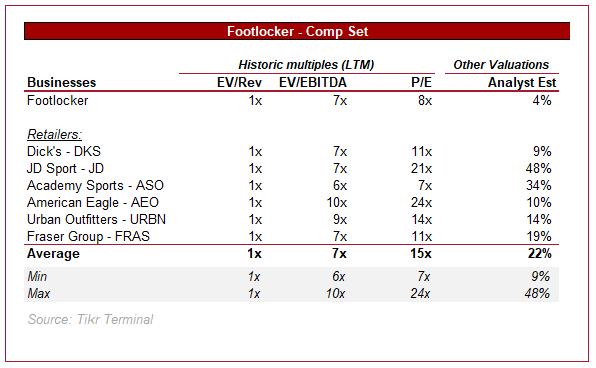

Peer group valuation (Tikr Terminal)

Foot Locker’s valuation is in line with that of its peers. P/E ratio is noticeably better but impacted by noise below the line. Analysts believe there is little room for stock appreciation currently, likely believing time and investment will be required to turn the business around.

When we compare these businesses on key metrics, we observe a relative normality between the businesses. Foot Locker’s GPM is worse, but the difference is gone on an EBITDA level. Interestingly, the forecast growth is abnormally low for Foot Locker, reflecting continued stagnation going forward.

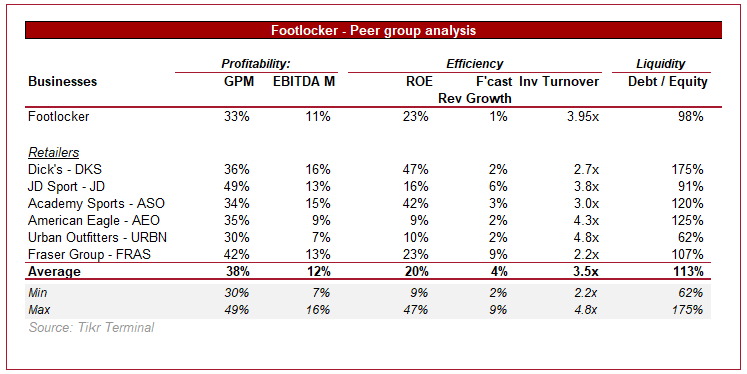

Peer group analysis (Tikr Terminal)

Unfortunately, there does not seem to be an opportunity to acquire Foot Locker at a discount. Even when we compare the stock to its 16-year average valuation, it is trading in line with this level (Source: Tikr Terminal). This does mean investors get any upside potential above and beyond expected for free, the likelihood of which is currently unknown.

Conclusion

Foot Locker has hastily taken the correct steps to move on from losing Nike, and we believe is well positioned to turn performance around. It is, however, too early to judge this process. Currently, profitability is fine without being impressive, but given the nature of retail, it is very difficult to outperform. Importantly for us, the business is cash-generative, and so any turnaround resources required can be financed with cash.

Unfortunately for Foot Locker, the near-term looks tough to navigate as demand will almost certainly fall. Retail as a whole will struggle with this and so the attractiveness of Foot Locker would come from being able to pick up shares at a discount. This is not possible with Foot Locker trading in-line with peers and its historic average.

We rate this stock, slightly harshly, as a sell. Profitability will likely fall and with it being fairly valued, share price will likely succumb to negative market sentiment.

Be the first to comment