Stock photo and footage

Last week, lithium-ion battery manufacturer Flux Power Holdings (NASDAQ:FLUX) or “Flux Power” reported better-than-expected Q1/FY2023 results with both top- and bottom line results exceeding expectations.

Company Presentation

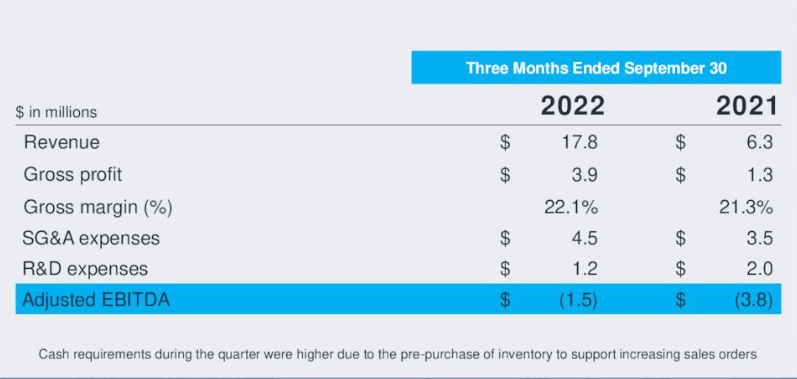

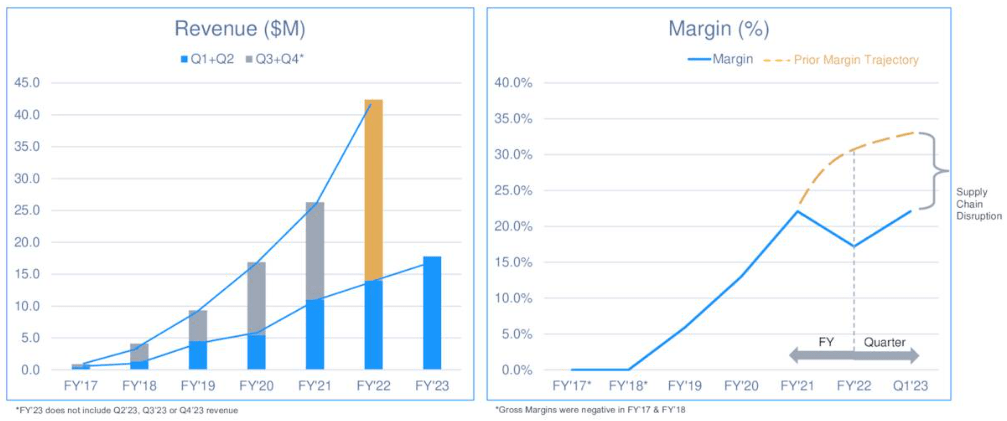

Revenue increased by 184% year-over-year and 17% sequentially to $17.8 million while gross margin of 22.1% continued to benefit from a number of recent improvement initiatives as well as easing supply chain disruptions.

Company Presentation

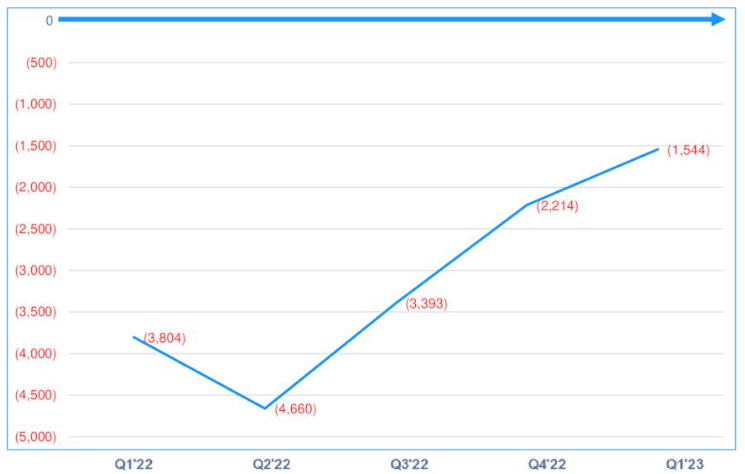

As a result, Adjusted EBITDA of negative $1.5 million continued its recent upward trend.

Company Presentation

That said, cash flow remained under pressure as the company decided to increase inventory by 16% sequentially to $18.9 million “to mitigate supply chain disruptions and support timely deliveries“.

So far in Q2, Flux Power has used some additional cash with cash and cash equivalents now down to $0.25 million and only $1.4 million available under the company’s $8 million revolving credit facility with Silicon Valley Bank as of November 4 but the company retains access to a currently undrawn $4 million subordinated line of credit and has $5.7 million left under its ATM facility with H.C. Wainwright.

Consequently, management does not expect any near-term liquidity issues and on the conference call, stated its intent to “avoid raising equity capital prior to reaching profitability“.

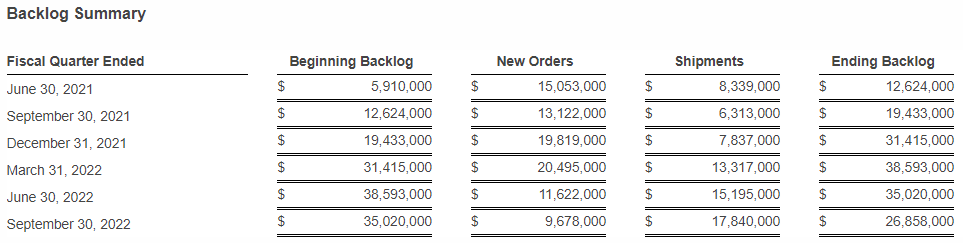

That said, order intake of $9.7 million was disappointing and resulted in the company’s backlog decreasing to a new one-year low.

Company Press Release

On the conference call, management was quick to dismiss related analyst questions by pointing to a letter of intent received from a Fortune 100 customer earlier this year which has been looking to secure build slots as part of its ongoing material handling fleet conversion. Potential revenue derived from this LOI might exceed $20 million over a two-year time frame.

Of course, we’re in a very volatile period in terms of the market, but at the same time, we work very closely with those very large customers. And in terms of their forecasting of what they need, we may not get the order. So you look at the backlog or you go, oh god, you guys are going to get the orders. That’s not. That’s an indicator, but it does not tell the whole story. They get the forklift first and then they get that — then they put battery orders to us.

Flux Power also added two new Fortune 500 customers during the quarter with “each having seven figure revenue potential“.

On the call, management reiterated its focus on reaching profitability “in the very near future” but according to my estimates this would require scaling quarterly revenue and gross margin to approximately $25 million and 30% respectively with these numbers not being supported by the company’s backlog at this point.

Bottom Line

Last week, Flux Power’s shares rallied on strong Q1/2023 headline numbers and management’s promise to abstain from near-time dilution for common equity holders but cash flow remained under pressure and new order intake was quite weak.

Taking into account recent backlog and gross margin trends, Flux Power is unlikely to achieve profitability anytime soon.

Following the 100%+ rally from recent lows, investors should abstain from chasing the shares at current levels.

Be the first to comment