Vertigo3d

FLEETCOR Technologies, Inc. (NYSE:FLT), which provides digital payment solutions for businesses, is facing significant headwinds for 2023, as the company projects slowing organic growth while bad debt expenses are probably going to continue to climb.

That said, the share price of the company has bounced big off its 52-week low of $161.69 per share, and is now trading at slightly over $200.00 per share as I write; a move I believe is far more than justified based upon the visibility we now have with the company.

Something to look at on the technical side is the company, over the last several months, has hit a ceiling of a little over $200.00 per share before pulling back. And since it has been trading in a fairly tight range since November 1, 2022, I think the market is waiting for confirmation the company is probably going to underperform in the quarters ahead before moving out of the trading range of about $175.00 to $200.00 it has been in.

In this article we’ll look at some of the headwinds the company faces, management guidance, and the strength of its balance sheet, which will provide support even if the share price plummets over the next year.

TradingView

Headwinds

By far the biggest headwind the company faces is the recession. While not being officially announced yet, many companies believe we’re already in. FLT management is basing their outlook on the assumption there’s going to be recession in 2023, and that it’ll have a material impact on the performance of the company.

That said, the company believes it is recession-resilient because a lot of spending from its customers is essential and not discretionary. For example, in a vertical like fuel, demand for the services of the company has increased when prices are higher or when companies are looking to cut costs.

While that’s true in other verticals it competes in, there will also be a number of them that will be negatively impacted. That’s the case even with it being diversified geographically, by various company sizes, and by a variety of segments. An example of that is the construction industry, which has been under pressure for a while now.

Another headwind the company faces in 2023 is in regard to bad debt expense, which during the third quarter of 2022 jumped 8 basis points to $37.00 million, approximately $10.00 million higher than the prior quarter, and about $26.00 million more than it was in the third quarter of 2021.

The boost in bad debt expense came primarily from an increase in loss severity associated with higher fuel prices in the second quarter of 2022, along with a boost in application volume and fraud.

In the third quarter bad debt levels continued to be high because of new customer sales that normally have “higher loss rates than the existing book, higher fuel prices and the changing macroeconomic landscape, which puts pressure on our smaller customers.”

I think this is going to continue to be a problem for FLT in 2023, which would put downward pressure on margins and earnings.

Organic revenue growth

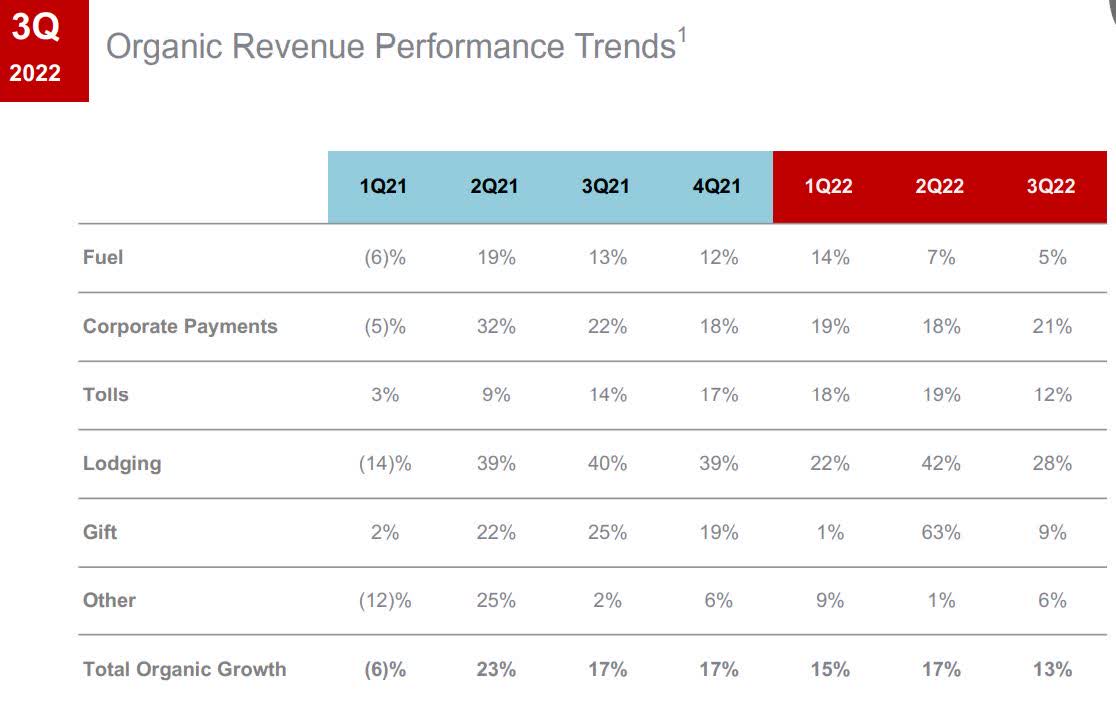

In the third quarter of 2022 FLT generated organic revenue of 13 percent, led by Corporate Payments of $205.00 million, which was up 21 percent, and Lodging with $127.00 million in the quarter, an increase of 28 percent.

On the other hand, Tools generated organic revenue of $89.00 million, or 12 percent, while Fuel generated organic revenue of $321.00 million, or 5 percent, in the third quarter of 2022.

Investor Presentation

As for preliminary guidance for 2023, management guided for organic revenue to grow 10 percent for the full year. That projection came from initial budget submissions for 2023.

I was actually very surprised by that low number for full-year 2023, and read it a few times to make sure I wasn’t getting it wrong. But either management misspoke or this is going to have a significant impact on the performance of the company in 2023, when considering organic revenue growth for the third quarter of 2022 alone was 13 percent.

Assuming 10 percent organic revenue growth is accurate, it would mean budget submissions are far lower than they have been for some time. It also points to expectations of a rough economic ride in 2023.

Based upon customer submissions at this time, the biggest hit the company looks to take in 2023 in regard to organic revenue growth is in its Lodging segment, which was up 28 percent in the third quarter of 2022, and is projected to grow in the mid-teens for 2023. Its remaining segments are projected to be flat or slightly down.

Investor Presentation

No matter how resilient FLT may be to a recession, it’s going to take a hit if this is how it plays out.

Balance sheet and liquidity

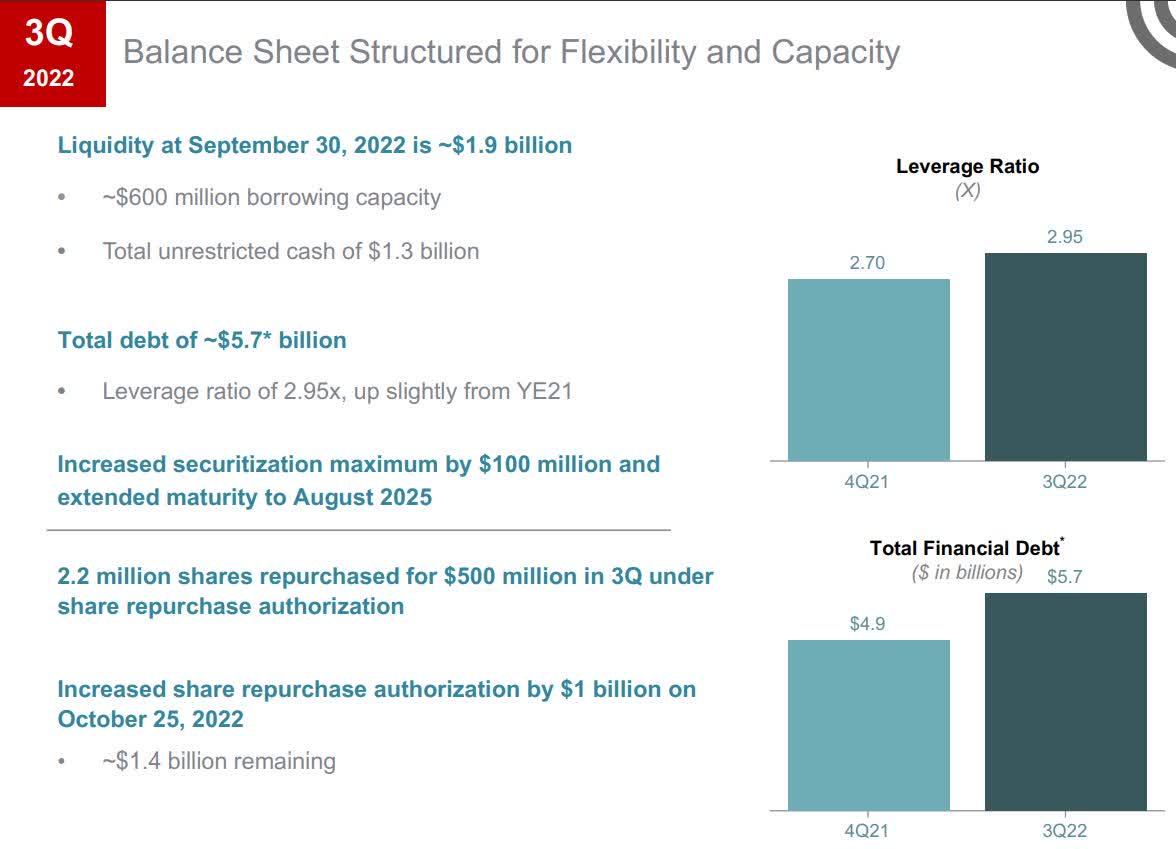

At the end of the third quarter of 2022 the company had cash and cash equivalents of $1.3 billion, compared to cash and cash equivalents of $1.52 billion at the end of calendar 2021.

It had an additional $600 million in borrowing capacity, bringing its total liquidity to $1.9 billion.

At the end of the reporting period the company held $5.7 billion in debt, with a leverage ratio of 2.95x.

It also boosted its securitization maximum by $100 million and extended maturity to August 2025.

Investor Presentation

With the company generating $321 million in free cash flow in the quarter, it should still remain fairly strong, even though that is probably going to come down some in the quarters ahead. When combined with its liquidity, it should be more than enough to take it through tough economic times, if that’s how 2023 plays out.

Conclusion

Based upon the numbers, company guidance, and the strong probability of a recession in 2023, I think FLT is going to struggle over the next year or so and will not be able to sustainably break through the $200.00 ceiling it struggled to break through during 2022.

That will come from the significant decline in organic revenue, increasing bad debt expense, and the decision by top management to rein in spending during 2023. With many new customers accounting for a large part of bad debt, according to management, it appears it’s going to be somewhat of an up-and-down year for FLX, with it moving more to the downside.

While its geographic diversity and numerous verticals it competes in will help mitigate some of the impact of a weak economy and slowing growth, it won’t be enough to support the stock as it has since the middle of October 2022.

For these reasons, I see the share price of FLT being under pressure throughout 2023 until the economy shows signs of recovery and interest rates top off.

Be the first to comment