Three Spots/iStock via Getty Images

Five9, Inc. (NASDAQ:FIVN) is one of the leading providers of cloud software for contact centers, which are used by customers in a wide range of industries, including financial services, healthcare, and retail. FIVN’s customer base includes businesses of all sizes, from small and medium-sized businesses to large enterprises. Actually, according to management, they continue to attract new large enterprise customers, with 134 large enterprise customers as of this writing, accounting for 86% of total revenue. FIVN remains aggressive in acquiring new talents and expanding their international footprint; in fact, they opened a new engineering hub in Portugal. However, as its human resource base expands, it will put pressure on its operating margins, making FIVN unattractive in the short term. In fact, FIVN’s GAAP earnings per share continue to be in negative territory, falling from -$0.30 in Q3’21 to -$0.33 in Q3’22. In addition, even when considering the adjusted gross margin, we can observe a declining trend that raises questions about the excessive growth of its stock-based compensation expenditure. This made FIVN unappealing, especially given its higher multiples in comparison to its peers.

Company Overview

As previously stated, FIVN continues to attract large enterprise customers who pay an annualized recurring revenue of more than $1 million. A huge driver of this success is their innovations, which allow the company to meet the demands of the growing Contact Center Software Market. In fact, FIVN offers new platform enhancements that strengthen digital self-service capabilities and new AI-powered automation tools that seek to further improve the customer experience. Additionally, FIVN continues to win recognition as Innovation and Growth Leader. Furthermore, despite the weak US dollar as of this writing, FIVN was able to retain a high dollar-based retention rate of 118%, which is a good catalyst for the company’s ability to continue expanding its revenue even in today’s challenging economic environment. In fact, management projected $2.4 billion in total revenue in 2027, with a dollar base retention rate of more than 120%. This translated to a growing total revenue of $198.3 million, up 28.52% from $154.3 million in Q3’21. However, this top-line growth did not translate well into declining adjusted gross margins, as illustrated in the image below.

FIVN: Declining Adjusted Gross Margin (Source: Company Filings. Prepared by the Author)

This is concerning since, despite its rising stock-based compensation expenditure, FIVN produces a slower adjusted gross margin of 61.4%, down from 64.1%. Additionally, the management’s earnings per share outlook for FY’22 is $1.36 on a midpoint basis, up 17.2% from $1.16 in FY’21, implying slower growth than the company’s three-year average of 24.9%. This slowing growth renders the company unattractive, especially given its high multiples.

FIVN: Trading At A High Multiples

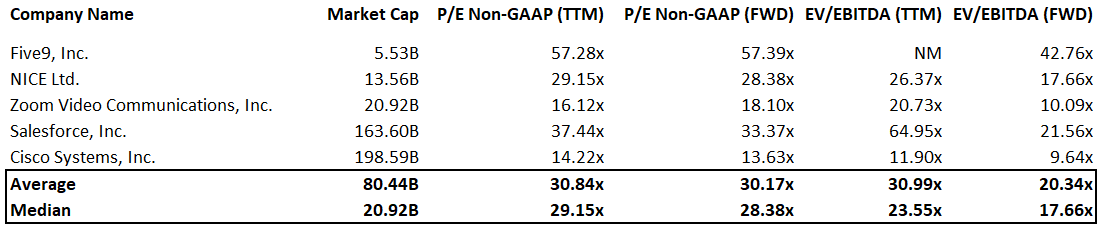

FIVN: Relative Valuation (Source: Data from SeekingAlpha. Prepared by the Author)

NICE Ltd.(NASDAQ:NICE), Zoom Video Communications, Inc. (NASDAQ:ZM), Salesforce, Inc. (NYSE:CRM), Cisco Systems, Inc. (NASDAQ:CSCO)

Following continued price cuts, it is unsurprising that FIVN currently trades at lower multiples than its 5-year average. In fact, FIVN currently trades at a trailing P/E ratio of 57.28x, compared to a 5-year P/E ratio of 113.35x. However, when we compare FIVN to its peers, we can see that FIVN trades at a premium. Especially given the company’s forward P/E ratio of 57.39x, which is higher than the peers’ average of 30.17x. Additionally, the company remains expensive when looking at its forward EV/EBITDA multiple of 42.76x vs. its peers’ average of 20.34x. As a result, I expect FIVN will stay under pressure in the short-term owing to its high valuation multiples.

Brewing An Attractive Correction

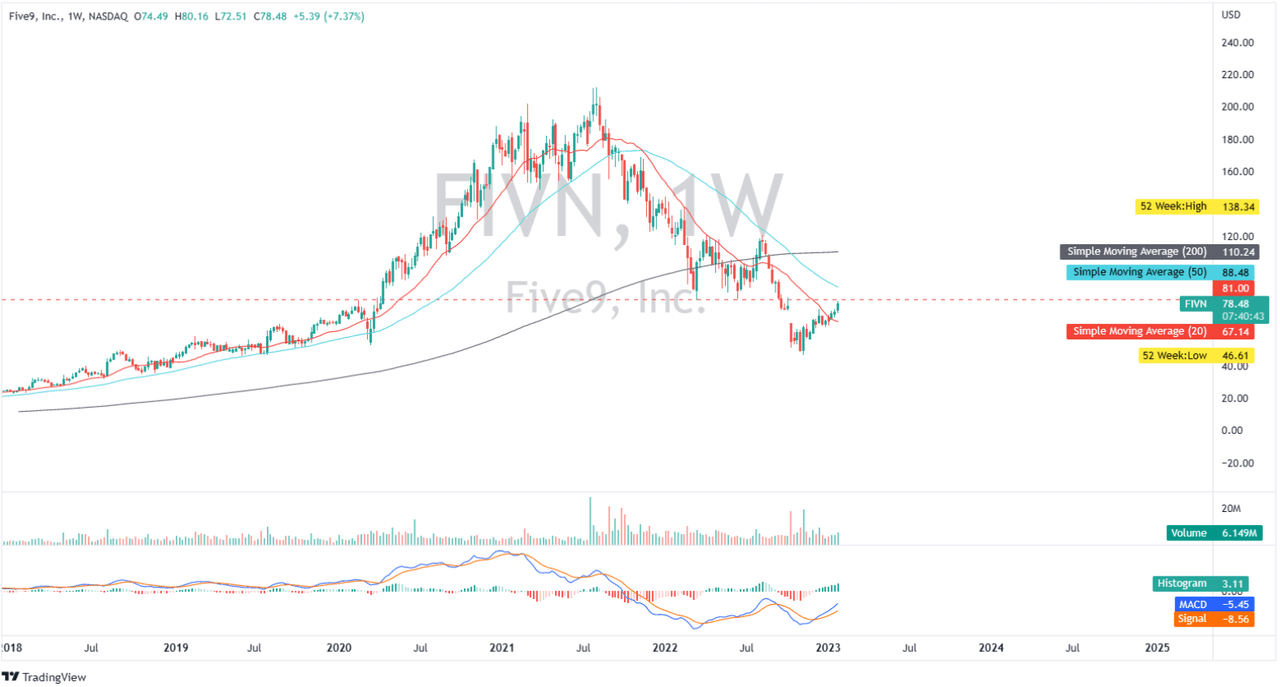

FIVN: Weekly Chart (Source: Author’s TradingView Account)

Source: Author’s TradingView Account

FIVN: Weekly Chart

As shown in the chart above, FIVN trades near its psychological resistance zone. Furthermore, FIVN is trading below its 200- and 50-day simple moving averages, indicating significant negative momentum. In fact, price is being driven higher by the bulls, with its MACD crossing above its Signal line. However, without a strong growth catalyst, this rally appears unsustainable. As a result, I would like to get FIVN at its immediate support level of $60, which would improve its risk/reward ratio over today’s level.

Caveat

Nevertheless, considering management’s long-term objective of $2.4 billion in total revenue in 2027 and a target of 23% adjusted EBITDA margin, which equates to 9.6x forward EV/EBITDA in FY’27. Today’s potential drop appears to be an excellent time to begin accumulating. But because of today’s economic uncertainty and headwinds, I think it’s best to wait for a better price or let the price retest its previous support level at $50.

Final Key Takeaways

In addition to the slower Y/Y growth rate predicted for FY’22, management anticipates a snowball effect in FY’23. In fact, management has projected a 16% YoY increase or $900 million in sales for FY’23 only, which is below the anticipated 27.16% YoY growth for FY’22. According to the management this is due to temporary headwinds, as quoted below.

…we may see a drop in the LTM enterprise subscription revenue growth rate from 37% we achieved in the third quarter into the high 20s due to the macroeconomic challenges. Source: Q3’22 Earnings Call Transcript

This negative growth catalyst snowballed into its earnings per share outlook, which remains below its FY’22 YoY growth of 17.2% as quoted below.

…In terms of the bottom line, we expect 2023 non-GAAP net income per share to increase at a similar rate to the 16% revenue growth outlook and increase year-over-year from the midpoint of our 2020 guidance, at a $1.36 to $1.78 in 2023. Source: Q3’22 Earnings Call Transcript

FIVN completed the quarter with a positive trailing free cash flow margin of 0.6%, compared to a negative margin of -2.2% in FY21. In addition, the company has $129.5 million in cash and cash equivalents and $447.6 million in short-term investments, the majority of which are low-risk investments, with no substantial debt maturing until 2025. To conclude, FIVN remains a relevant player in the industry, but potential weaknesses in its profitability make the firm unappealing at these levels.

Thanks for reading and good luck!

Be the first to comment