Morsa Images

Thesis

First Advantage Corp. (NASDAQ:FA) is a leading global provider of background screening services, competing head-on with other firms such as Sterling Check Corp. (STER) and HireRight Holdings Corporation (HRT). I like the market for background screening and believe there is room for multiple winners, including FA. FA also has the highest margins, lowest leverage, and the only active share repurchase program amongst the three publicly traded companies. However, I remain cautious on the current macro backdrop and believe there could have been some pull-forward in FA’s growth following the significant outperformance in organic growth over the past few years. I could become more constructive on the shares in the event of multiple beat and raise performances and/or management finding a transformational M&A deal to help turbocharge growth.

Focusing On Verticals That Have Held Up Well During The Pandemic

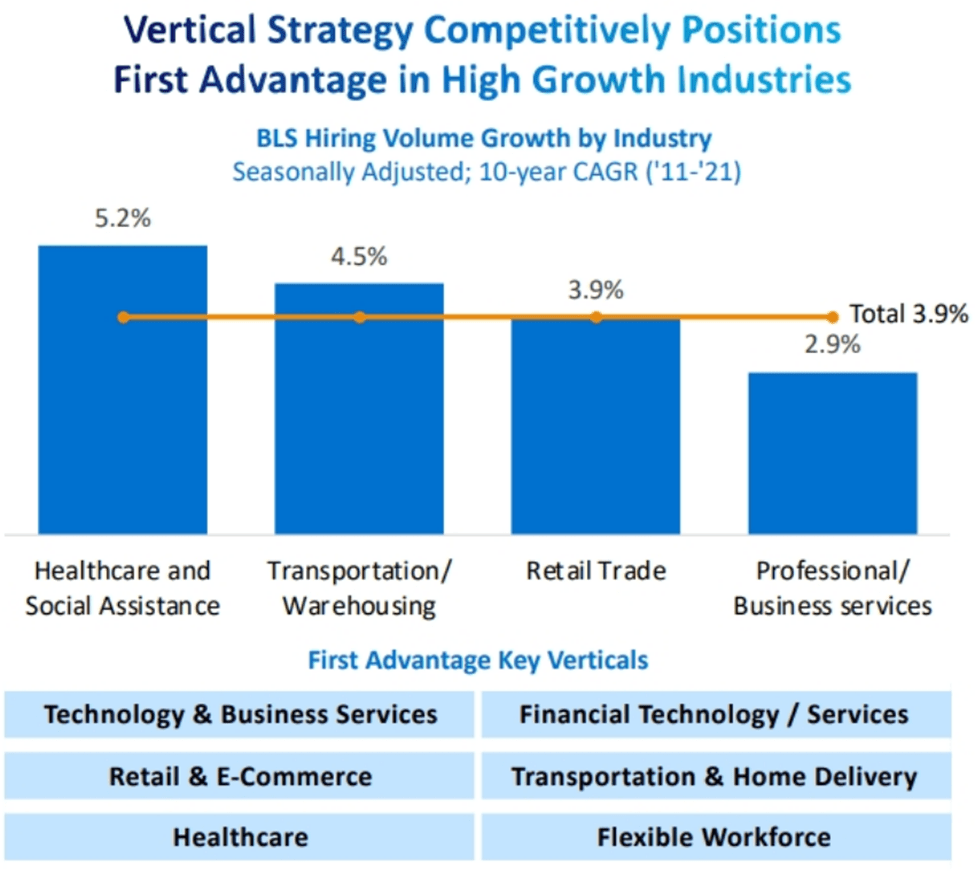

FA provides background screening services, with offerings that include criminal records screening, drug and alcohol screening, resident screening, and tax credit and incentive screening/compliance services. I view the TAM for background screening as large, with the company estimating the current TAM at $13 billion, which implies that FA commands a 6.5% market share based on FY22 revenue estimate. FA specifically focuses on verticals such as technology and business services, retail/e-commerce, and transportation/home delivery. I believe this helped FA navigate the early impacts of the Covid-19 pandemic better than Sterling Check Corp. or HireRight Holdings Corporation. Of note, FA was able to post 5.7% growth in FY20, whereas both HRT and STER reported a drop in revenue as customers in their focus verticals experienced significant disruption in the labor market.

FA has focused on high-growth verticals (Company Presentation)

Investments In Automation/Digitization Leading To Premium Margins

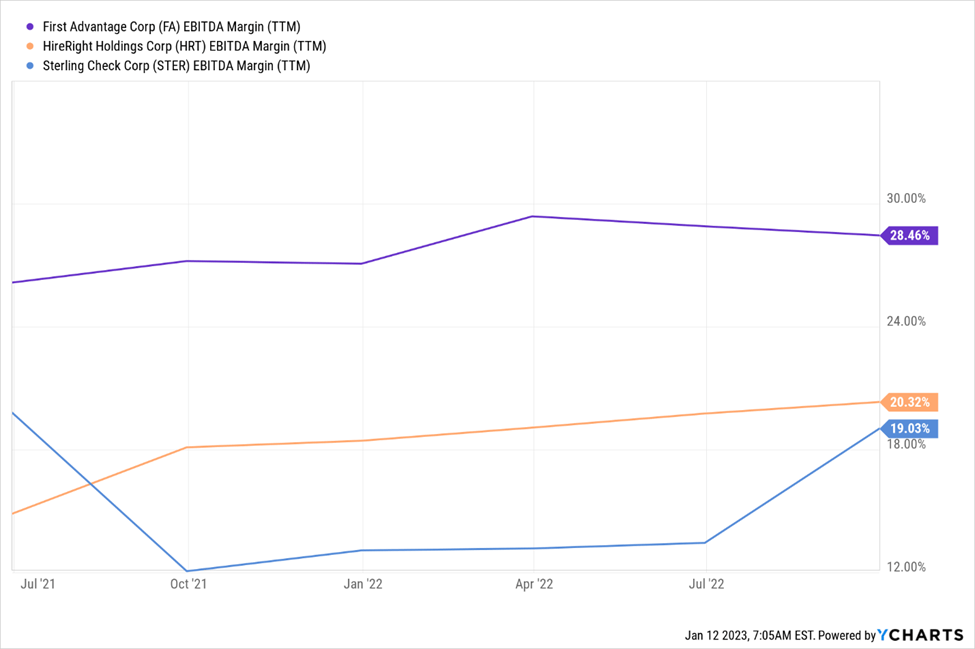

FA has historically generated substantially better EBITDA margins vs its peers HRT and STER. I believe that FA generates its industry-leading margin by prioritizing automation/digitization, which helps improve operating efficiency while also resulting in quick turnaround times for clients. In addition, I believe that FA’s investments in proprietary data, including building a National Criminal Database by compiling court records and other public documents, helps further improve efficiency and save on third-party data costs.

Although FA has the highest margins in the background screening space, I have modeled a decline in the EBITDA margin in FY22 as FA absorbs the impact of recent lower-margin acquisitions, invests in technology, and incurs higher third-party data costs. While I expect margin expansion in FY23, I will be keeping a close eye on expenses in the coming quarters, especially in a high-inflation environment.

FA’s EBITDA Margins vs. Peers (YCharts)

Relatively Low Financial Leverage as compared with Peers

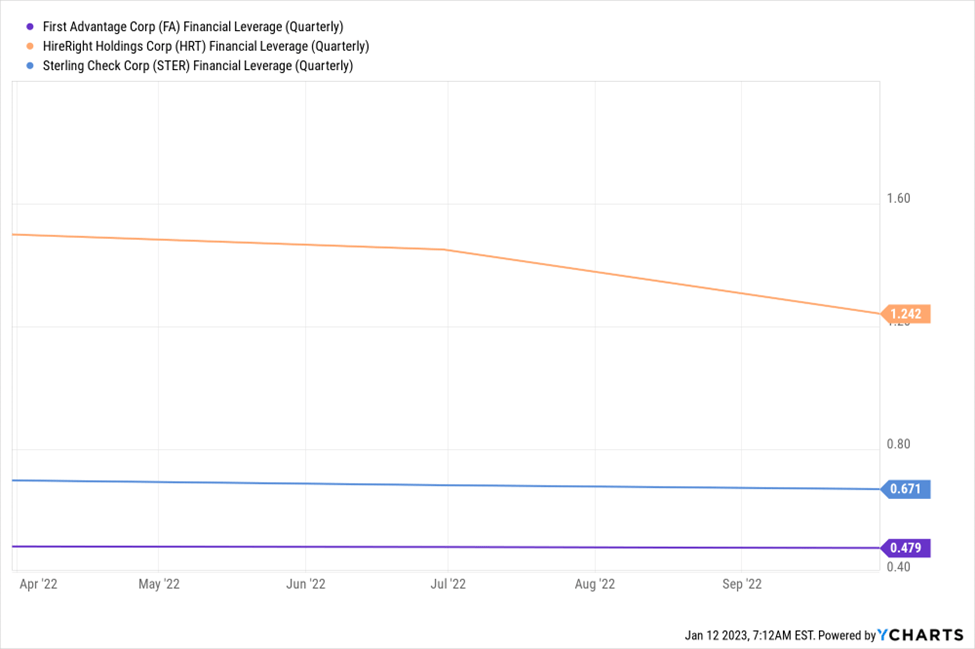

As of 9/30/22, FA had $390.3 million in cash and cash equivalents and $556.2 million in debt under a credit facility that matures on January 31, 2027. In addition, FA has $100 million of capacity available on a revolving credit facility, providing the company with ample liquidity and no looming debt maturities.

FA’s net financial leverage currently stands at just 0.47x, below both HRT (1.24x) and STER (0.67x). Given the low leverage relative to peers, I believe that FA has the flexibility to add leverage to the balance sheet to pursue accretive M&A that could turbocharge growth.

FA’s Financial Leverage vs. Peers (YCharts)

Financial Outlook

Top Line

Most of FA’s relationships with customers are contract-based, and the term length is typically three years. Given that the revenue is transactional, FA’s services have a defined price to identify the value of the relationship. Clients are billed on a monthly basis, and revenue is recognized upon completion.

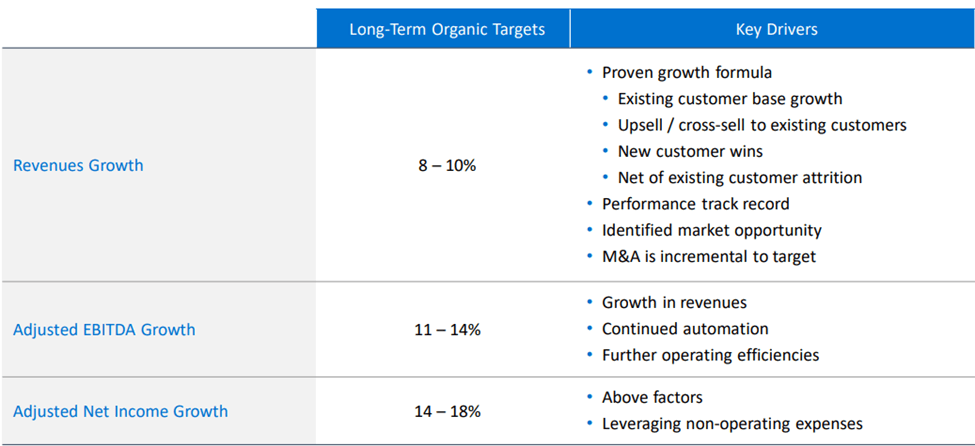

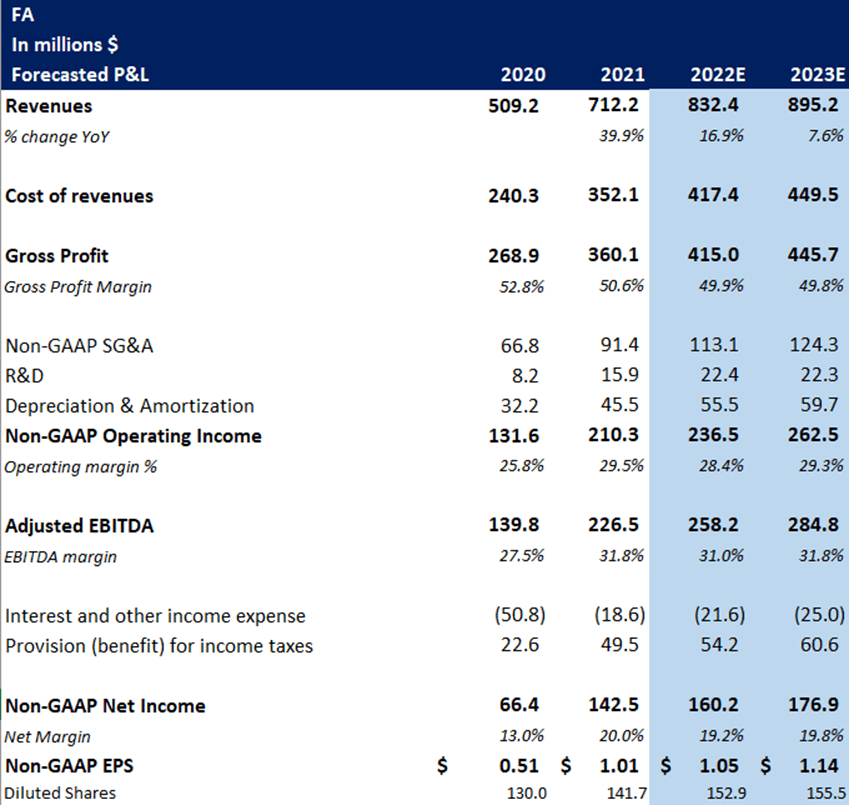

FA’s revenue has grown steadily since FY19, and even during the pandemic-impacted FY20, through a combination of organic efforts and M&A. FA derives the majority of its revenue from pre-onboarding screening services, which are largely tied to hiring volume/job turnover. While FA offers services in over 200 countries, the United States accounts for the majority of revenue. In FY21, coming out of the pandemic, the majority of growth was driven by existing customers due to the broad recovery in demand for screening services that was pressured during the onset of the pandemic. In addition, the acquisitions FA made in FY21, acquiring Corporate Screening Services and MultiLatin Advisors contributed ~$25 million in revenue in the year, resulting in nearly 40% revenue growth in FY21. While I expect LT growth to moderate to a high single-digit range, I am modeling 16.9% revenue growth in FY22 due to strong organic growth, a full year’s contribution from the FY21 acquisitions, and 2022’s acquisition of Form I-9 Compliance. In FY23, I expect FA to return to a more normalized, LT growth rate as the recent acquisitions lap in and prior year comparables normalize. I am modeling 7.6% revenue growth in FY23, and expect organic growth to be driven by a combination of new logo wins, cross/up-sell efforts, and growth with the existing user base.

FA’s long-term targets (Company Presentation)

Margins

FA has executed well on driving steady and consistent margin expansion, which primarily comes from investments in increased automation and deployment of robotic process automation (RPA) technologies that are designed to improve speed, efficiency, and quality. By leveraging RPA processes, FA can conduct quick turnaround times, leading to 90% of criminal searches in the US conducted by FA being completed within one day. While I expect FA’s EBITDA margin to remain healthy, I have forecasted a contraction of 80 bps in FY22 as incremental public company costs are absorbed, and management invests in technology efficiencies and its sales strategy. In addition, higher third-party data costs are expected to pressure margins, though these costs are fully passed on to clients. I expect 80 bps of margin expansion in FY23 as the impact of higher third-party data costs normalize and the business continues to scale.

FA’s forecasted P&L (my estimates)

Cautious Macro Signals And A Slowdown In Growth Demands A More Conservative Rating

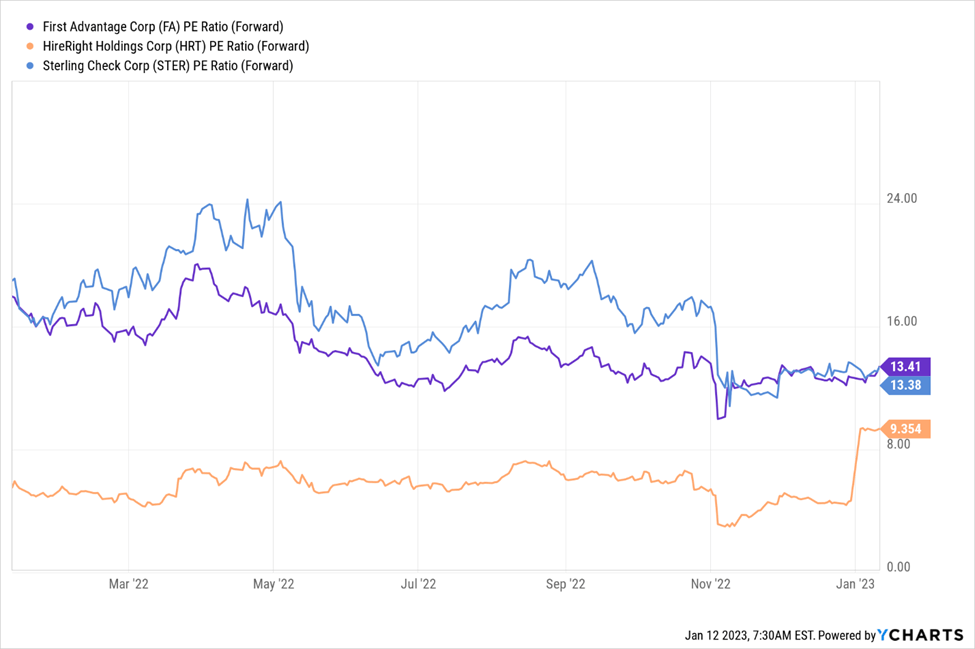

FA trades at a P/E multiple of 13.4x of FY23 estimate, a premium to HRT (9.3x), and at par to STER (13.4x). While I remain positive on FA’s business strategy and the background screening space as a whole, I am more cautious about the macro-outlook given the increasingly mixed economic data and increasing fears of a recession. I believe a recession would eventually impact the labor market, which could put pressure on FA’s growth.

In addition to the hesitancy on the macro-outlook, I believe that some growth could have been “pulled forward” in FY20, partially due to FA’s focus on verticals such as home delivery, e-commerce, and flexible workforce workers, all areas that thrived during the pandemic. Of note, FA was the only publicly traded background screener that grew during FY20, and while that is commendable, and I believe it could have pulled forward some growth. I could become more constructive on the shares in the event of the company reporting additional beat and raise quarters, which would increase my confidence that the impressive results since going public are sustainable. In addition, I believe that a transformational acquisition, especially in an international market, could help turbocharge growth and make the shares more compelling despite the uncertain macro backdrop.

FA’s forward P/E ratio vs. Peers (YCharts)

Final Thoughts

I view FA as a company that is well-positioned to thrive as a global provider of background screening services, a quickly growing and attractive space that I believe has room for multiple winners. While I am positive on FA’s long-term prospects, I believe that increased macro pressure/recessionary fears could result in a more challenging operating environment in the next several quarters, especially if job hiring/turnover slows. Given these dynamics, I keep a Neutral rating on the stock with no price target. I could become more constructive on the shares in the event of continued strong organic growth despite a choppy macro backdrop and/or a transformative acquisition that would help FA entrench itself as the largest global player in the space.

Be the first to comment