dpproductions

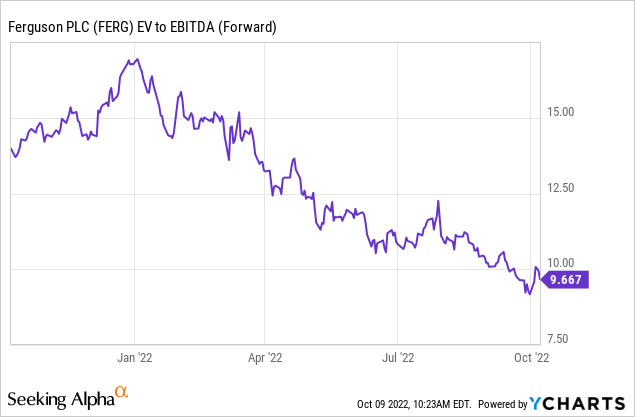

Having rebased the guidance post-results to account for a macro slowdown, I see little downside risk to current consensus estimates for Ferguson (NYSE:FERG). Instead, I maintain the view that distributors with pricing power and defensible margins like Ferguson will outperform in an inflationary environment. With global supply chain constraints not easing as quickly as initially anticipated, Ferguson’s balance sheet strength should allow it to accelerate industry consolidation; in effect, the company is well-positioned to gain market share from smaller players and better pass-through inflation to customers. Ferguson’s revenue diversification is also a major asset, as its balanced residential/ non-residential portfolio allows for top-line resilience through the cycles. Along with the incremental contribution from bolt-on acquisitions and share repurchases, I see the low-teens earnings growth target as well-supported over the medium term. At current valuations, Ferguson shares trade at 9-10x EV/EBITDA, a discount to its historical average, despite a near-term US index inclusion catalyst.

Q4 ‘22/Fiscal 2022 in Review

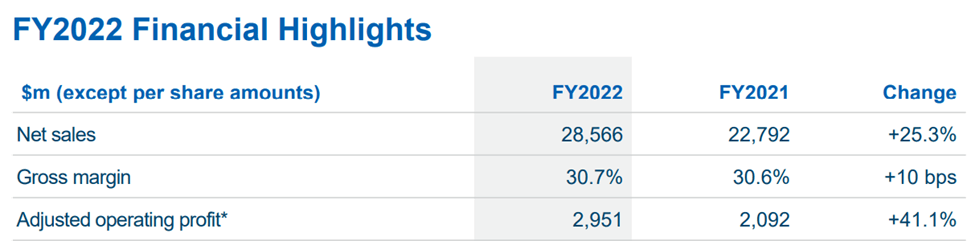

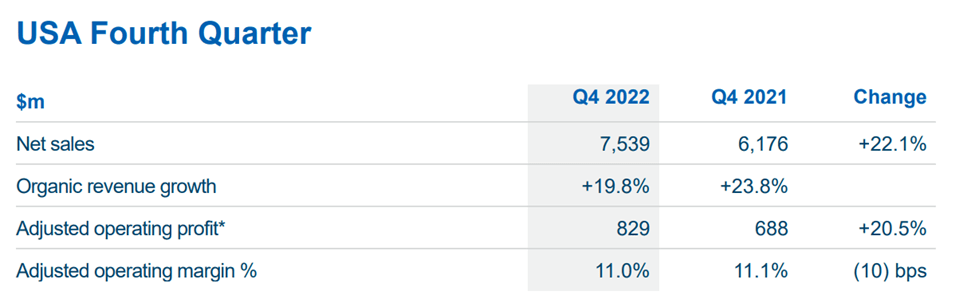

Ferguson’s fiscal 2022 results were strong across the board, led by reported revenue growth of +25% and adjusted operating profit growth of +41% at a 10.3% margin. The key fiscal 2022 outperformer was the US, where organic growth reached +20%, with another c. 2% contribution from M&A. Also helping the full year strength was the Q4 ’22 margin performance at 10.7%, along with an impressive +19.5% organic growth (comprising US growth of c. 20% and Canada at c. 14%).

Ferguson

By region, the US was again the highlight in Q4, as residential end markets remained surprisingly robust despite the Fed rate hikes. While signs of a slowdown are emerging in new residential housing starts and permits, Ferguson’s renovation maintenance improvement (RMI) activity outweighed any negative impact. Organic growth of +14% in Canada may seem comparatively slow, but I would note the result included a c. 4% negative currency impact, clouding the underlying residential/non-residential growth. Overall, the solid operating metrics across the portfolio, with residential revenue up a solid c. 17% in Q4 and non-residential revenue also up c. 28%, should give investors plenty of confidence heading into the upcoming fiscal year.

Ferguson

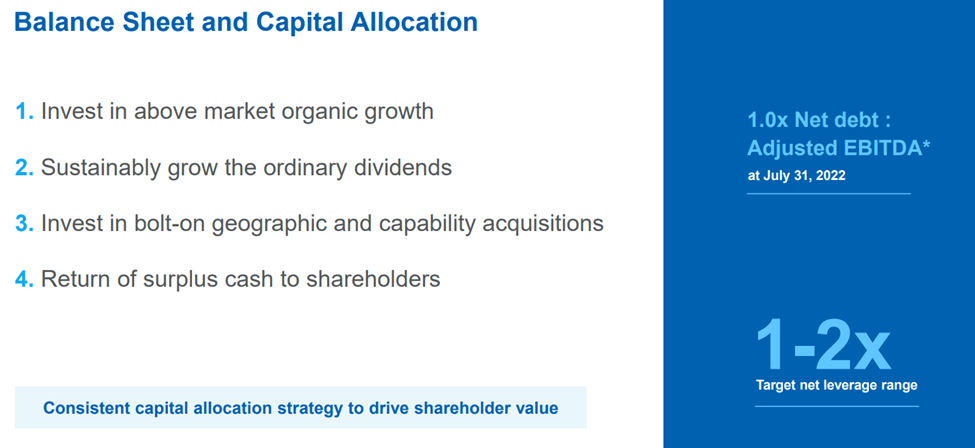

Ferguson has also managed its balance sheet well through the cycles, with leverage of c. 1x net debt/ EBITDA well within the 1-2x target range. This offers the company plenty of room to deploy capital into accretive opportunities ahead. Thus far, management has opted for repurchases, completing c. $1.5 billion of share repurchase (out of the original $2 billion allocation). The latest extension of the repurchase program by c. $0.5 billion, expected to be deployed within the next twelve months, further highlights the undervaluation of the shares. Alongside the repurchases, Ferguson’s move to a quarterly interim dividend schedule in fiscal 2023 (first dividend expected at the Q1 ‘23 results) will be well-received by investors.

Ferguson

Positive Fiscal 2023 Guidance

Looking ahead to fiscal 2023, Ferguson expects low single digits % net sales growth and an adjusted operating margin range of 9.3% to 9.9%. Alongside moderating starts, RMI activity is also projected to soften despite the company’s focus on high-end consumers who tend to be less price sensitive. The moderation in growth and margins tallies with management commentary that the flat volumes it saw toward the end of Q4 ’22 will turn negative as we move through the fiscal year. In Q1 to-date, however, revenue growth has been surprisingly resilient in the mid-teens % despite some tough Y/Y comps. Considering Ferguson’s track record of delivering consistent GDP plus organic growth over the last decade, this is unsurprising to me, reflecting the benefits of the company’s balanced portfolio.

Moderating inflation could also drive an upside surprise to the margin guidance. Ferguson is already seeing supply chains normalizing and expects to work through elevated inventory levels throughout the fiscal year. Assuming management also delivers on the execution front, I expect pricing to be relatively stable Y/Y as inflation eases across the portfolio.

Aside from the Ferguson base case for a conservative low-single-digit % decline across its underlying end-markets and 3-4% pts of outperformance, M&A is also expected to play a role, with management guiding for an additional c. 2% impact from the integration of closed acquisitions. To recap, in Q4 ’22 alone, the company completed an impressive seven acquisitions, adding c.$470 million of annualized revenues. Considering the healthy pipeline of deals and the strong balance sheet position, Ferguson is especially well-positioned to continue consolidating the industry through the upcoming downcycle. Longer-term, the non-residential construction pipeline of projects also offers the company exposure to growth themes like on shoring, EV, and battery storage, while upcoming US fiscal infrastructure plans offer good near-term support.

Final Take

Ferguson shares have faltered this year, largely due to a compression in the valuation multiple, which I view as unfair following another in-line quarter and considering the management team’s typically conservative guidance. Admittedly, supply chain constraints and inflationary conditions are headwinds, but distributors with strong balance sheets like Ferguson should outperform. The company has already demonstrated its pricing power by successfully passing on inflation to customers, while its ability to acquire during the downcycle accelerates its market share gains. Ferguson’s resilience is down to its balanced resi/non-resi portfolio mix which, combined with M&A and share repurchases, underpins a low-teens growth algorithm over the medium to longer-term. With the latest 10-K filing also granting Ferguson shares eligibility for US indices, I continue to see plenty of upside ahead.

Be the first to comment