mattabbe

The Federal Reserve has entered a period of tighter monetary policy to combat the inflation in the economy that reached a forty-year high of 9.1 percent in June.

The Dow-Jones Industrial Average rose 658 points on Friday. The Standard & Poor’s 500 Stock Index increased by 73 points on Friday. The NASDAQ index jumped 201 points on Friday.

So much for monetary tightening? Oh, all three indexes suffered weekly losses.

Here is the weekly chart of the Dow-Jones

Dow-Jones Industrial Average-Last Week (Federal Reserve)

Caitlin Ostroff and Justin Baer write in the Wall Street Journal

“U.S. stocks rebounded Friday, capping a volatile week during which investors tried to reconcile a flurry of corporate-earnings reports and data that at times appeared to offer conflicting narratives on the economic outlook.”

The background:

“Major indexes rallied to end the week on a fresh round of bank earnings and data showing retail sales had climbed more than expected in June. They tumbled earlier on a new reading showing inflation at yet another four-decade high and as some of the biggest banks posted disappointing quarterly results.”

In other words, investors are getting conflicting information and this conflicting information is resulting in more volatile market movements.

The Two Pictures

The conflict seems to lie in the two narratives that investors appear to be dealing with. These two stories are not new and are modifications of what investors were thinking when the discussion was about whether or not inflation was a problem that the Federal Reserve was dealing with.

At that time, there were a group of investors – and policymakers – that believed any inflation problem on the horizon was only going to be very short-lived and as a consequence, the Federal Reserve was not going to really have a problem on its hands and could get by without really tightening up on monetary policy to any degree.

The alternative viewpoint was that inflation was going to be more of a severe problem, something that the Federal Reserve was really going to have to battle.

The last narrative turned out to be closer to the truth and the Federal Reserve has really had to enter the fray.

Currently, the narratives are very similar only both pictures have the Federal Reserve tightening up on monetary policy.

The first picture is one captured in the Wall Street Journal article cited above. Brad McMillan, chief investment officer at Commonwealth Financial Network, claims that: “We are in a bottoming process.”

The period of economic slowdown is bottoming out and we will soon return to a more expansive growth period.

To Mr. McMillan, stock prices are now more closely aligned to projected earnings and many investors are already accounting for the effects of rising interest rates.

As I have mentioned in earlier articles posted this past week, the bond markets have five-year and ten-year inflationary expectations that are built into government bond yields that show only relatively modest gains in inflation in the near term and five-year inflationary expectations are lying below ten-year inflationary expectations meaning that investors appear to believe that actual inflation will only be relatively short-lived and brought under control in the relatively near term.

That is, inflation is going to peak soon and get back to the level of the Federal Reserve’s target for inflation.

The other view is that inflation will not be so short-lived and will turn out to be much higher, over time, than a lot of people now think will be the case.

Like in the earlier situation, the investors that believe that the current situation will only be very short-term in nature and that inflation will quickly come back under control seem to me to be overly optimistic.

The likelihood that inflationary pressures will be stronger and last longer fit my picture of the future more closely.

I think the market is pricing in too fast of a recovery of stable prices than is warranted. To me, the battle is going to be tougher than that.

The Future

Mike Bell, global market strategist at JPMorgan Asset Management, is quoted in the Wall Street Journal, as taking the second view mentioned above. “Recession risks have risen since the beginning of the year.”

If we don’t get any signal of consumer retrenchment, maybe it’s not as bad as people fear, but if we do get that, it’s a signal recession risk is materializing.

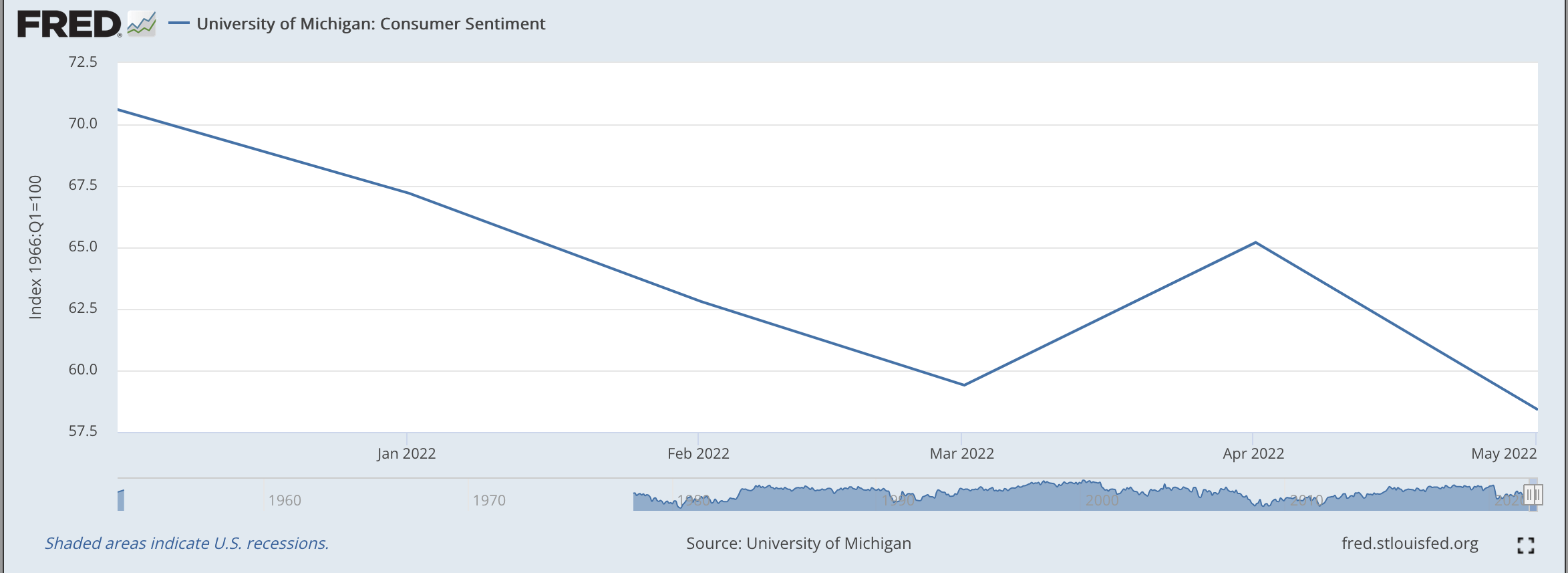

This latter scenario is the one I believe will hold. The University of Michigan consumer sentiment index for July 2022 was 51.1. Although this is above the June figure of 50.0, the index is hovering around its all-time low.

University of Michigan Consumer Price Sentiment (Federal Reserve)

My feeling is that this index is going to come in lower in August and as we enter into the fall.

If I am correct, this just adds to the possibility that the recession is going to be worse than what the “optimistic” set believes.

We must keep an eye on this scenario.

The Picture

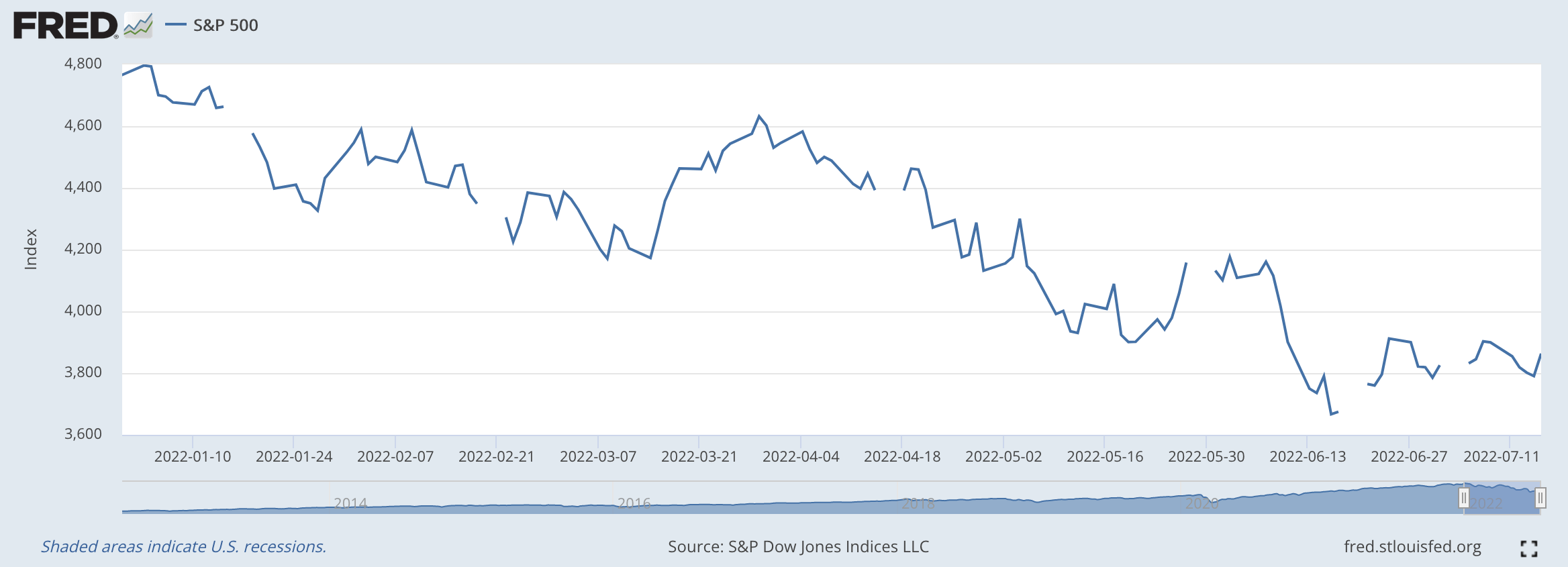

The Standard & Poor’s 500 Stock Index has been declining since January 3, 2022. Here is what the trend looks like.

Standard & Poor’s 500 Stock Index (Federal Reserve)

By January 2022, investors in the stock market realized that the Federal Reserve was serious in its plan to begin to tighten up on monetary policy and start to raise its policy rate of interest, and to begin reducing the size of its securities portfolio.

Federal Reserve officials had gotten over their attachment to the earlier narrative about the quick demise of inflation and had committed to going into battle against the inflationary pressures in the economy.

But, when the Fed officials finally convinced investors that they were really going to fight inflation, stock market prices peaked and began to decline.

That is the chart we have just above.

Now, as described above, many investors still seem to believe that “we are in a bottoming process.”

And, these beliefs are behind the market statistics we see today.

I believe, just as in the earlier case, that these optimists are wrong.

I believe that the inflationary pressures are stronger than these people imagine.

I believe that the fight against inflation will be harder and more extended than these people imagine.

Therefore, I believe that the chart of the Standard & Poor’s 500 stock index will continue to drop and the chart is extended out toward the right.

Be the first to comment