Khanchit Khirisutchalual

A Quick Take On Fathom Holdings

Fathom Holdings (NASDAQ:FTHM) went public in July 2020, raising $34 million in an IPO that priced its shares at $10.00.

The firm provides an online real estate brokerage and mortgage platform in the U.S.

With U.S. residential housing prices in decline and fewer sales negatively impacting the firm’s mortgage segment, my outlook for FTHM’s near term is not optimistic, especially since the firm doesn’t appear to be making significant headcount reductions.

Accordingly, my view on FTHM in the short term is on Hold.

Fathom Holdings Overview

Cary, North Carolina-based Fathom was founded to create an online platform for real estate agents to facilitate the buying and selling of real estate via the Internet.

Management is headed by founder, Chairman and CEO Joshua Harley, who was previously founder and CEO of Texas Home Central.

The company operates in 38 states and says that it is the 6th largest independent brokerage in the U.S.

The firm focuses on attracting real estate agents to its platform by effectively sharing more of the transaction commission with the agent and taking a flat fee per transaction.

FTHM also provides mortgage lending and processing services.

Market & Competition

According to a 2019 report by IBISWorld, the market for real estate sales & brokerage in the U.S. was expected to reach almost $167 billion in revenue in 2020.

This represented a forecast 1.4% increase from 2020. Assuming this, the industry will have grown an average of 3.3% per year from 2015 to 2020.

The main drivers for this expected growth are generally lower-than-average interest rates and a strong job market that provide property buyers with ample ability to afford new homes, especially among younger demographics such as Millennials who are buying homes for the first time.

The company cites three primary types of competitors to their services:

-

National independent real estate brokerages and franchises

-

Companies that seek to disrupt the traditional brokerage model

-

Companies that purchase homes directly from sellers

Fathom’s Recent Financial Performance

-

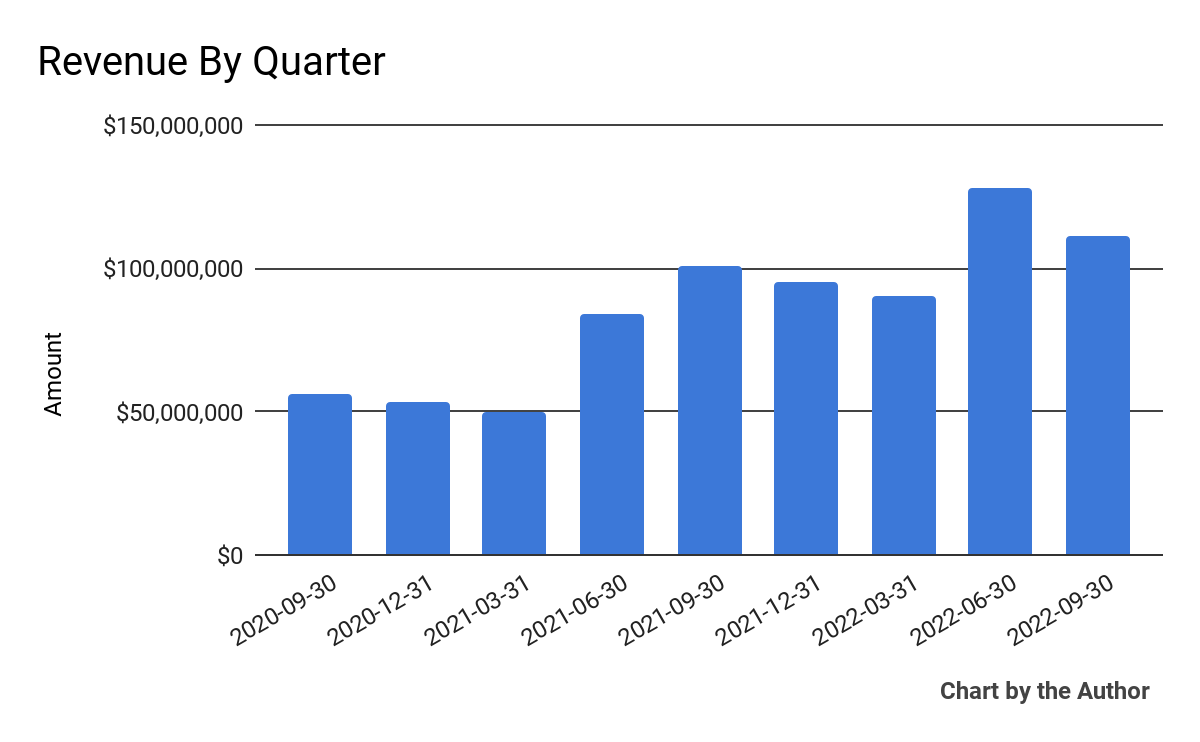

Total revenue by quarter has increased materially in recent quarters:

9 Quarter Total Revenue (Financial Modeling Prep)

-

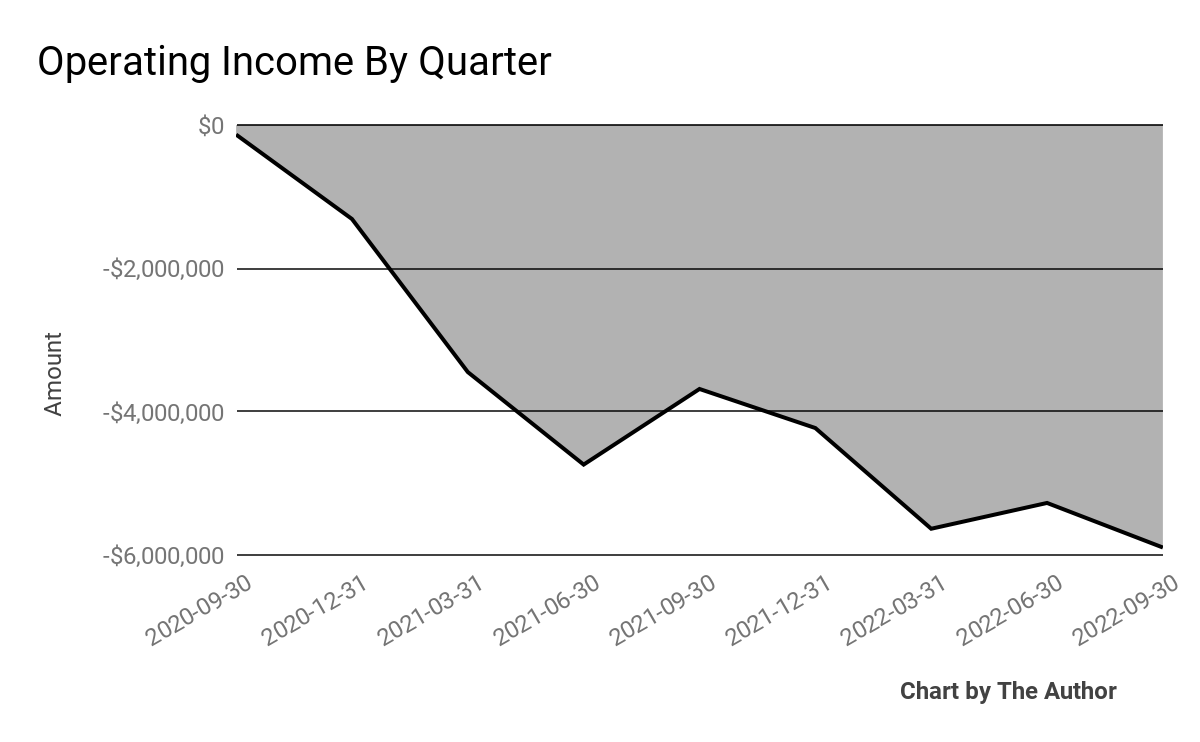

Operating losses by quarter have increased sharply recently:

9 Quarter Operating Income (Financial Modeling Prep)

-

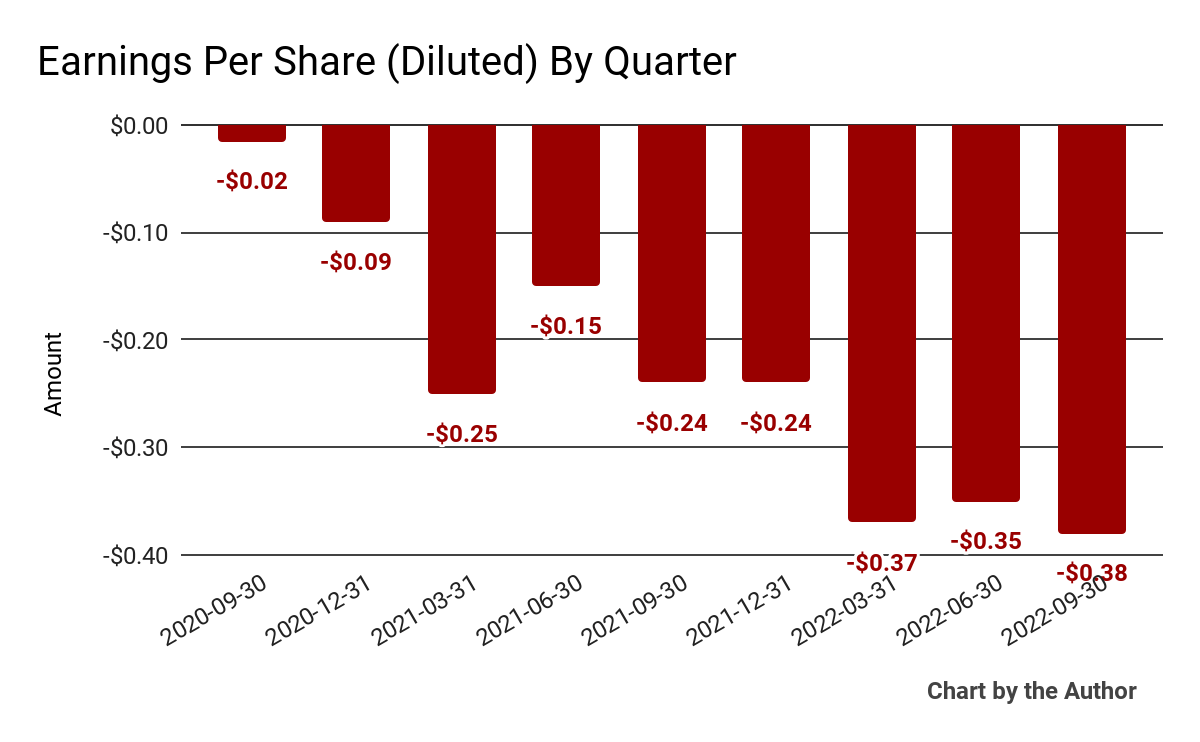

Earnings per share (Diluted) have worsened substantially in recent quarters:

9 Quarter Earnings Per Share (Financial Modeling Prep)

(All data in the above charts is GAAP)

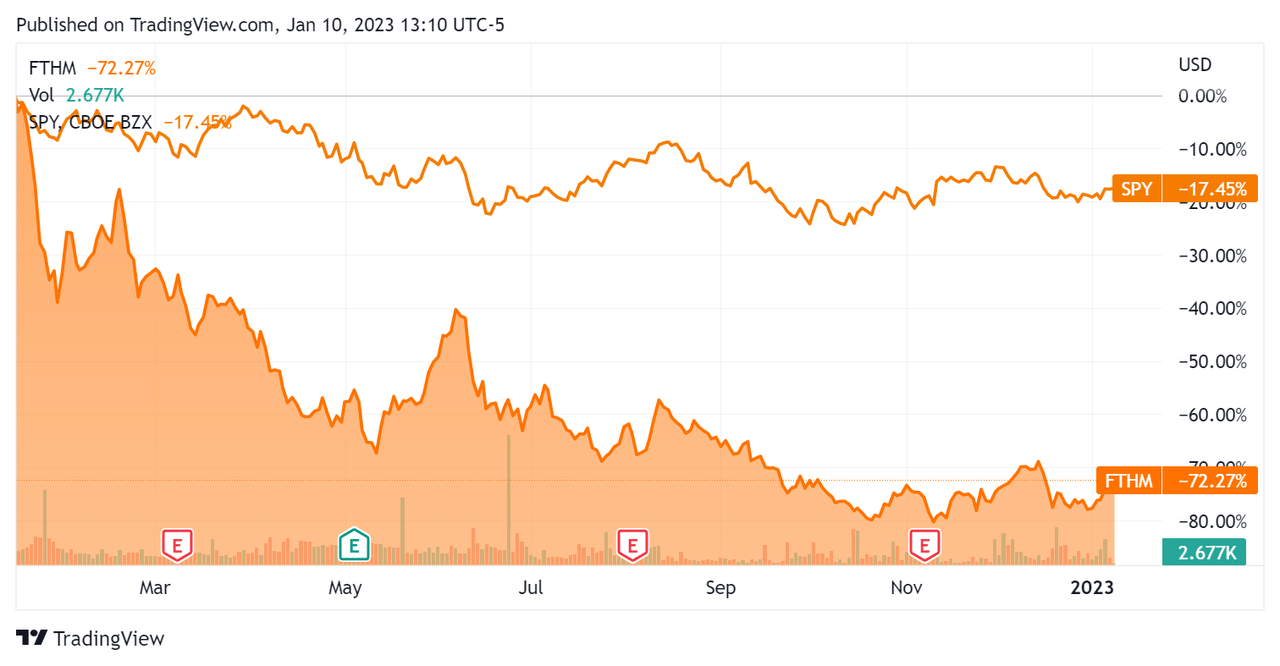

In the past 12 months, FTHM’s stock price has dropped 72.3% vs. the U.S. S&P 500 index’s drop of around 17.5%, as the chart below indicates:

52-Week Stock Price Comparison (Seeking Alpha)

Valuation And Other Metrics For Fathom

Below is a table of relevant capitalization and valuation figures for the company:

|

Measure [TTM] |

Amount |

|

Enterprise Value / Sales |

0.2 |

|

Enterprise Value / EBITDA |

-4.8 |

|

Revenue Growth Rate |

47.5% |

|

Net Income Margin |

-5.0% |

|

GAAP EBITDA % |

-4.2% |

|

Market Capitalization |

$90,324,632 |

|

Enterprise Value |

$85,328,567 |

|

Operating Cash Flow |

-$6,370,000 |

|

Earnings Per Share (Fully Diluted) |

-$1.34 |

(Source – Financial Modeling Prep)

Commentary On Fathom Holdings

In its last earnings call (Source – Seeking Alpha), covering Q3 2022’s results, management highlighted the firm’s growth to become what it claims is ‘the 10th largest brokerage in the country out of more than 86,000 brokerages and the sixth largest independent brokerage.’

Notably, the company’s Q3 agent count increased by 33% and transactions rose by 5%.

However, against the firm’s low-fee model, it announced a transaction fee increase effective January 1, 2023. In addition, the firm is increasing the annual cap on the number of sales for which the company charges a full fee.

As to its financial results, revenue rose 10% year-over-year, reaching $111.3 million.

Management said the company’s agent retention rate was ‘approximately twice the national average,’ and stated that it had an average 1.5% monthly attrition rate over the last 12 months.

However, operating losses worsened significantly, as did negative earnings per share, highlighting the need for the firm to increase its take rate and putting into question its ultra-low-cost approach.

For the balance sheet, FTHM finished the quarter with $14.8 million in cash, equivalents and trading asset securities and $9.3 million in debt. $8.5 million was classified as ‘short-term borrowings.’

Over the trailing twelve months, free cash used was $12.9 million, of which capital expenditures accounted for $1.3 million. The company paid $7.6 million in stock-based compensation.

Looking ahead, management guided full-year 2022 revenue of $420 million at the midpoint of the range and adjusted EBITDA loss of $8.7 million at the midpoint. Adjusted EBITDA usually excludes stock-based compensation, which is running at $7.6 million annually.

Regarding valuation, the market is valuing FTHM at an EV/Sales multiple of 0.2x.

The primary risk to the company’s outlook is the increasingly poor U.S. real estate market as a result of rising interest rates and lower affordability.

A potential upside catalyst to the stock could include a pause in interest rate hikes, improving the firm’s valuation multiple and giving some needed relief to prospective borrowers.

With U.S. residential housing prices in decline and fewer sales negatively impacting the firm’s mortgage segment, my outlook for FTHM’s near term is not optimistic, especially since the firm doesn’t appear to be making significant headcount reductions.

Accordingly, my view on FTHM in the short term is on Hold.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment