Phiromya Intawongpan/E+ via Getty Images

Investment Thesis

Farfetch (NYSE:FTCH) had an Investors’ Day that can be summed up with one word: underwhelming. As Farfetch was about to wrap up 2022, with the stock already down more than 75% from its all-time highs, Farfetch asked investors to be a little more patient and to hold out to 2025.

For investors, during a period when the market is already particularly shaky, this was one demand too much.

That being said, I believe that investors may be too quick to disregard this investment opportunity. I will not argue that this investment is a low-risk high-reward opportunity. There’s in fact substantial risk.

But investors can invest with this insight in mind and appropriately weigh this position in their portfolios.

Investors’ Day? Oh, But I’m Not So Sure

In the interest of full disclosure, I’ve been bullish on this name for a long time, and so far I’ve been demonstrably wrong.

Also, further complicating the investment thesis, Farfetch had its Investors’ Day back on 1 December, and that event Farfetch drove its shareholder base out the door.

More specifically, Farfetch’s Investor Day saw its stock fall 35%. Leading me to argue that Farfetch’s Investors’ Day did not end up being a day for investors in Farfetch. It was a horrible day for investors that buy into the long-term bull case in Farfetch.

So, with this in mind, let’s discuss the bull case.

Fact: Luxury Market is Hot

Farfetch seeks to be the ”go-to luxury fashion marketplace”. Whether it succeeds in this endeavor or not remains up for debate.

However, even if Farfetch takes some market share in the luxury market, that alone could be enough to propel this company further.

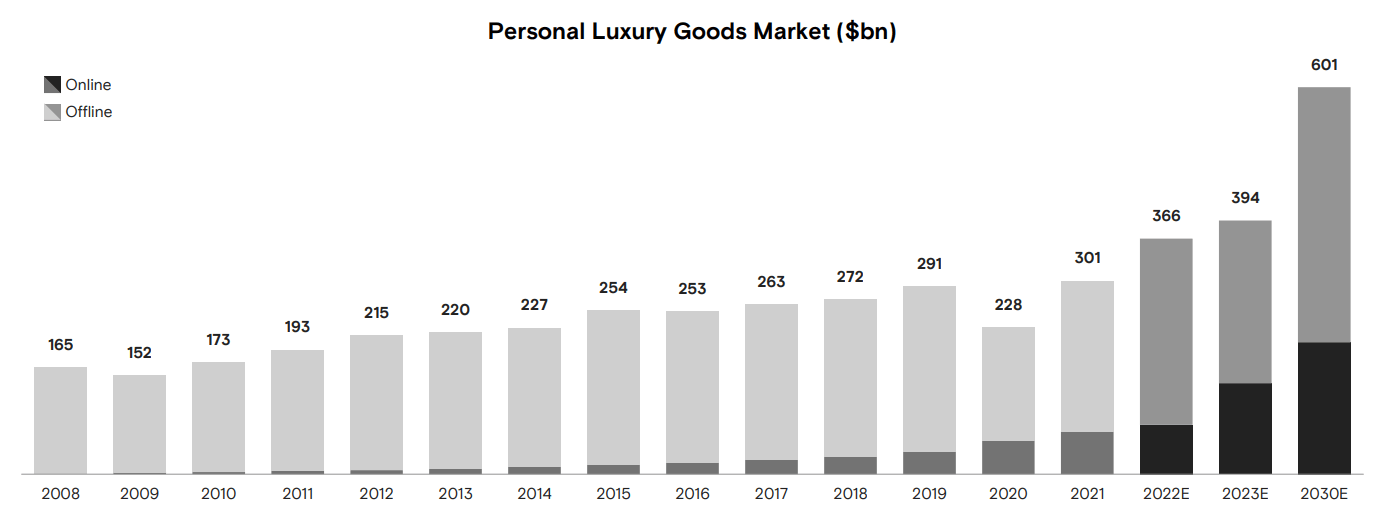

Now consider the graphic below which reminds us of the opportunity for luxury goods. What you see below is that the online luxury market is growing meaningfully faster than the offline market.

FTCH Investor Day

Even as both the online and offline luxury goods market grows, the online market appears to be growing much faster.

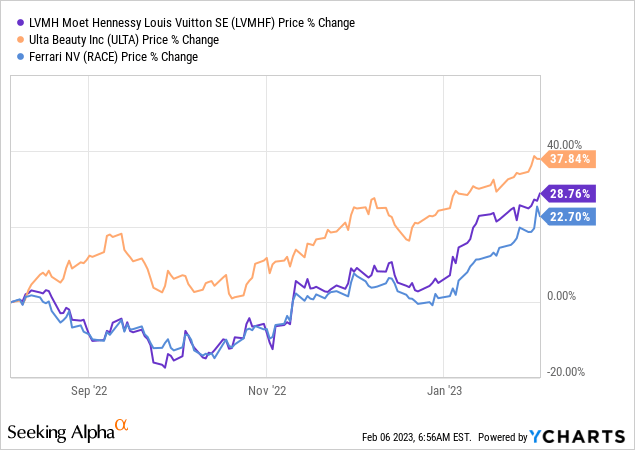

What’s more, for 2023 the luxury goods market appears to be more resilient than other parts of the economy. Put another way, I declare that irrespective of what investors may think about the macro economy, it appears to be the case that the luxury market is stronger than many investors may have been led to believe.

Above I’ve highlighted LVMH (OTCPK:LVMHF), Ferrari (RACE), and Ulta Beauty (ULTA), as examples.

My point is that while investors attempt to formulate a ”version” of where the economy is headed and what makes sense to them, the luxury market appears to already be leading the way.

With that context in mind, it’s worthwhile acknowledging that even though Farfetch has priced slightly off the lows of December, for all intents and purposes it is still at a multi-year low. Thus, it’s fruitful for us to dig further and get a little closer to Farfetch’s fundamentals.

Guidance Leaves a Lot to be Desired

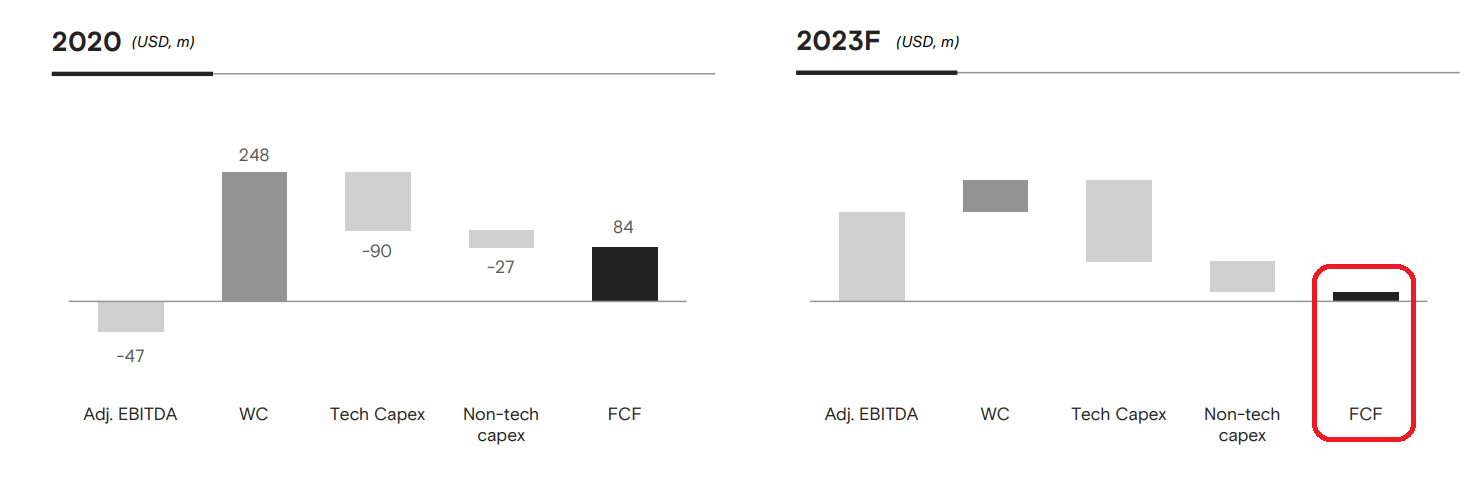

Now, we get to the core of the problem facing Farfetch’s 2023 guidance.

FTCH Investor Day

Think about it from this perspective, what the graphic above appears to infer is that Farfetch’s strongest free cash flow yielding days are in the rearview. Or more specifically, back in 2020.

How can investors buy into a company where management is literally telling you that this year holds little promise?

Again, let’s circle back to reality. At the time, the stock was already down 80% from its peak. Investors were already bruised. But at the same time, the message coming out from Farfetch in 2022 had been very consistent. In 2023, Farfetch would ”return to profitable growth”. So, now Farfetch appears particularly uninteresting.

But here again, this is now ”known news”. Investors will have by now come to terms with the fact that Farfetch is guiding for 2023’s adjusted EBITDA margin to be around 2% or somewhere less than $100 million adjusted EBITDA. In sum, I suspect that this negativity is already priced into the stock.

The Bottom Line

Farfetch has a lot of appeal. And when financial conditions were much easier, such as in 2020, Farfetch’s lackluster profitability was not an issue.

But right now, looking ahead to 2023 and asking investors to hold out for less than $100 million of adjusted profitability could be an ask too much.

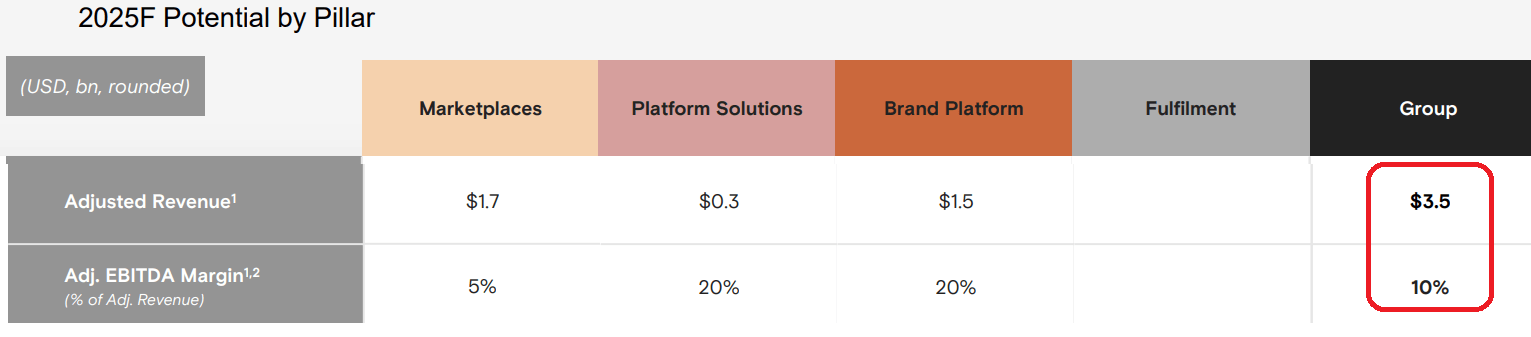

FTCH Investor Day

On the other hand, for investors that have a longer time horizon and are able to hold out two years until Farfetch is able to gain some traction on its profitability prospects, Farfetch could be reporting around $350 million of adjusted EBITDA. I won’t go as far as to declare this is cheap. But at the same time, most reasonable minds will struggle to argue that the stock is priced for perfection.

In sum, investors that are bullish on this stock should take care and appropriately size this in their portfolios. As I believe that a lot of bad news is already priced into the stock.

Be the first to comment