Edson Souza/iStock via Getty Images

Financial markets in the US and Europe face growing turmoil as the western banking system undergoes its most significant challenge since 2008. As discussed in “BIL: Stop Giving Banks Your Interest,” US investors have few safe options if difficulties continue to grow. The overarching issue is the stability of the US dollar vs. the strength of the economy and financial system. If the US Federal Reserve creates a new stimulus to “save” the overleveraged financial system, then it may risk making a collapse in the US dollar (due to inflation and interest rate cuts). However, failure to do so may result in significant losses for stock and bond investors as beliefs in the “Fed put” fade and depositor insurance is questioned.

The US government is studying ways to ensure all $18T in deposits, implying they may be willing to jeopardize the dollar’s stability to maintain the bank’s stability. Of course, this situation is highly non-linear, so there is little sense in making firm predictions. That said, I believe investors would be wise to consider ways to reduce exposure to US and European financial turbulence. One possible way is through foreign stock ETFs not hedged against currency fluctuations, thus gaining value if the US dollar declines on a new QE program or interest rate cuts. One interesting example may be the iShares Brazil ETF (NYSEARCA:EWZ).

US investors may underappreciate Brazil due to its economic turbulence over the past decade. Brazil is the largest economy in Latin America and the 12th largest globally. Unlike the US and most European countries, Brazil is consistently a net exporter of goods, selling primarily critical commodities like oil, food, and minerals – all of which have been subject to shortages in the US and Europe over recent years. Crucially, Brazil is also on good political and economic terms with virtually all countries. As the US and Europe distance themselves from China and Russia, Brazil gains an increasingly advantageous geopolitical and trade position.

Foreign stocks have particular risks that US investors must be aware of. EWZ has also performed relatively poorly over the past decade due to ongoing turbulence in Brazil’s internal economic and political realm. While these issues may continue, the US and Europe now face similar, if not larger, strains, making Brazilian stocks much cheaper than most in the US. I believe EWZ is a strong hedge against risk factors in the US and Europe. However, its absolute performance may remain negative until its economic and monetary outlook stabilizes.

Brazil Stock Valuations Absurdly Low To US

The US S&P 500 trades at a weighted-average “P/E” ratio of ~17.5X, well below its level last year but slightly above its long-term median. This equates to an earnings yield of 5.7%, which to me, is not very high considering the US discount rate is likely to reach 5% this year. Thus, given US bond valuations, US large-cap stocks appear a bit overvalued, particularly considering the recent negative trend in the S&P 500’s EPS.

Either US stocks are highly overvalued, or Brazil is significantly undervalued. To compare, EWZ currently trades at a weighted average “P/E” of 4.5X, giving the fund a dividend yield of 12.75% and an earnings yield of 22.2%. This is a very low relative valuation, far outside the normal range of US and European equities. Brazil’s “CAPE” ratio (or PE using 10-year average EPS) is the lowest globally after Turkey, Poland, and Russia. Of course, low valuations usually equate to higher risks, and Brazil’s troubles are not insignificant; however, I do not believe they are so much larger than those in the US and Europe to justify the enormous valuation discount placed on Brazilian equities.

Of course, EWZ is less diversified than the S&P 500. Around 25% of the fund is in the materials sector, and 15% is in energy. Other significant sector exposures include financials (23%), industrials (9.6%), utilities (8%), and consumer staples (8%); however, those weightings are not too dissimilar to that of the S&P 500. Whereas the US and Europe equity markets have more weighting toward consumer discretionary and healthcare, EWZ has far more toward commodity production. While some investors may see materials and energy as inherently riskier due to those sectors’ high turbulence in the 2010s, I believe they’re far superior in the 2020s. Materials and energy directly benefit from global inflation and shortages. Comparatively, consumer discretionary and healthcare are harmed by inflation since they’re generally “goods consumers.” More broadly, this difference illustrates EWZ’s value as a hedge against US dollar risks.

Will The Brazilian Real Stabilize?

The most significant attraction to foreign stocks is their capacity to hedge against US dollar risk associated with potential impending Federal Reserve stimulus efforts. International stocks also offer some economic risk reduction since they’re not directly exposed to the US economy. However, US recessions usually sink all stocks globally due to US trade dependence, although Brazil’s closer economic ties to Russia and China may reduce its overall exposure.

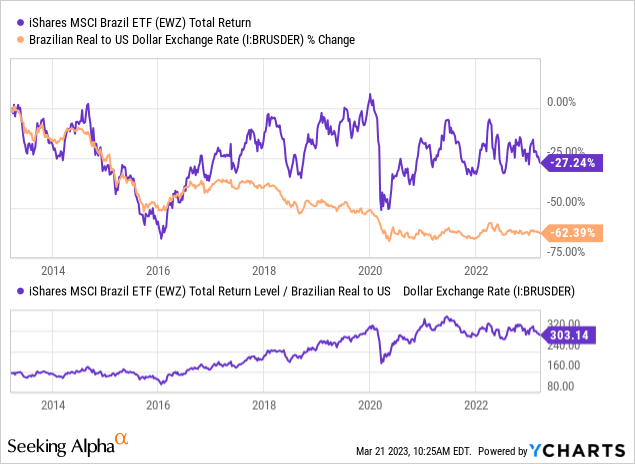

EWZ’s most significant challenge over the past decade has been the declining value of the Brazilian Real to the US dollar. If we adjust EWZ’s performance for Real, it’s been a decent investment in recent years. The Real suffered significant losses from 2013 to 2016 as collapsing global commodity prices hampered Brazil’s export value. This occurred again in 2020, with the Real failing to recover despite the rebound in commodities. See below:

Brazil’s current inflation rate is 5.6% annually, nearly the same as in the US and most European countries; however, Brazil’s interest rate is much higher at 13.75%. Under the real interest rate model for currency valuation, the Brazilian real should be much stronger today than the US dollar as it pays far more after inflation. Brazil also has a positive trade balance and a significantly lower public debt to GDP. That said, due to its higher interest rates and economic weakness over the past decade, Brazil’s government has been stuck in a huge fiscal deficit of 4.5% of GDP over the past year. The US deficit was more significant at 5.8% of GDP last year, signaling Brazil’s deficit is improving while the US’s is worsening. Brazil’s banking risks, relevant for the ~23% of the ETF in financials, are also much lower due to the country’s high 21% cash reserve requirement. In 2020, the US Federal Reserve set the cash reserve requirement to zero, directly helping fuel today’s liquidity crisis.

Overall, by all typical measures of currency stability and value, Brazil’s Real appears much stronger than the US dollar and Euro. During the 2010s, Brazil’s economic and monetary stability was poorer than today’s, while the US was much stronger. However, based on 2020-2023 data, Brazil’s monetary stability appears much more substantial as the country benefits from rising export prices due to commodity shortages. Comparatively, the US and Europe have been hampered by this change due to their dependence on foreign commodity imports. Further, Brazil has stronger financial protections, as seen in its much higher deposit rate and bank reserve requirements.

Brazil’s economy is not “strong,” but it is not worse than most today. Like the US and Europe, most of the country’s leading economic indicators signal a contraction. Its unemployment rate is historically low but did rise slightly last month. Further, Brazil’s labor productivity and economic output have declined since 2012; however, that is mainly due to the negative impact of commodity prices on its economy due to its commodity export orientation.

Brazil’s current leader, Lula, has a less capitalistic orientation than its last leader and seeks to reduce the country’s interest rate. At 13.75% with 5% inflation, I do not expect an interest rate cut to have a significant negative impact on the Brazilian Real since its real rate is already so much higher than the US dollar. Brazil’s tumultuous election, political drama, and its leader’s socialist bias have certainly dissuaded investors from the country. While Brazil’s political situation is a risk factor, I do not believe it is any larger than we see in the United States and Europe today.

The Bottom Line

Overall, EWZ trades at a considerable discount today compared to the S&P 500. Similarly, the Brazilian Real appears to trade at an immense discount, given the superiority of Brazil’s monetary policy and the improvement in its fiscal policy compared to the US (which has deteriorated dramatically). EWZ specifically offers investors positive exposure to the Brazilian Real, provides a very high double-digit yield, trades at an extreme valuation discount, and has sector exposures that give it a positive correlation to inflation in the US.

EWZ’s primary driver is the Real-USD exchange rate. Based on relative valuation metrics, the Real appears tremendously undervalued today. Fundamentally, I do not believe emerging market currencies are discounted for any solid economic reason, but due to the immense “exorbitant privilege” in the US dollar, which maintains a high global price despite a huge trade deficit and generally unsupportive monetary and fiscal policies. Investing in EWZ may seem particularly risky today, with the Brazilian Real as weak as it is. Still, at this point, I believe the gamble is becoming very favorable to emerging market currencies as the Federal Reserve makes a dovish shift in response to the banking crisis.

Emerging market countries are beginning to make efforts to break the US dollar’s privileged status. Brazil and Argentina are looking to create a Latin American currency union. China, Russia, India, Saudi Arabia, and South Africa have also stated similar intentions and are working to decrease the dollar’s trade dominance. In general, these countries have much stronger commodity exports and industrial power than the US and Europe today, giving them more potential currency power if a type of currency union or similar agreement is formed. This factor is another reason US investors may want to hedge against the US dollar actively.

Overall, I am slightly bullish on EWZ today. Compared to the S&P 500 and most other western equity indices, I believe EWZ is vastly superior due to its low valuation, commodity orientation, and potential currency appreciation. I believe EWZ’s most significant possible bullish factor is appreciation due to the likely depreciation of US and European fiat currencies triggered by the banking crisis. That said, ongoing signs of a global economic recession may impair EWZ’s value as the EPS of many of its constituents declined. While EWZ may be less exposed to this risk than the S&P 500, it may still lose considerable value if equity declines are not matched with currency appreciation. To me, EWZ is a superior hedge against mounting US risks, but it is still a very volatile and slightly speculative bet that investors should be mindful of.

Be the first to comment