belterz/E+ via Getty Images

Main Thesis & Background

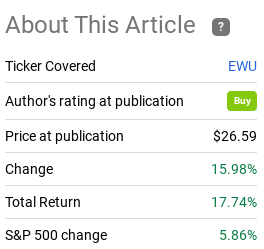

The purpose of this article is to evaluate the iShares MSCI United Kingdom ETF (NYSEARCA:EWU) as an investment option at its current market price. The fund’s stated objective is “to track the investment results of an index composed of U.K. equities.” The fund offers exposure to large and mid-sized companies that are based in the United Kingdom.

I noted this fund as a solid contrarian investment in early October because the prevailing market sentiment was heavily against Britain and British stocks. While there were some valid reasons for this, I believed the pessimism was overblown. In hindsight, I was completely correct, with EWU seeing a very large gain that easily surpasses the S&P 500 during the same time period:

Fund Performance (Seeking Alpha)

The reality is that while this was a very welcome return (as an investor in EWU), once such a big gain occurs, I always start to get a little cautious. Out-performance can often continue for long stretches of time, but it makes sense to revisit a buy thesis after such a move to see if it still holds true. After seeing an almost 18% pop for EWU and re-evaluating the investment opportunity I now see some reasons for caution. Therefore, I believe a downshift to “hold” is the correct outlook for EWU and I will explain why below.

Corporate Anxiety Could Weigh On Investment

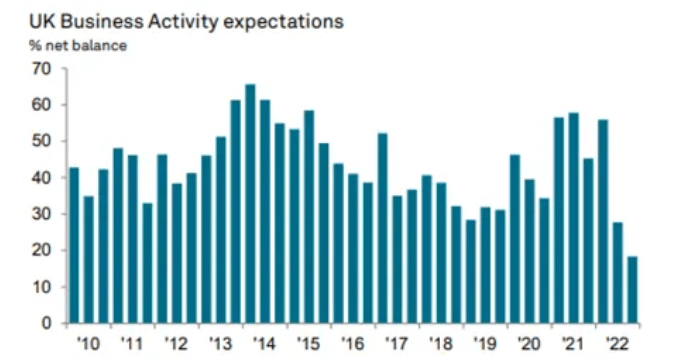

Among my concerns are business confidence. This can be a leading indicator that is a self-fulfilling prophecy (to some degree). The idea being that if business leaders/executives are worried about the economic outlook they will hold back on spending and investment. This then leads to a weaker economic backdrop if the trend becomes widespread, rendering the pessimistic outlook correct by their own actions!

The reason I am more worried now than usual is that UK business confidence has been falling consistent and recently hit its lowest level in over a decade:

Corporate Outlook (UK) (S&P Global)

This tells me that employers are getting increasingly concerned about their potential for revenue and profit. This could lead to a lack of investment across Britain and put a pinch on an already weakening economic environment. While investors in EWU have the benefit of holding mid and large-cap companies that tend to generate quite a large percentage of their revenues (and profits) from outside the UK, we should still be concerned with what is going on within the island itself. This level of pessimism tells me at the very least to be more cautious with my investment dollars, suggesting a downshift in my rating is the right move for EWU.

Britain Looks To Under-Perform Developed Markets In 2023

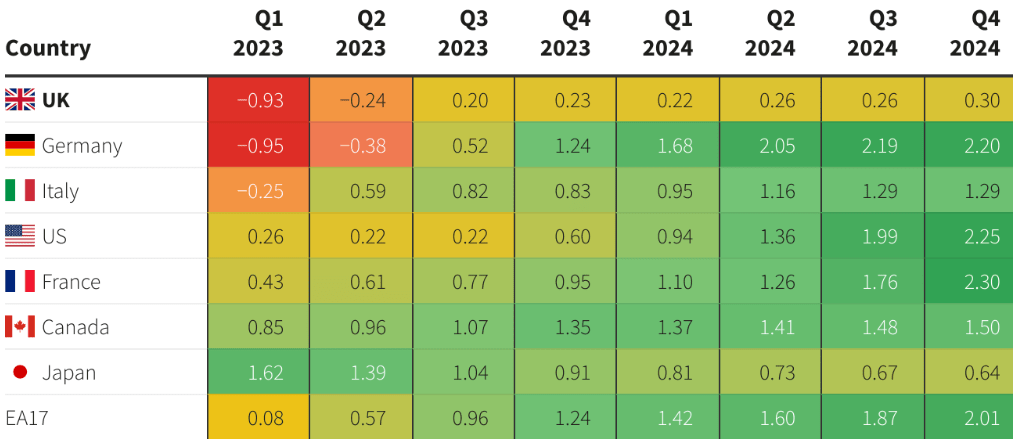

Expanding on the above point, the worries about growth are more widespread than just British business leaders. According to the OECD, the UK is expected to see a sharp decline in growth in Q1 2023, followed by negative growth in Q2 as well. This is never a positive sign, but it is especially troubling since the current forecast illustrates most of the G7 will see stronger growth in the year ahead:

Relative GDP Forecasts (G7) (Organisation for Economic Co-operation and Development (OECD))

Aside from being a net negative in isolation, I am concerned this forecast could limit the investment potential in funds like EWU. Investors will recognize this risk and begin to limit their holdings in British stocks, and also potentially the British pound debt as well. The result will be higher borrowing costs and a bleaker investment backdrop that could push down the valuation premium investors are willing to pay for British equities.

To be fair, this has been a headwind for a while and investors seem to have been shrugging off these concerns with a new Prime Minister restoring some confidence. But this again stems back to such strong gains the stock market there has already seen. If EWU was sitting with recent weakness/declines in the past few months, I would probably be a buyer here. But with an 18% move higher for EWU and likely negative growth for the next 3-6 months across Britain, the prudent move here is to get cautious.

Higher Borrowing Costs A Disproportionate Risk

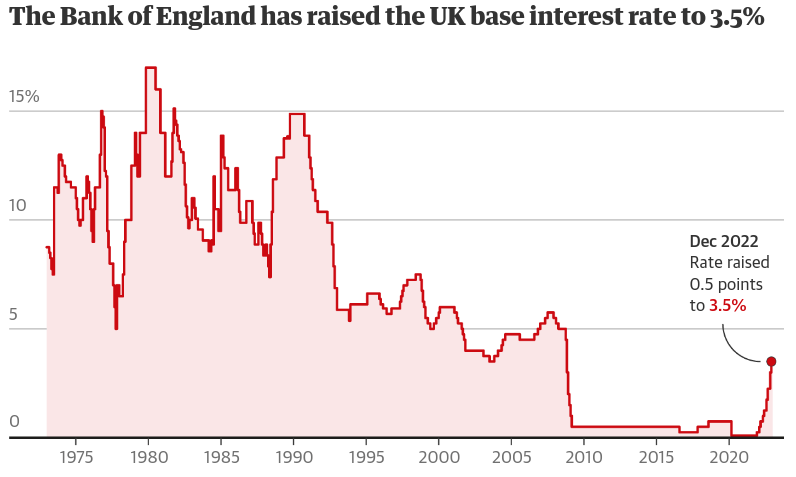

Another risk to contend with that is relatively unique to the UK is rising costs of mortgages. This stems from the fact that interest rates have been on the rise consistently in the UK and elsewhere in the developed world. The latest rise from the Bank of England was just last week when the benchmark rate was hiked to 3.5%:

BoE’s Rate Moves (BoE)

I am not suggesting the BoE is alone in this maneuver. Here in America the Fed has continued to increase interest rates and so have the central banks in Canada and continental Europe. So that is not the differential. What is the differential is that British households are potentially more exposed to this development.

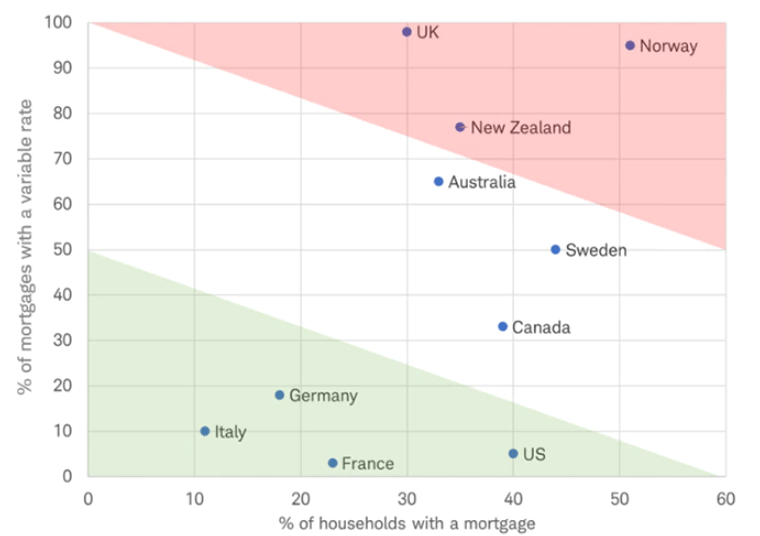

The reason being is that a high percentage of mortgages in the UK hold variable rates after an initial period expires. Yes, other countries like Norway and New Zealand are in the same boat, but the majority of the G7 has a residential population with long-term fixed rate financing for their homes:

Mortgage Picture (Charles Schwab)

The conclusion I draw here is the British consumer – at least the ones who own a home with a mortgage – could face steep increases in their monthly mortgage payments going forward. As interest rates reset higher throughout 2023 (and potentially longer), mortgage obligations are going to increase. This risks a decline in consumer spending, particularly in discretionary areas. The reason I see it as a headwind for Britain, and EWU by extension, is other comparable investment opportunities across major countries do not face this risk to the same degree. This lowers the attractiveness in British stocks, especially domestic-oriented stocks, in relative terms.

There Has To Be Some Good News – Right?

My tone so far has been pretty negative. This may be making readers wonder why I am not “bearish” on EWU, rather than neutral. Simply put, I do see some bright spots for Britain and British stocks that suggest if the worst case scenario does not occur there is plenty of room for more gains. I have to weigh the bad against the good, and there definitely is some good out there.

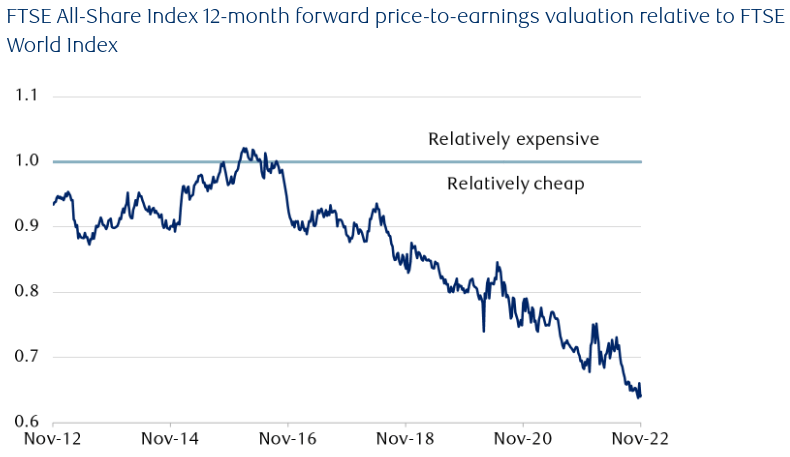

One bright spot has to do with relative value. Despite EWU’s surge in the last two and a half months, it tracks an index that is still cheaply priced in relative terms. Broader speaking, the FTSE index has seen its valuation gap between the rest of the world markedly increase over time. As global equities rebounded in November, this dynamic accelerated:

FTSE’s Relative Valuation (RBC Wealth Management)

This suggests that even for investors who did not buy into EWU yet, there is potential ahead. Actual GDP growth could surprise to the upside, the BoE could hit the brakes a bit, and business confidence could be restored – or some combination of all three. When I combine these “ifs” with the valuation gap present across the pond, that makes it difficult for me to be a bear here.

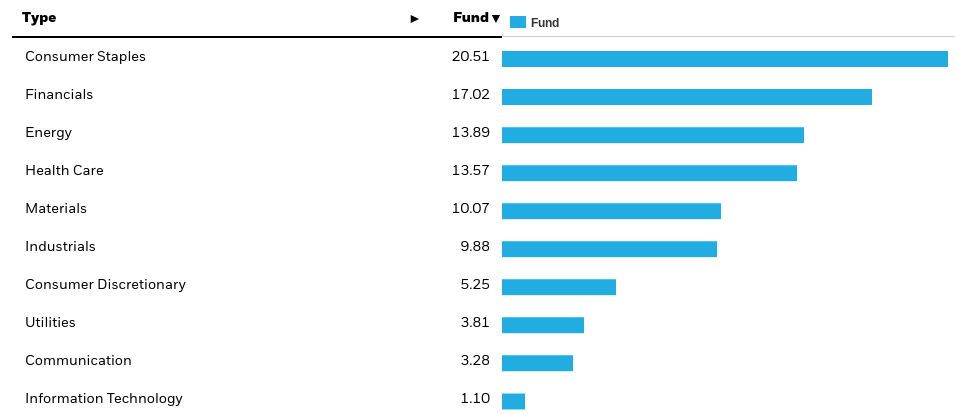

Further, I continue to like EWU as a relative hedge against my U.S.-centric portfolio. While the S&P 500 is overweight in Technology, Health Care, and Consumer Discretionary, EWU’s top three sectors are Consumer Staples, Financials, and Energy:

EWU’s Sector Weightings (iShares)

The point I am getting at here is this ETF helps to round out my sector exposure nicely. I am getting British companies, which are obviously different than what is in the S&P 500, but I am also getting a higher concentration of sectors that are less dominant in the S&P 500. This is a win-win, especially as we enter a challenging 2023. EWU’s more defensive nature (compared to the S&P 500) tells me that holding on to this product has plenty of merit. I just don’t see a compelling “buy” thesis right now, but that could change if we see a forthcoming correction.

Bottom-line

The UK has been a source of headlines and drama for quite a following. This is especially true in a post-Brexit world, the implications of which persist today. Looking ahead to next year, there are multiple challenges British equities will face, and that makes me cautious considering the run EWU has had recently.

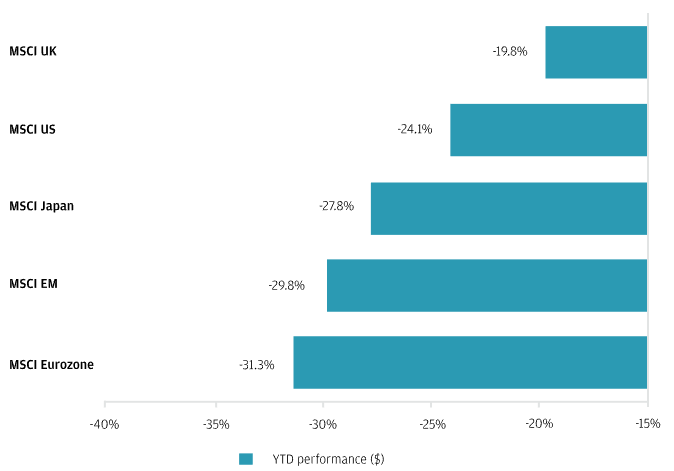

But I would not suggest investors get overwhelmingly bearish on EWU either. British stocks have done poorly in total in 2022, but that is true across the world. In fact, Britain’s recent surge, combined with its lack of proximity to the Russia-Ukraine war (compared to most of Europe) has actually allowed equities there to out-perform their global peers year-to-date:

Global Performance (JPMorgan)

In addition, some of the challenges facing Britain could result in a weaker currency. While this may not be a “good” thing overall, it could give a boost to funds like EWU whose large-cap holdings make a significant percentage of their earnings overseas. Generally speaking, there has been a strong inverse correlation between the relative performance of UK equities and the British pound. This has been true in 2022 and could be true next year as well.

In short, this is a push-pull environment and will probably remain that way for the next few quarters. So I won’t be clamoring to buy just yet, but I will keep EWU on my watchlist and consider adding when and if the price declines. This leads me to believe a “hold” is the right rating for the fund, and I suggest readers approach any new positions selectively at this time.

Be the first to comment