frantic00/iStock via Getty Images

A lot has been happening in Europe this summer. Recent elections in both the UK and France have garnered the attention of global media. I’ve been steadfastly watching the Euros, the quadrennial European soccer tournament that is intended to tide us over in between World Cups. This year’s Euro Cup is taking place in Germany, and I’ve realized it has been far too long since I’ve covered Europe’s largest economy.

Way back in March I covered the Global X DAX ETF (DAX), and today I’ll be looking at its much larger (in asset size) counterpart the iShares MSCI Germany ETF (NYSEARCA:EWG), highlighting key differences and contextualizing its performance against the current German and European economic backdrops.

EWG is well positioned for some upside based on its exposure to the industrials sector that will benefit from the monetary environment in the EU. However, the relative strength of the dollar is diminishing some of the return potential for the fund. Even still, I rate EWG as a buy given that the recent inflation data for the US is positive, and will likely lead to an interest rate reduction soon.

ECB rate cuts could benefit German exporters

Germany is known for its strong manufacturing base and export-oriented focus relative to other European economies. For this reason, EWG’s performance is more sensitive to ECB machinations that move the needle on the Euro’s relative strength. The dollar has been stronger relative to the Euro for the first half of 2024 and this trend will likely continue for as long as the Fed keeps interest rates elevated relative to the ECB. A weaker Euro makes German exports more competitive for the time being.

EWG fund overview

EWG debuted in 1996 and has roughly $1B at the time of writing. Germany has several options in the way of representative single country ETFs, which is not surprising given the significance of the German economy. It is currently ranked as the third-largest economy in the world, after the US and China, in terms of nominal GDP. EWG is by far the behemoth in terms of assets under management, more than 10x the size of the second-largest German ETF, DAX. While we are here, it is worth mentioning that EWG is the more expensive than DAX, with an expense ratio of 0.50% vs. DAX’s 0.20%

EWG tracks 56 large and mid-sized German companies. From a sector perspective, it has a strong tilt towards industrials (~20%), followed by financials (~20%), and IT (~18%).

iShares

When comparing EWG’s sector holdings relative to DAX, we see that the only sector with significant drift is in the industrials sector.

ETF Research Center

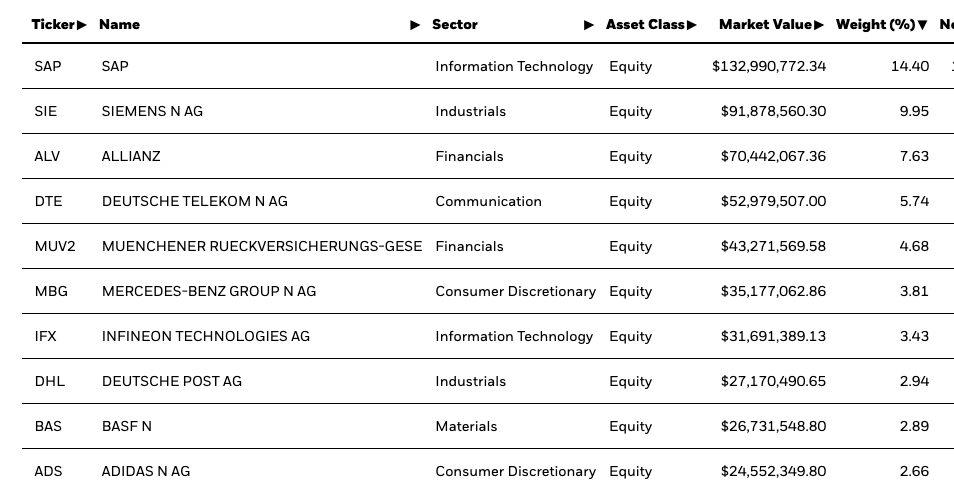

At the individual holdings level, EWG is fairly concentrated. About a quarter of all assets are allocated to IT giant SAP (SAP) (~14%) and the industrials company Siemens (OTCPK:SIEGY) (~10%). About 58% of all the fund’s total assets are concentrated in the top 10 holdings, which is in line with expectations for a single country ETF. Both SAP and SIEGY have printed large returns on a trailing 1-year basis (around +50% and+ 22% respectively).

iShares

EWG has a couple of attractive data points at the moment. For starters, it is trading at 1.5x book value and around 13x earnings. Given the fund’s large exposure to the “growthy” IT sector, these valuations are enticing. EWG also has a trailing twelve-month dividend yield of 2.44%, while not exceptional, is not much below the median for all ETFs.

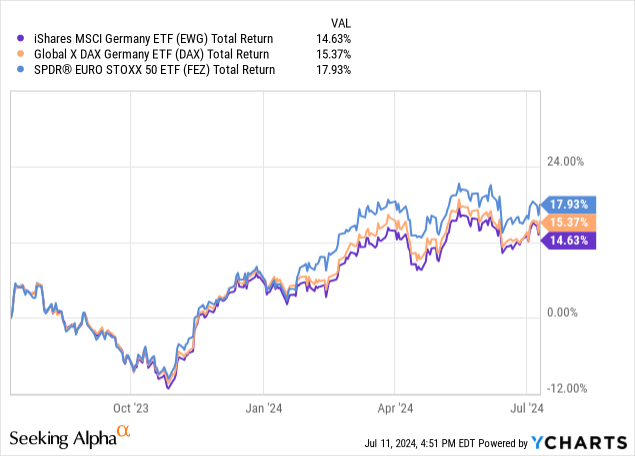

Performance comparison

From a total return perspective, EWG has delivered ~15% over the past year. This has slightly underperformed DAX, as well as a broader European universe of blue chip equities in FEZ.

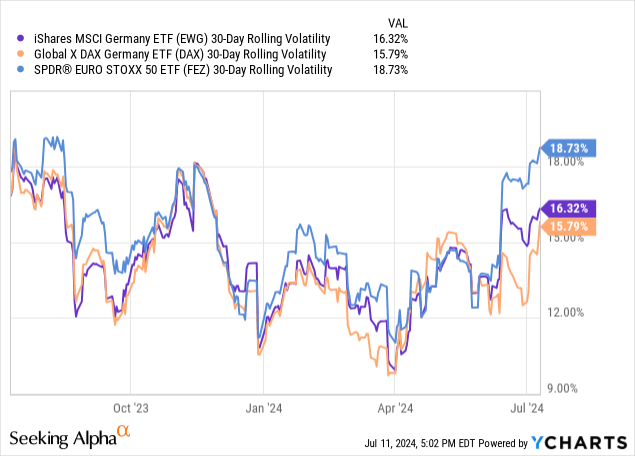

From a volatility perspective, we see EWG’s volatility profile is comparable to that of DAX, and lower relative to the broader European universe.

Flows

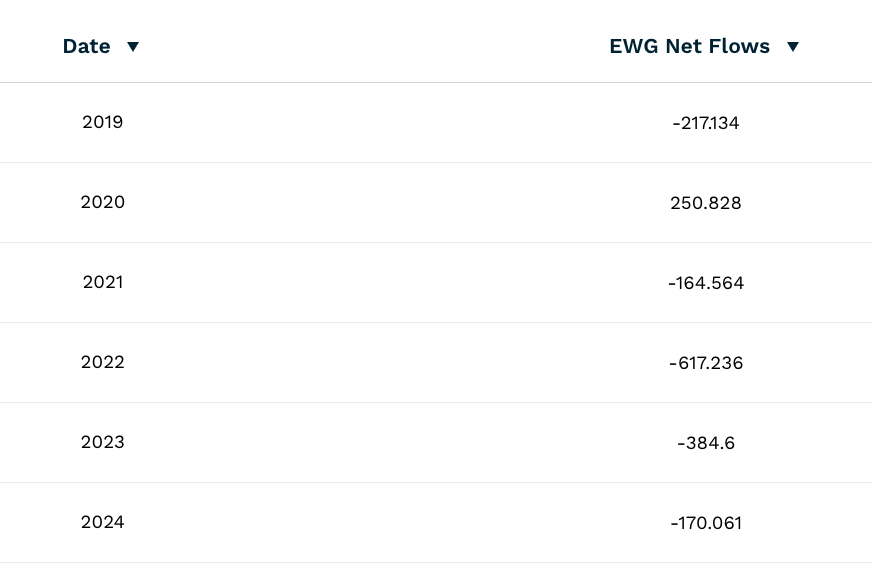

From a flow’s perspective, EWG has been challenged, despite delivering +15% over the 5-year period. EWG has seen consistent outflows since 2021, with particularly sizable outflows in 2022. This is likely due to economic weakening in the Euro area that took place after the onset of COVID. This contrasts with DAX, which has seen inflows over the same period, albeit significantly smaller inflows. Remember, EWG has close to $1B in assets compared with DAX’s $71M.

ETF.COM ETF.COM

Continued rate cuts pose risk to financials

While rate cuts have the potential to provide continued tailwinds for the German industrials sector, a continuation of rate cuts could pose as a challenge for the German financials sector, which makes up about 20% of the EWG. Diminished interest income could outpace an expansion in lending, which is a realistic risk for EWG.

Conclusion

EWG has delivered middling returns YTD, but the continued economic expansion in the Eurozone and the potential for still lower interest rates in the region could benefit EWG. There is a balance to be struck, where lower interest rates in the Eurozone do not diminish the Euro so much that dollar-denominated EWG returns are subdued. I believe with a likely forthcoming rate reduction from the Fed, EWG could strike a more favorable balance. I currently rate EWG as a buy.

BlackRock

Be the first to comment