Alex Wong

Bitcoin (BTC-USD) has long been championed as an alternative asset class. Now, in a time when many investors are seeking just that, amidst hit after hit to equities as the Federal Reserve keeps raising rates, Bitcoin is more correlated to the stock market than ever. As Bitcoin becomes more mainstream, I don’t expect this trend to reverse. All of this is problematic for Bitcoin as an asset.

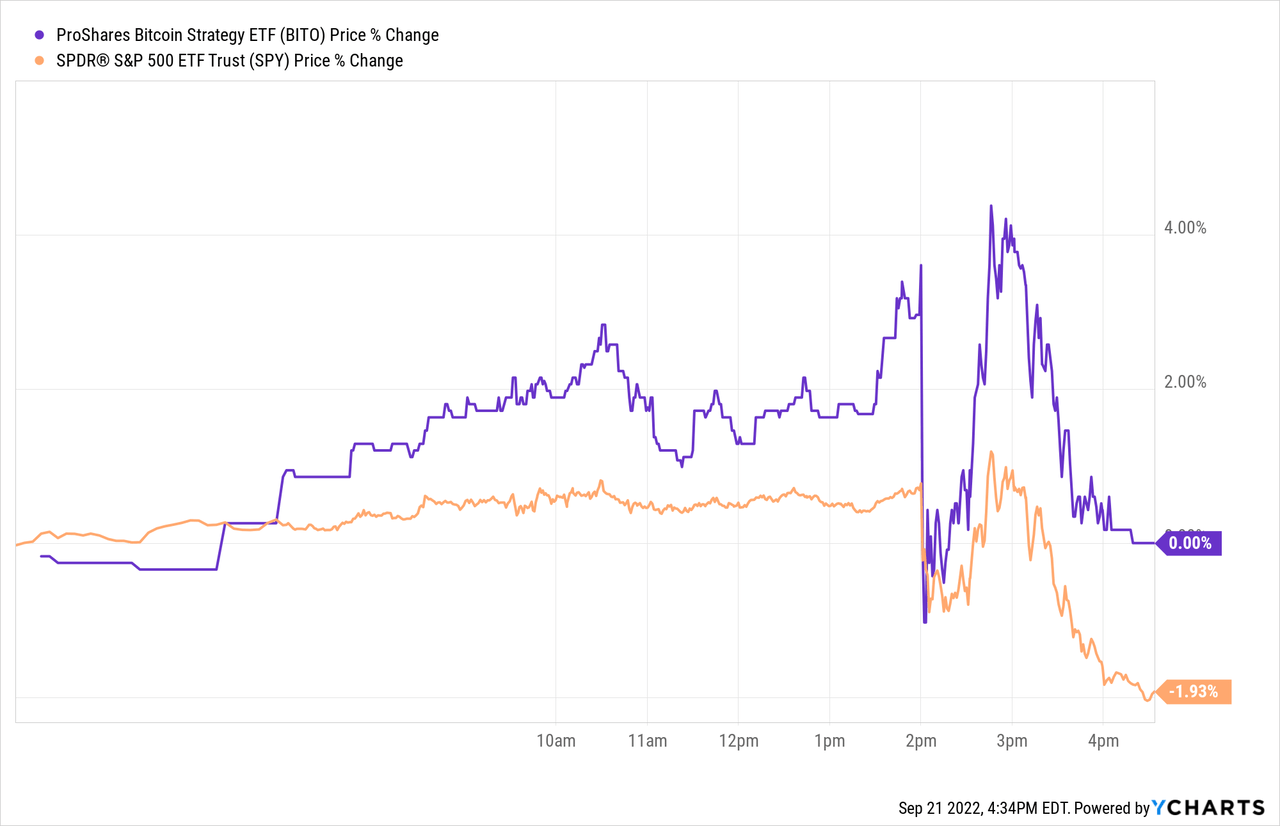

September 0.75bp Rate Hike Tanks Bitcoin

On Wednesday, the Federal Reserve met and decided on yet another 0.75 basis point hike. Additionally, they made it excessively clear that curbing inflation is the Fed’s number one priority:

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. In support of these goals, the Committee decided to raise the target range for the federal funds rate to 3 to 3-1/4 percent and anticipates that ongoing increases in the target range will be appropriate. In addition, the Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage-backed securities, as described in the Plans for Reducing the Size of the Federal Reserve’s Balance Sheet that were issued in May. The Committee is strongly committed to returning inflation to its 2 percent objective.

This subsequently sent the stock market tumbling. But it also sent Bitcoin down. If the goal of Bitcoin and other cryptocurrencies like Ethereum (ETH-USD) is to “decentralize finance” and provide an alternative asset class for investors, Wednesday’s performance was highly problematic.

The above graph shows ProShares Bitcoin Trust (BITO) and SPDR’s SPY ETF (SPY) moving nearly perfectly in sync after the Fed’s 2 pm announcement.

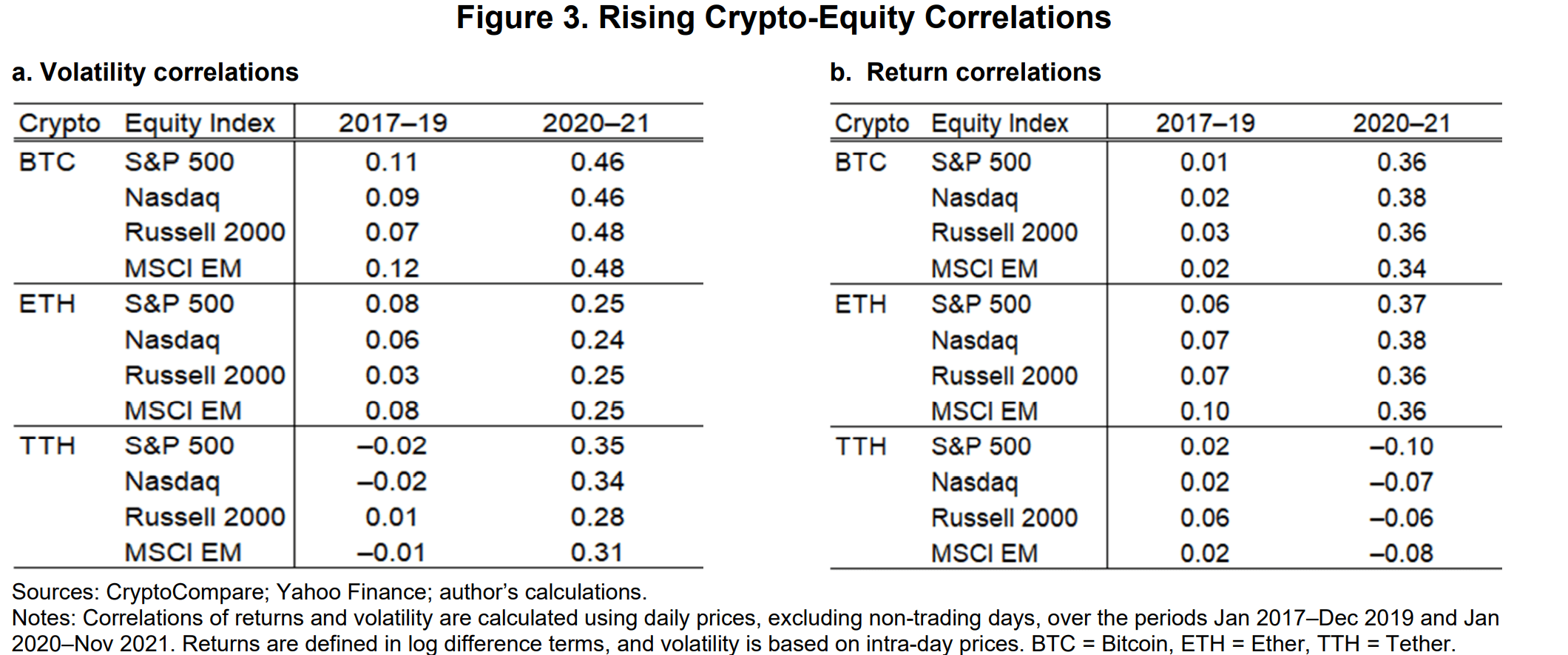

Recent Research Shows Bitcoin Increasingly Linked With Equities

This correlation is not purely anecdotal either, nor is it a one-time event. According to a study published by the International Monetary Fund in January,

The findings suggest that the interconnectedness between crypto and equity markets has increased notably over 2017-2021.6 For example, compared to pre-pandemic years, the correlation between Bitcoin price volatility and S&P 500 index volatility has increased more than four-fold, while Bitcoin’s contribution to the variation in the S&P 500 index volatility is estimated to have increased by about 16 percentage points in the post-pandemic period.

The volatility of Bitcoin is much higher, generally, than the stock market, and it is increasingly correlated with equities. This correlation increased four-fold between 2017 and 2021 according to the study:

“Cryptic Connections: Spillovers between Crypto and Equity Markets” (Tara Iyer, Published IMF)

The spillover effect from the S&P 500 (SP500) to Bitcoin has increased even more strongly than in the opposite direction, suggesting equity markets increasingly decide the movement of crypto:

For example, volatility spillovers from Bitcoin and Tether to S&P 500 have increased by about 16 and 6 percentage points, respectively, between 2017-19 and 2020-21, whereas volatility spillovers from the S&P 500 to Bitcoin and Tether have increased by 13-15 percentage points (Figure 5). Similarly, return spillovers from Bitcoin and Tether to the S&P 500 have increased by 10 and 6 percentage points, while those in the reverse direction have increased by 12-13 percentage points (Figure 6).

This increased correlation has been called “temporary” in a report by 21Shares, suggesting this is only a short-term phenomenon and that long-term crypto remains useful for asset diversification. However, given the significant increase over the last few years, the idea that crypto and equities will decouple again is questionable.

This is primarily because Bitcoin, alongside Ethereum and other large coins, is no longer a niche asset. Institutional investors have piled into the crypto space and for lack of any fundamentals to make buy and sell decisions (as one might consider with equities), crypto is quick to be traded on sentiment swings.

And sentiment ain’t never swing like when Jerome Powell hikes interest rates.

Takeaway

One of the problems with discussions of Bitcoin trading separately from the stock market is that such decoupling often assumes a calm market environment. For example, in this June article:

Despite hitting a 17-month high in correlation with the S&P 500 this year, Bitcoin has a proven track record of actually remaining uncorrelated from equities. When market conditions become safer, Bitcoin will return to its normal self and trade uncorrelated.

But the time when you most want an asset class uncorrelated to the stock market is in an inflationary market facing significant bearish pressures. Unfortunately for crypto investors, the opposite is the case.

Ironically, it seems that Bitcoin’s adoption may also be its downfall. As Bitcoin is increasingly accepted by mainstream financial services, it loses its value and becomes just another asset in a basket. Decentralization isn’t much use if your asset is owned and processed by the largest banks in the world.

I’ve already discussed why I don’t believe Bitcoin is useful as an actual currency. However, it is increasingly clear that Bitcoin is not a very good asset class either. It is highly correlated with stocks, except more volatile in a hostile market environment. For me, that means now, perhaps more than ever, is a good time to stay away.

Be the first to comment