Juanmonino/E+ via Getty Images

The Secret

The Christmas lights displayed all around Paris were still lighted, but both the city and the sky were dark-tinted grey. And it was cold. It was that bone-penetrating, humid, Paris cold you get at the end of December and that lasts to early Spring.

There’s a young woman sitting under a heat lamp in front of a local brasserie. She is eating her favorite item on the menu – warm onion soup. She is wondering about some of her high school friends. She lost track of them years ago, and she is thinking that most of them by now have probably wrapped up graduate school or launched careers. Her and their lives started to diverge when they all went off to university and she didn’t. As more time went by, the less in common she felt she had with any of them. The most stark difference was when she started to feel that unlike any of her former classmates, she wasn’t moving towards anything. How could she? Unlike most people her age, she was already THERE in many senses. She sometimes feels that she’s been THERE ever since she was 14 years old, when her mom sat her down for the first time and told her about “The Secret.”

The Secret. She had gotten plenty of practice carrying The Secret around very discreetly when she was still in school, but the hints naturally had started to seep out through the cracks of her life. Like when her friends used to work through the night studying for their exams. She never bothered to. It wasn’t about being smarter than them – she knew she wasn’t. It was about not being answerable in the way most people are. Or then there was that time when she got her first car and totaled it. She was lucky not to have been seriously hurt – or to have hurt anyone else. The car itself didn’t matter. She bought a new one two weeks later. Same color.

Other than that, there weren’t many outward signs of The Secret while she was growing up. She was raised in a small apartment with her mom and dad, both of whom worked as English teachers. A long time ago, dad had gone into business with a friend selling used books out of a tiny shop back in Small Town, U.S.A. It was a modest and irregular supplement to his teacher’s salary, but mostly he just loved working on Saturdays and Sundays in a place where he could be surrounded by old books that smelled like mothballs. But in the late 1990s, he saw the writing on the wall. He knew that a major chain like Barnes and Noble would certainly put him and his business partner out of business one day. Then in 1997 came the end of the beginning, Amazon (AMZN). There was no way to compete against that, against the convenience of books that you could order online at the lowest price the market was willing to bear (or in many cases, even lower than that).

So her dad did the only thing he could think to do. He bought stock in Amazon. He didn’t buy much – maybe $15,000 or something like that (the young woman wasn’t sure). But back then, it had been a huge chunk of her mom and dad’s entire net worth. Dad was just convinced that Amazon would change the way used books are sold – so much so that he decided to not only buy himself and his wife some shares, but to also buy about $8,000 of shares for the young woman, too, which he placed into something called a “Uniform Gifts to Minors” account (that meant she couldn’t get the money until age 18). She was less than a year old at the time, which meant 17 years for the account to grow. Dad thought that one day, the account might even be big enough to pay for her college – or at least pay for a good part of her tuition.

Dad always said that he was no great investor. But he and mom were thrifty, like most teachers are. Dad invested most of his and mom’s 401(k) plans into index funds, but the rest of their savings just went into two stocks – Apple (AAPL) (the only reason why was because mom loved the products and used Apple computers in her classroom), and of course Amazon. As mom and dad’s accounts started growing beyond their wildest dreams, they began to make $8,000 gifts to the woman’s Uniform Gifts to Minor’s account and every year, and dad bought her more shares of the two companies that he knew best – Apple and Amazon.

“I was never a great investor,” is what dad liked to say. “My only claim to fame is that I didn’t listen to all those private bankers who kept telling me I needed to diversify. If they aren’t worth more than me, how can they say they know better than I do what I should do with my money?” He loved telling stories all the time but that one was probably his favorite.

And then one day there was just one single working mom (who still washes and reuses plastic zip lock bags), a modest home with beat-up furniture, the daughter and The Secret always looming in the background. Plenty of the kids she went to school with came from rich families and were more than happy to put that fact boldly on display. But by the time she’d turned 18, she’d quickly learned that there is a huge difference between coming from a rich family verses having your own money. That is what made her strange, and being strange is what made her feel strange.

It’s old news to her now, but the young woman is still amazed what $8,000 investments into Apple and Amazon stock can do after 25 years.

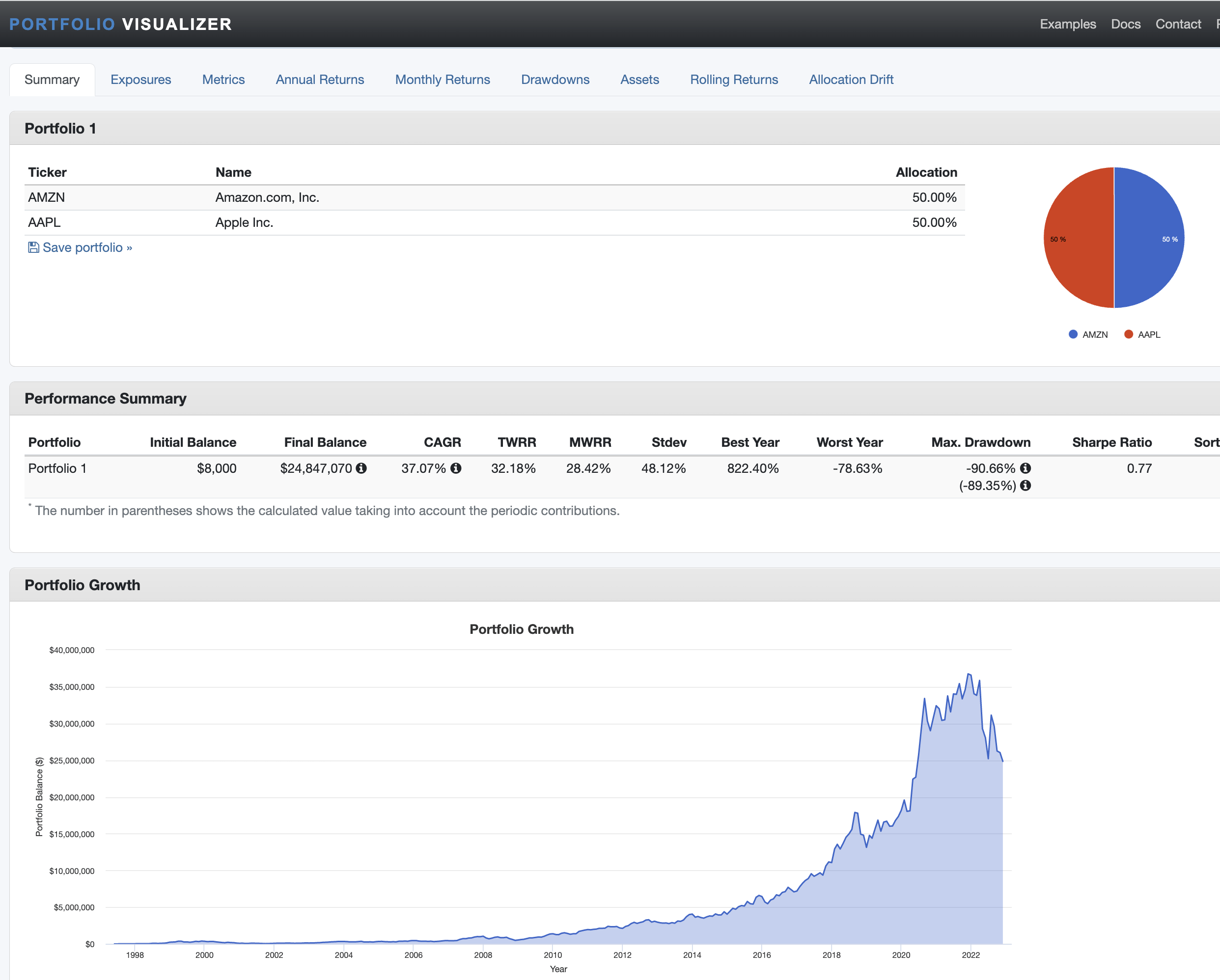

A Scary Chart (Portfoliovisualizer.com)

The chart is practically imprinted on her imagination, but not just because of the numbers at the top of the page. It’s because in so many ways, the chart has defined the arc of her life. She remembered last year, for example, a time when she’d still felt a sense of progress with her life. Back then, with $35m to her name, she figured that based on her portfolio’s past returns, she was probably likely four or maybe five years away from having what she had recently come to think of as “serious money.” $100m. The chart also reminds her of the time when she was 14 years old and her mom decided to tell her that her account had just hit $1m for the first time. Back then, she had no clue what $1m meant – only that it was a lot of money that put her in a different situation than any of the kids she knew. She didn’t start to feel “wealthy” until a couple years later, once her account cleared $5m. She definitely felt wealthy when she bought herself a new Porsche for her 16th birthday… with her own money. And then by the time she was 20 years old, she hit nine figures for the first time. It turns out that was the turning point in her life because from that moment to today, she has never again felt the sensation of being wealthy. That’s when building a $100m portfolio had become something like her life’s quest.

She used to tell herself that she had a career just like anyone else her age – the only difference was she worked for herself and got paid a whole lot more than most people. That thought gave her a sense purpose until late last year when she allowed herself to admit the truth: there was nothing for her to actually “do” in order for her account to finally clear the $100m mark. Her life’s goal, she realized with dismay, meant little more than just… waiting. It was like that’s all she had ever done.

Her old friends definitely wouldn’t have understood. The Secret. Mom always told her that she had to keep her finances completely secret or everyone she knew would start pestering her for loans that they’d never pay back, or to invest in their pet start-ups. “Once they know, money is going to dominate your relationships.” Those warnings had certainly made it easier for her to avoid having many close friends.

It gets dark early in Paris in the winter. The young woman finishes most of her remaining onion soup and then looks at the time. 3:00pm, and the sun’s already low in the cloudy afternoon sky. Her shift isn’t up for another two hours. Her legs will ache by end of the day – waitresses are on their feet nonstop. She doesn’t care that the pay is bad or that the work is hard – physically and occasionally (with certain customers) emotionally. This is her first job and she loves it. She talks to people all day. The chef and kitchen crew like to tease her and make her laugh. And whenever she’s at work, she always forgets about The Secret.

The waitress on a late lunch break (Author’s photo collection)

The Best Four Estate Planning Lessons I Can Give

The math is so simple when it comes to planning for your children’s financial futures: just start with a small cash gift (or series of small cash gifts), invest into some high-quality stocks and/ or low-cost index funds, and then allow the power of compounding to multiply those amounts exponentially as the years and then decades roll by. Dare I say that is the easy part?

As an estate planner, I always thought my value-added consisted of my exceptional ability to imagine the worst case scenarios (coupled with my completely average abilities to plan around them). One thing I never gave much thought to, though, was this: what happens in “the best case” scenario?

We’re all investors here (or at least many of us are). What is “the best case” scenario as far as we’re concerned? That’s easy! Become rich! None of us will have any problem handling that kind of success for ourselves – not if we’re the ones who made it happen in the first place.

But it’s a different thing when someone else succeeds FOR YOU. And it’s a much different thing when someone else achieves so much on your behalf that nothing you can do on your own will ever come close. Money always comes at a cost. Motivation. Relationships. Personal fulfillment. When you’re planning for your kids’ financial futures, the big questions are (1) what form do those costs take; and (2) which generation ends up paying them.

How can you manage the costs to your children of giving them money that they didn’t earn? Here are four ideas.

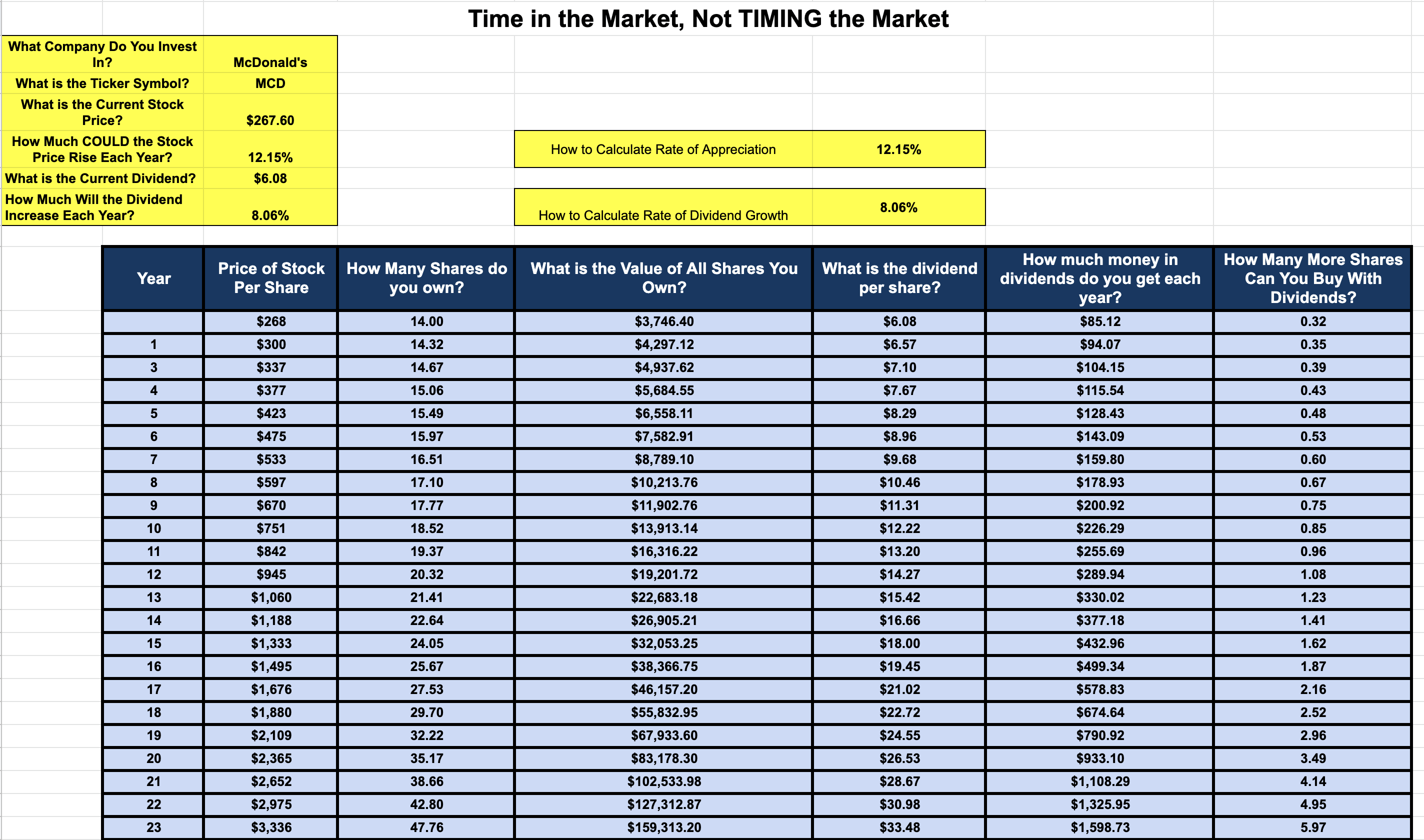

First, you can teach them about money, like Rida Morwa describes in his recent (and I think brilliant) article. You can set up an account for your kids and then sit down down with them every month and talk through how to reinvest their dividends. Maybe let them click the “buy” button and give them real world, real-time experience. If you want to teach kids about the power of compounding, feel free to download a copy of a free spreadsheet that I created to help tutor teenagers at my daughter’s school in personal finance. I sit down with the student, we input a ticker symbol, I manually input the dividend amount and dividend growth rate (which I show them how to pull off Seeking Alpha), and I show them how to arrive at a reasonable assumed rate of capital appreciation. Then the student can visualize how the account mushrooms in value over the next 20, 30 or 66 years. Follow the link and you’ll see other lesson plans that I use, too. And please feel free to make a copy and adapt the material as you see fit.

Compounding Learning Tool (Google Finance)

And who knows? Your kids might even listen to you this time! If you’re lucky, they might even go on to write a few investment articles of their own. My best advice is for you to let them participate as business partners who help EARN the money through consistent discipline, saving and risk-taking.

Second, you can do what a lot of estate planners suggest – fund a trust but link distributions to the beneficiary’s accomplishments (like graduating college). That approach always seemed like tying the beneficiary up with financial puppet strings, but you’re not alone if you see the issue differently from the way I do.

Third, you can find the gift “sweet spot” – enough NOT to constantly worry about money, but not enough TO constantly worry about money. You’ll have to pinpoint that number for yourself, but if you succeed in doing so, then what I can tell you is that there are techniques to keep your gifts in the sweet spot… ESPECIALLY in the “best case” scenario where one or two of the investments go through the ceiling. For example, maybe you draft a trust with a clause that caps the total value of the trust at some inflation-adjusted level that you find reasonable, and then maybe kicks any excess funds out as charitable donations? Maybe you could even give your kids the power to direct which charities get any “excess” trust assets. Giving something back to society can be a wonderful form of motivation that unearned wealth could otherwise sap.

The fourth idea is the one that really matters the most because it’s the one you’ll come up with. You see, there is a reason why I told you that story about the young woman – which is actually a compendium of true stories that I’ve witnessed, experienced, or given advice on. In one guise or another, her story is not as unusual as you might guess. It might be yours one day, or your child’s. But having read the story, can you identify a few steps to avoid or mitigate some of the problems you think the character faces? If so, then you’ve just taught yourself something that even the best estate planners struggle with. Put those ideas of yours to good use when you plan to make gifts to your children or grandchildren.

Be the first to comment