James O’Neil/DigitalVision via Getty Images

Investment Thesis Summary

We are constructive on Esperion Therapeutics (NASDAQ:ESPR) heading into its FY22 full-year numbers, but are opting to wait for the earnings print before pulling the trigger, if at all. Shares have broken longer-term support lines despite positive top-line data around its Nexletol label in January. Looking back to February last year, at the time of its FY21 results, the company’s president and CEO, Sheldon Koenig, mentioned: “[w]e enter 2022 reinvigorated, as it will be an exciting year for Esperion as we expect to achieve 100% MACE accumulation of our unprecedented CLEAR Outcomes trial during the second half of the year and progress towards a topline readout in the first quarter of 2023.”

Twelve months later, and ESPR hit its mark on this. Data from the CLEAR Outcomes trial met its primary endpoint, and multiple secondary endpoints, creating a potential catalyst for those speculating on late-stage clinical assets to work from. The company has potential tailwinds in milestone payments should its Nexletol segment receive label expansion from regulatory authorities in the FDA and EU. Nevertheless, the market’s price response to this was soft, and many took profits or diverted capital from the stock in the weeks following. This makes us question if the stock has legs for a reversal, despite the quality data from its phase 3 studies. Net-net, we rate ESPR stock a hold for now, awaiting more data from its FY22 numbers. As a footnote, ESPR posted its preliminary Q4 revenue expectations in January, calling for ~$15mm in net product revenues at the upper end of the range.

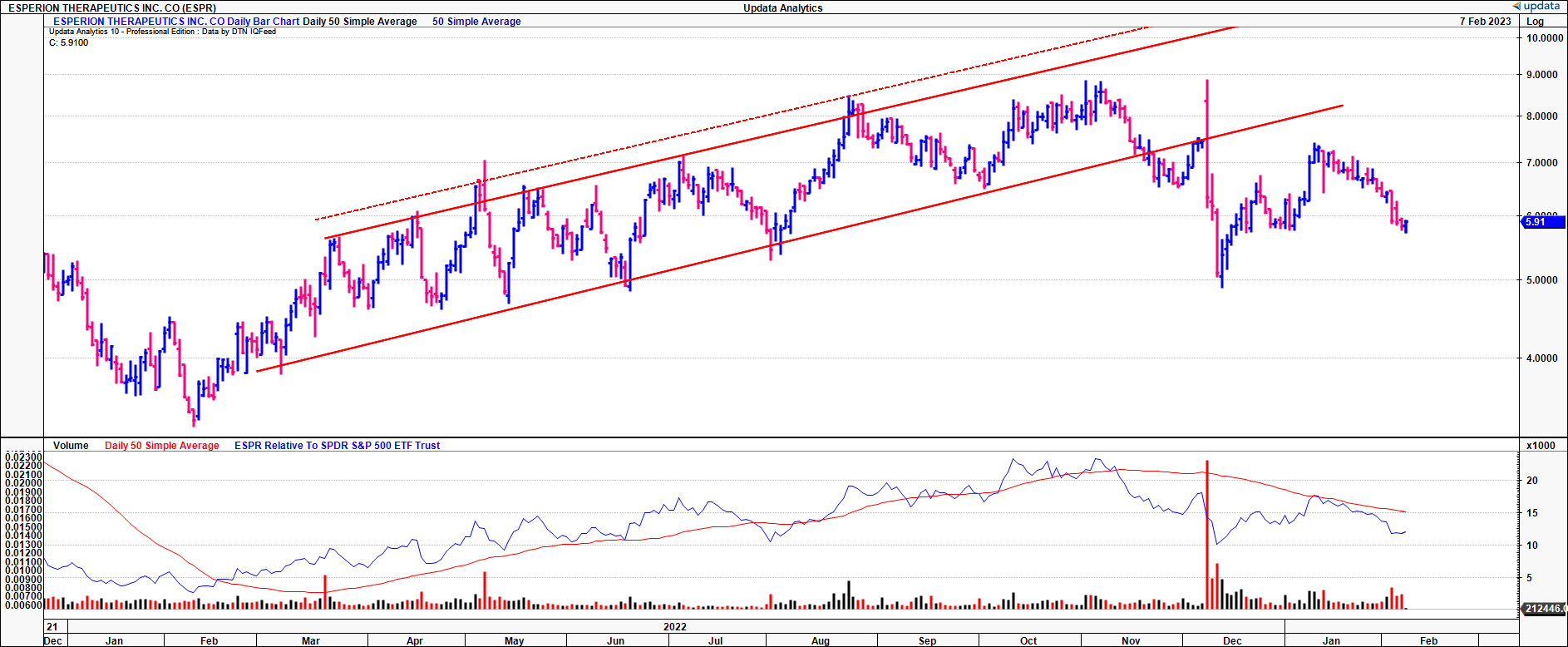

Exhibit 1. ESPR price evolution, FY22-date

Data: Updata

ESPR recent developments

The obvious price catalysts to move the needle for ESPR is the momentum around its Nexletol label. Nexletol [the underlying compound of which is bempedoic acid] is a novel lipid-lowering agent. It’s mechanism of action targets the inhibition of ATP citrate lyase, a critical enzyme in cholesterol biosynthesis. It aptly sits within a new class of drugs called ATP citrate lyase inhibitors. ESPR’s studies show its potential treatment for dyslipidemia and cardiovascular disease, particularly for patients with hypercholesterolemia, who remain at elevated risk despite being treated with maximum doses of statins and/or other lipid-lowering therapies. So far, it is indicated as an adjunct to diet and other lipoprotein inhibitors, especially in patients who are unresponsive to maximally tolerated statin therapy.

The CLEAR Outcomes trial, a Phase 3, double-blind, placebo-controlled, event-driven, randomized, and multicenter study, looked at the efficacy of Nexletol in reducing the risk of cardiovascular events (“CVEs”) in patients with documented statin intolerance and elevated low-density lipoprotein (“LDL”) cholesterol levels. The study involved over 14,000 patients from 1,200 sites in 32 countries. Top-line results posted in December illustrated that Nexletol met its primary endpoint. Per the release: “Bempedoic acid [i.e. Nexletol] becomes the first ATP citrate lyase inhibitor and first oral non-statin to meet the major adverse cardiovascular events (MACE-4) primary endpoint”.

However, it’s important to understand the compound still exhibited many identifiable adverse events (“AEs”). In fact, the CLEAR trial documented several AEs that were commonly observed in trial participants. The most prevalent reactions included upper respiratory tract infections, muscle spasms, hyperuricemia, back pain, abdominal pain, bronchitis, pain in proximal and distal extremities, anaemia, and elevated liver enzymes. Additionally, benign prostatic hyperplasia and atrial fibrillation were reported at a lower frequency, though still more frequently than with placebo. We question if this was a potential reason behind the sharp selloff immediately after the announcements.

With respect to tailwinds this year, the company expects to submit the dossiers from its CLEAR Outcomes trial to both the FDA and European Medicines Agency (“EMA”) during H1. As another potential tailwind, ESPR believes that it could be eligible to receive milestone payments from its collaborative partners, should it be awarded label expansion upon receiving any of these regulatory approvals in the US and Europe.

In a further effort to raise awareness of the benefits of LDL cholesterol reduction and cardiovascular health, ESPR entered into a strategic alliance with RFK Racing. The deal is structured as a 12-month marketing initiative, and will encompass a 360-degree advertising plan aimed at RFK’s 10mm fan base. This is a curious play. ESPR says that many of RFK’s fan base have been diagnosed with high cholesterol and other cardiovascular conditions. Hence, it hopes to convert potential patients from this ‘addressable market’. The key events under the collaboration include RFK’s major race event in February, sponsorship of the RFK Fan Day 5K road race, and other events dotted throughout FY23′.

ESPR technical positioning into FY22 earnings

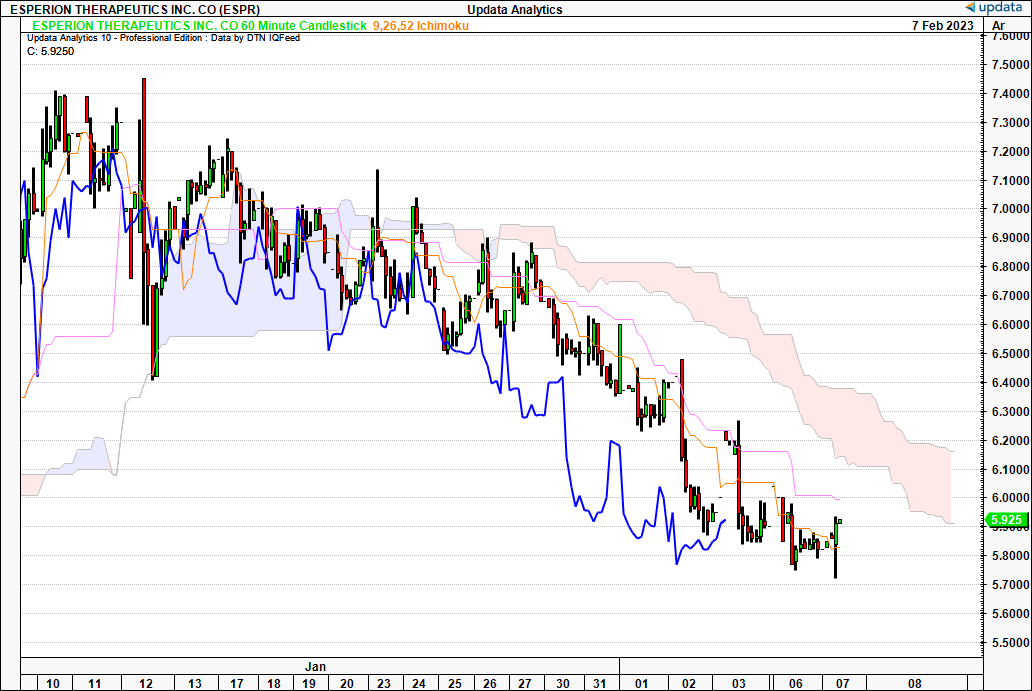

We are looking at multiple time frames in the below analysis. First, to understand what’s happening with the trend. On the 60-minute chart, that we use to look out to the coming days, shares are bearish below the cloud after crossing the cloud back in January. Both the price line and lagging line are positioned in bearish territory on this chart.

Exhibit 2. Bearish below cloud on 60-minute time frame

Data: Updata

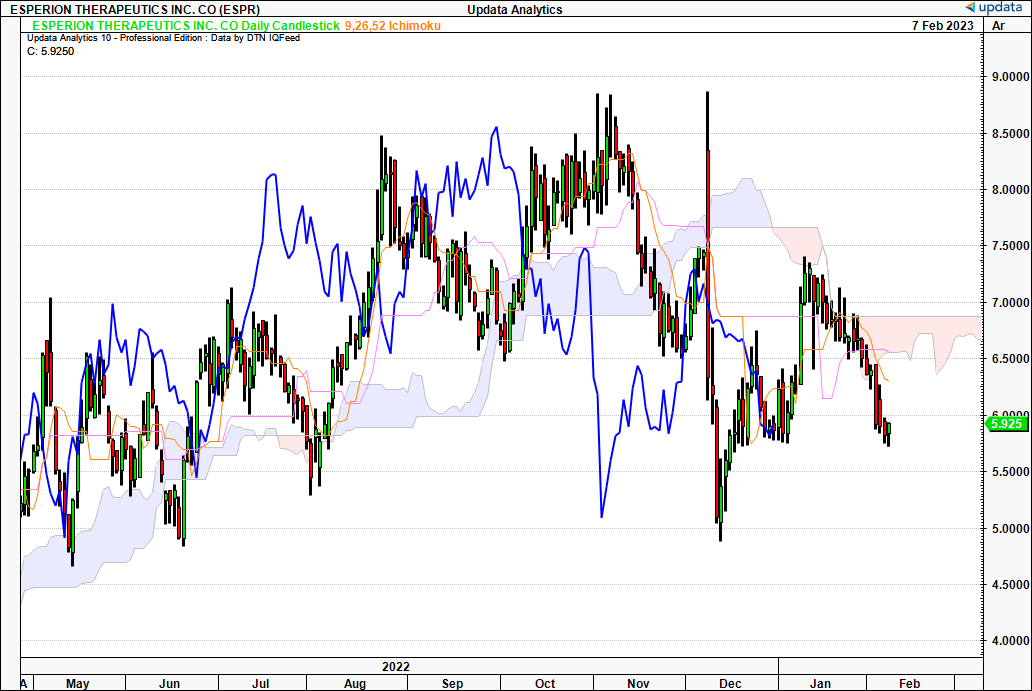

Turning to the daily chart, that gives us data on the distribution of probabilities into the coming weeks, with the latest price action we are also below the cloud here. Resistance is firm at ~$6.90. The price line tested the cloud in January but was rejected heavily despite several attempted breakouts. This is after a cloud cross back in October last year. Meanwhile, the lagging line hasn’t approached the cloud base since crossing back in October.

Exhibit 3. Again price and lagging lines positioned below the cloud despite attempted cross in January

Data: Updata

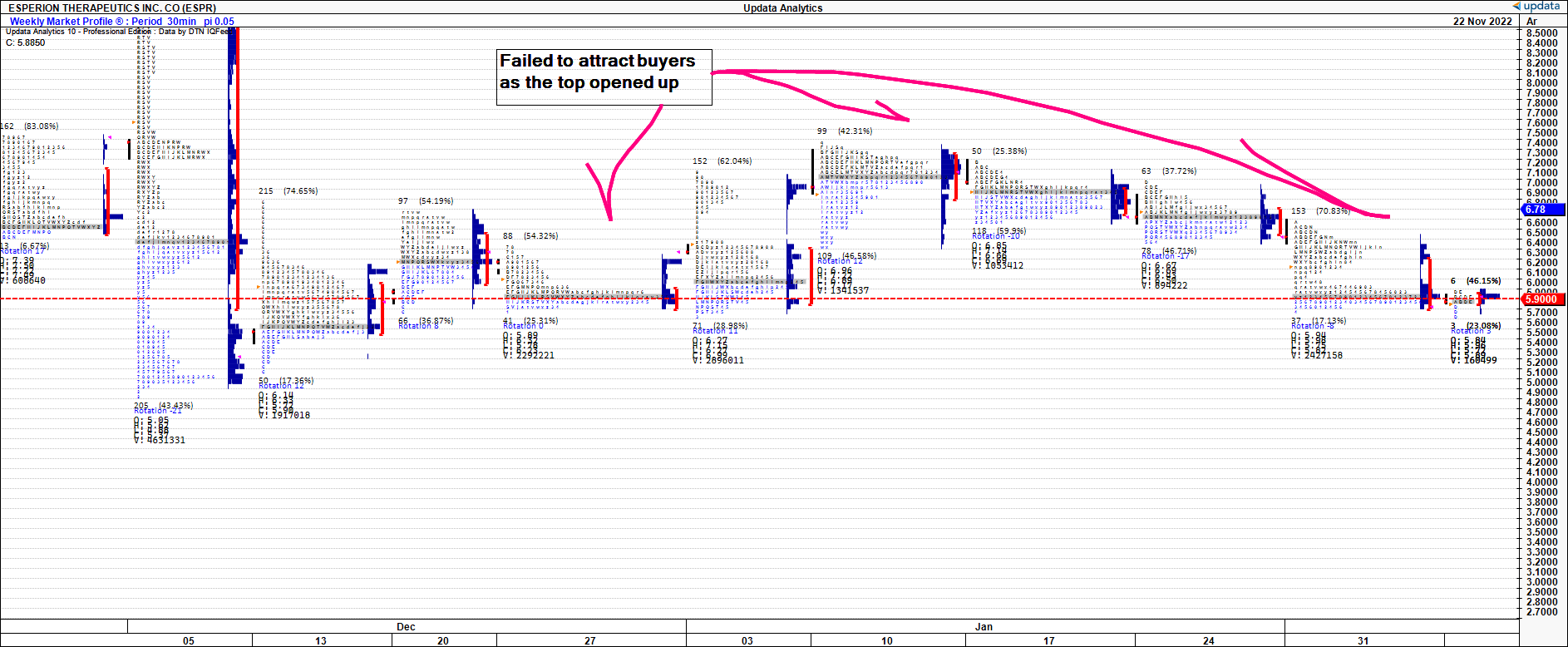

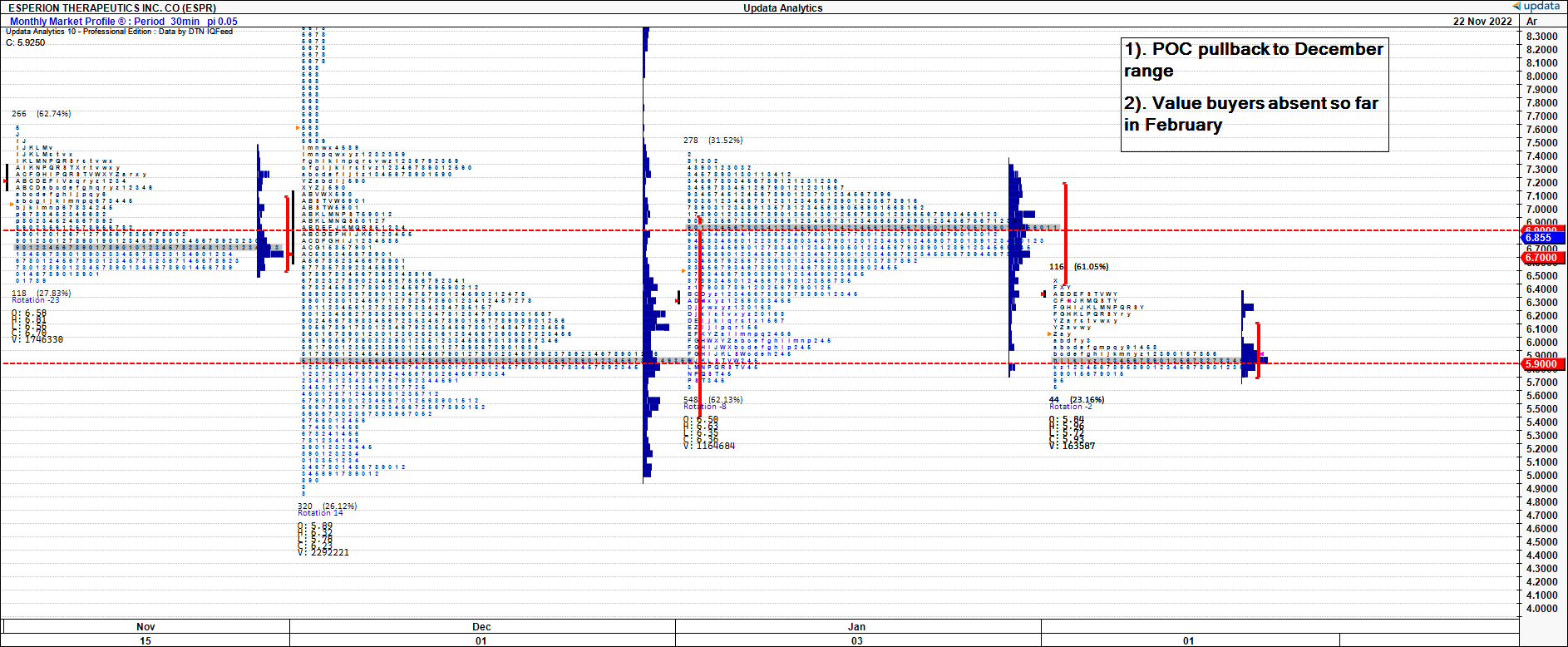

Looking at the weekly and monthly market profiles [Exhibit 4 and Exhibit 5, respectively] investors have repriced ESPR back to December range and found equilibrium at this mark. Demand has been thin in February so far. Value buyers have also been agnostic at the roll into February as well. As the top opened up on the rally in November, there wasn’t a surge of demand where investors saw an attractive entry point. As such, the point of control – i.e., the market’s estimate of fair value – is back at December range. We are less confident in its ability to re-rate higher on this market profile.

Exhibit 4. Weekly market profile, demand weak rolling into February

Data: Updata

Exhibit 5. Monthly market profile, point of control back at December range

Data: Updata

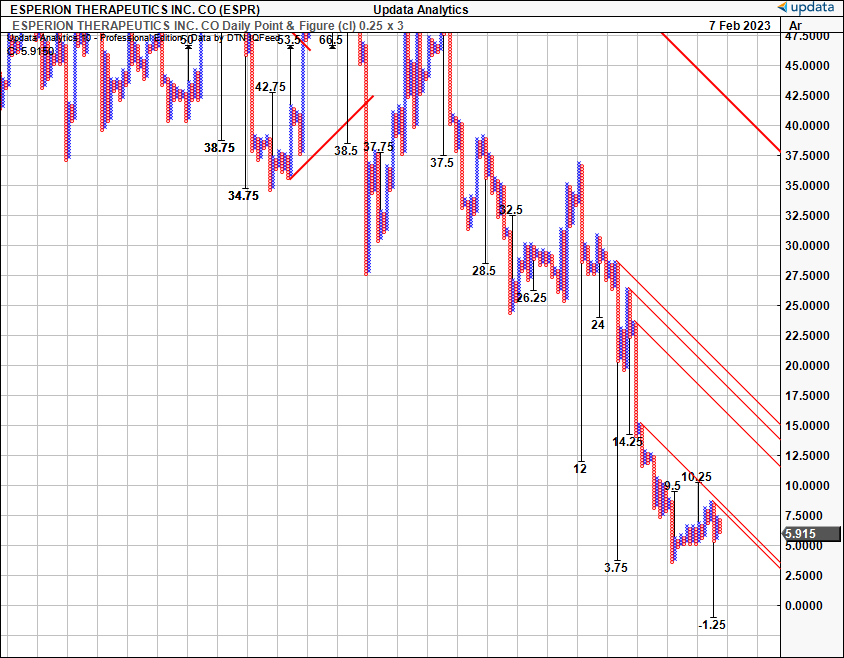

Consequently, we have limited upside priced in on our point and figure studies, and therefore, we see potential downside risk looking ahead. We are keen to wait for ESPR’s full-year numbers before examining the validity of these suggested price ranges.

Exhibit 6. Limited upside targets, downsides to $1.25 balancing investment debate

Data: Updata

In short

Whilst the Nexletol data is a net positive for ESPR stock, the market hasn’t responded in the same way. The corresponding price action tells us investors were chasing more in the results, or, that the upside had already been priced in earlier than the announcement. Moreover, the company’s preliminary Q4 results weren’t enough to reverse the downside, unlike last year when shares rose 9% on the same corresponding announcement. Consequently, we are awaiting the company’s full-year numbers before making any considered investment decision, but are trigger ready on this name. We encourage investors to adopt the same methodology.

Be the first to comment