On April 5, I covered the bull case for Arch Resources (NYSE:ARCH), one of North America’s largest coal mining companies. Since then, the stock is up roughly 12%, outperforming the S&P 500 by roughly 26 points. We’re now at a point where supply issues meet even higher demand as Europe is forced to go back to coal. Not only is natural gas too expensive, but pressure from lower Russian exports and expectations that Russia could halt all exports are also forcing coal power to return. While Arch coal has high metallurgical coal exposure, it benefits from strong pricing, a cheap valuation, and what could become a very cold winter.

Now, let’s look at the details!

We Need Coal!

On June 27, I once again dove into the depths of the European/Global energy crisis. As my daily newsletter is paywalled, I’m going to give you the most important parts that explain why coal demand is back.

Here are three headlines that I covered in my article:

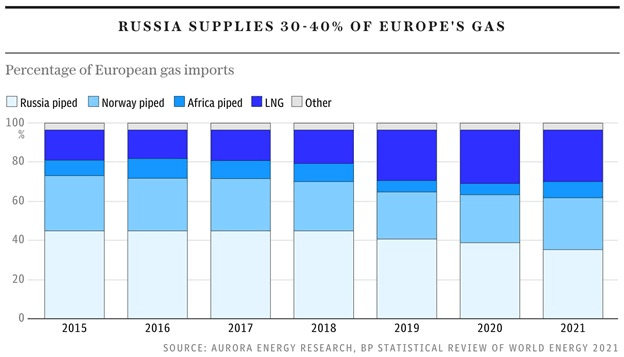

Essentially, we have a situation where Russia could cut off all natural gas exports to Europe. This means that Europe needs to find a replacement for close to 40% of its natural gas imports.

The Telegraph

Almost needless to say, that’s not an easy task. In fact, it’s not possible at all.

Right now, the European strategy consists of two aspects.

Hoping that Russia doesn’t shut off natural gas exports to Europe.

Saving as much natural gas as possible.

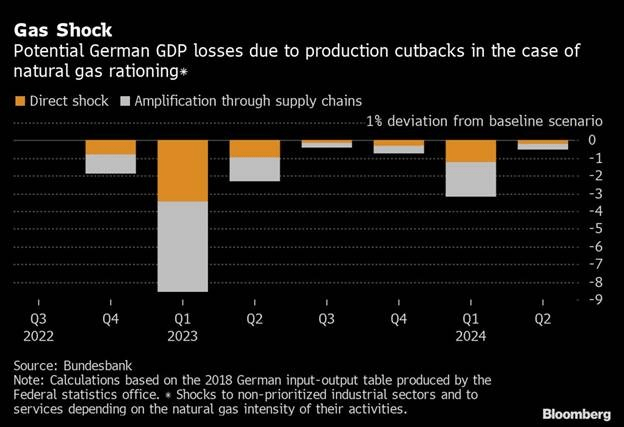

Why? Because a “gas shock” could look like this:

Bloomberg

The German economy alone could face a EUR 220 billion headwind, posing a bigger risk than the pandemic lockdowns. Personally, I think the situation could be even worse as natural gas is not just an energy source, but feedstock for a lot of chemical processes. The damage would be immense.

So, what does this mean? Saving natural gas can be achieved by reducing energy demand, but also by boosting coal production.

[…] Germany is not alone in its new embrace of the black stuff. Last week the Dutch government, led by Mark Rutte, scrapped limits on power production from coal-fired plants until 2024. And last weekend, Karl Nehammer’s government in Austria ordered a reserve gas plant to switch to burning coal; the Mellach station was mothballed just two years ago, when Austria became the second country in Europe after Belgium to go coal-free.

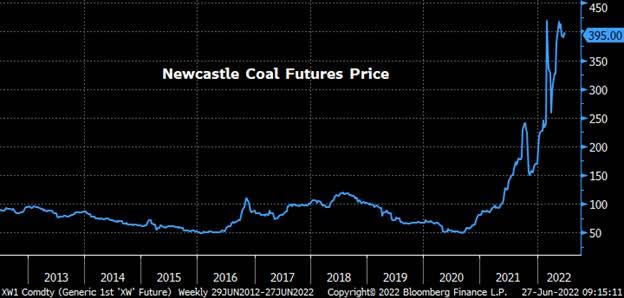

ICE Newcastle Coal futures show what is happening. Demand is higher than expected, and supply is an issue as I will show you in this article. Hence, coal is trading more than 5x above pre-crisis highs.

Bloomberg

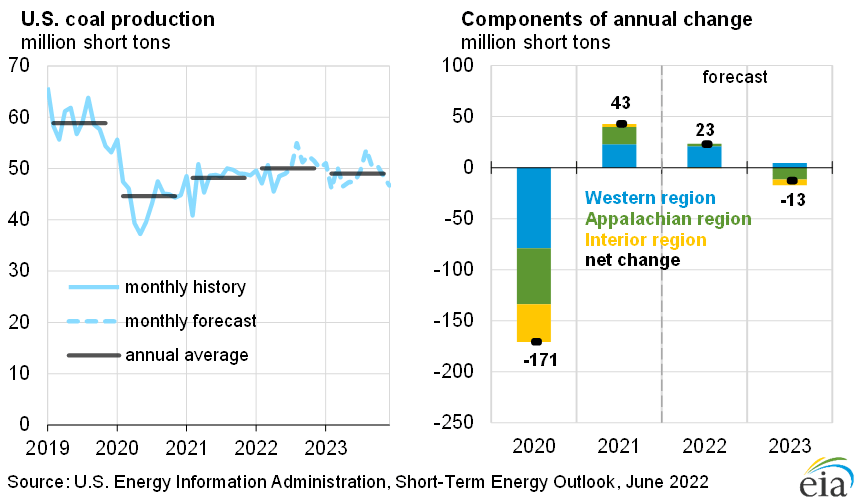

What’s interesting when looking at EIA data is that US coal production is not expected to pick up meaningfully. In fact, it’s expected to be stuck at 50 million short tons per year, which is below the 60 million short tons that were produced prior to the pandemic.

EIA

Moreover, it’s interesting that Europe – and Asia – are diversifying toward liquified natural gas (“LNG”). This allows Europe to become independent from Russia (slowly but steadily) and Asia to become less polluting. The problem is that the trend is slow and far from “climate-friendly”.

Between coal and the search for LNG, the ESG trend (environment, social, and governance) is in a very bad spot. One could say it’s dead – for now.

This is where Arch Resources comes in.

ARCH Is Still Cheap

The company, formerly known as Arch Coal is a $2.42 billion dollar coal heavyweight. As I wrote in my April article:

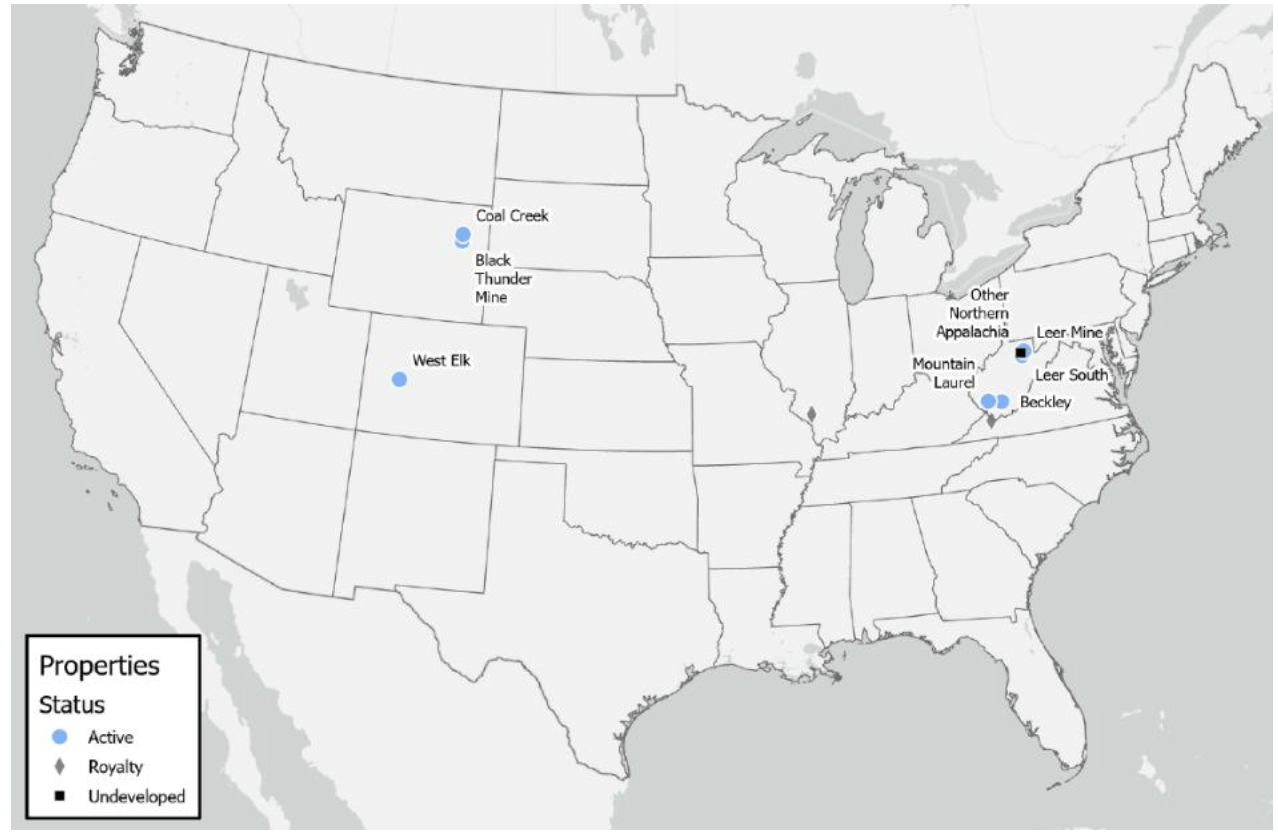

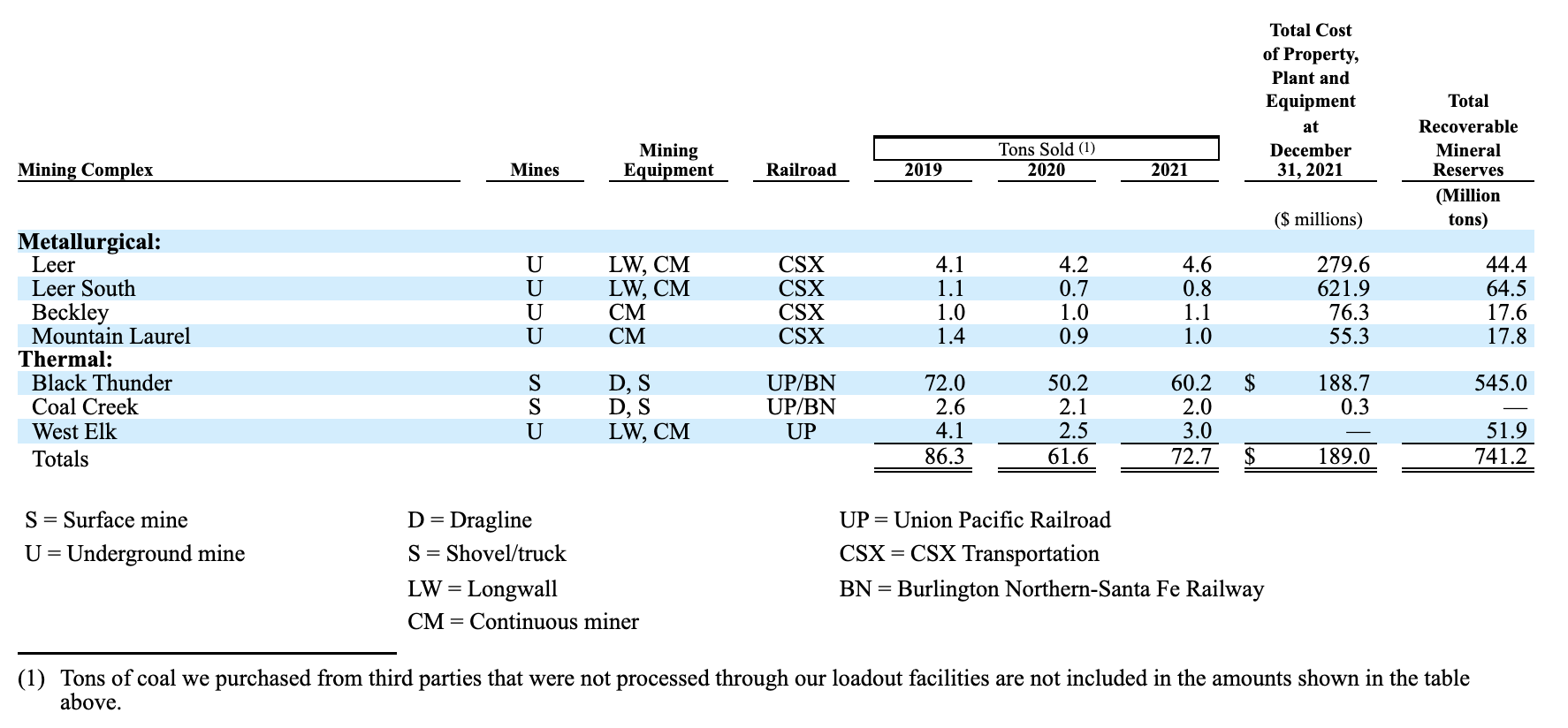

Arch produces roughly 11% of the total annual US metallurgical coal supply, which was estimated to be close to 65 million tons in 2021. The company sold its product to six North American customers and exported it to 24 customers overseas in 15 countries last year. All of the company’s metallurgical coal is produced in the state of West Virginia. Thermal coal is produced in Wyoming and Colorado.

Arch Resources (via SEC 10-K)

This year and going forward, Arch aims to generate 80% of its EBITDA from metallurgical coal. Note that thermal coal volumes are higher, but due to lower margins the impact from metallurgical coal is higher.

ARCH is very export-focused. The company plans to ship 95% of its 2022 coking coal output into the 300 million metric tons per year global seaborne metallurgical market. The company benefits from great infrastructure including rails and export facilities as well as long-term contracts with steel producers and related.

What’s interesting is that I own shares in two of three railroads that service the company’s mines: CSX Corp. (CSX) and Union Pacific (UNP). BNSF is owned by Buffett.

Arch Resources (SEC 10-K)

Roughly half of its output is destined for Asian buyers.

It also helps that the company has access to affordable production. For example, its Leer mine produces at cash costs of less than $50 per ton. That’s among the cheapest producers in the world.

Moreover, EBITDA in the company’s thermal segment has exceeded capital spending by 8x since 2016. The company expects this to widen further thanks to better thermal coal prices as I discussed in the first part of this article. If anything, this tide lifts all boats. Both metallurgical coal and thermal coal are experiencing accelerating tailwinds as supply simply isn’t there.

Arch estimates that global coking coal demand will be 335 million metric tons in 2026. Supply is estimated to be 277 million metric tons, incorporating current operations and depletions. In other words, 58 million tons of supply need to be found.

On a side note, in its calculations, ARCH used a 2% annual depletion rate, which is conservative.

Bringing back coal isn’t easy. Both coking and thermal coal production are “dirty” and while politicians move back to coal, none of them want to commit to bringing back supply on a long-term basis. That would hurt their ESG goals and climate commitments. Even coal leader Australia is reducing output. In 2021, output was 168 million metric tons. That’s down from 184 million tons prior to the pandemic.

As I explained in a lot of prior articles, one way out of the energy crisis is to acknowledge that we need coal (and oil). I’m not at all a big fan of coal and I think moving to cleaner energy is important. However, I’m not someone who likes forced climate targets and related issues. The transition needs to be very gradual in order to avoid supply shortages of any kind and to avoid hurting coal communities and affordable energy sources.

The way “we” do things now is ending in a total disaster.

Valuation

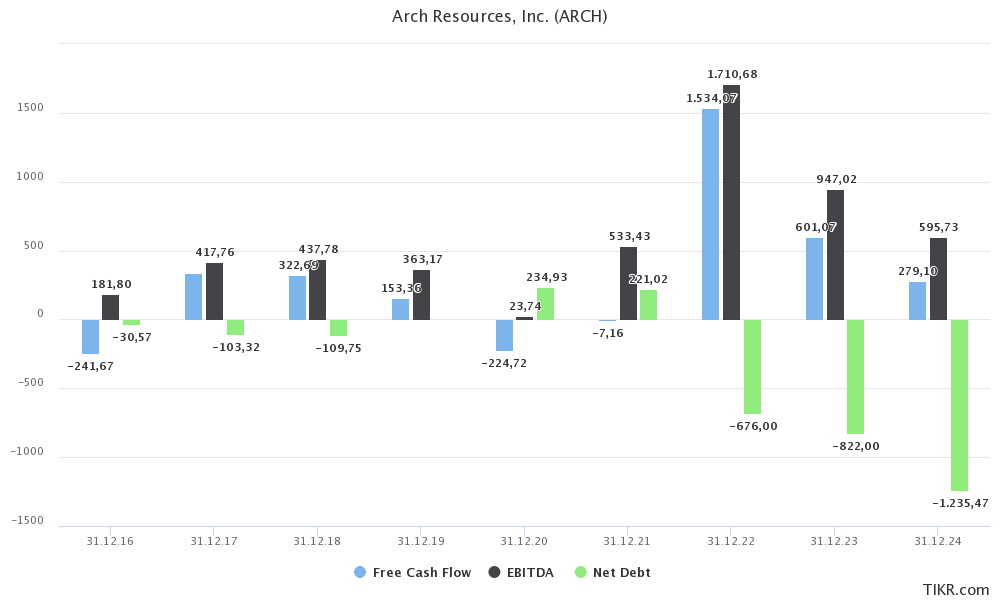

Even if coal prices implode next year (not a prediction), this year is turning into a total blessing – financially speaking. Arch is on track to do more than $1.5 billion in free cash flow, more than half of its current market cap. Adjusted EBITDA is expected to come in at $1.7 billion. That’s more than many prior years combined. As a result, net debt could fall to minus $680 million.

TIKR.com

In April – of this year – estimates were that free cash flow would be $1.0 billion. That’s a 50% adjustment in just a few months.

In this case, giving the stock a valuation isn’t easy. I don’t want to use 2022 estimates as this will clearly be a “one-off” year. Coal will remain strong, I believe, but 2022 is shaping up to be an outlier.

If we assume that 2022 will be good, we can use the lower (expected) net debt load and next year’s EBITDA – assuming that analysts are wrong about the decline in coal prices in the year ahead. Just like they missed coal’s upside potential this year given their aggressive adjustments.

So, using the $2.42 billion market cap, $680 million in net cash (negative net debt), $75 million in pension-related liabilities, and $950 million in expected EBITDA gives the company an enterprise value of $1.8 billion, and a 1.9x EBITDA multiple. This could have been even lower if I used next year’s net debt expectations. This gives us a margin of safety.

1.9x is incredibly cheap – even for a coal company. The multiple would still be fair if I used the market cap instead of (lower) enterprise value and 2024 EBITDA estimates (4.0x valuation).

Given these numbers, I believe that ARCH has at least 50% more upside. This can be gradual over the next 6-12 months or “suddenly” when things started to worsen in the global energy market.

After all, this continues to be a headline-driven market with regard to the war in Ukraine and supply-related headlines.

Takeaway

A while ago I wrote that coal is back. Arch Resources’ EBITDA (and related) estimates are rapidly rising as there’s no way around coal anymore. The ESG playbook has been thrown out of the window as even the most climate-committed countries in the world are now going back to coal energy in order to lower natural gas demand.

There is no way around the use of coal anymore as American, European, and Asian customers are accelerating demand. One of the biggest beneficiaries is ARCH. The company has an export-oriented business model and benefits from both high margins in metallurgical coal and accelerating thermal coal demand.

Its balance sheet has become extremely healthy, which is helping the company’s valuation.

ARCH is extremely attractively valued, which makes my 50% upside estimate rather conservative.

That being said, coal is extremely volatile and the long-term outlook is uncertain. If you’re not a trader, don’t start trading coal now – for your portfolio’s safety. One goal of this article was to inform people about the energy/coal market. Trading coal stocks is something only experienced traders should do.

FINVIZ

If you decide to buy ARCH, keep your position limited.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment