sl-f

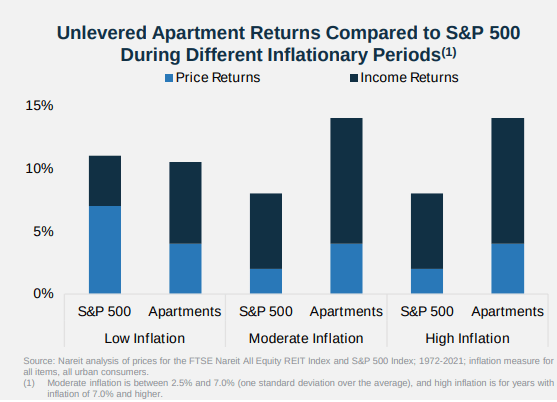

As we stated in our initial coverage of Equity Residential (NYSE:EQR), we like high-quality apartment REITs because they tend to outperform the S&P 500 index (SPY) during periods of higher inflation. Back in August when we started coverage we believed shares were reasonably valued at ~$75. With shares now closer to $64, and the company delivering solid Q4 results and 2023 guidance, we believe there is a clear margin of safety in the valuation, and we are therefore upgrading our rating to ‘Strong Buy’.

Equity Residential Investor Presentation

In 2022 Equity Residential delivered same-store revenue growth of 10.6%. This strong same-store revenue growth combined with modest expense growth of 3.6% resulted in a 17.7% increase in year over year normalized FFO. The company is guiding for another strong year in 2023, above their long-term average, but certainly not as strong as 2022. Guidance is for same-store revenue growth of 5.25% at the mid-point. The midpoint of their same-store revenue guidance assumes a 90 basis point reduction in revenue growth due to the impact of bad debt and lack of rental relief payments. The company sounds confident in achieving this level of growth given the significant embedded growth of about 4.2% from leases written in 2022 and an above average loss to lease. Equity Residential is guiding normalized FFO to be $3.75 per share at the mid-point which would imply more than 6% year over year growth. This puts the forward valuation based on P/NFFO at ~17x, which we believe is quite attractive considering the growth Equity Residential has been delivering. The company also looks quite attractive on a price to NAV basis.

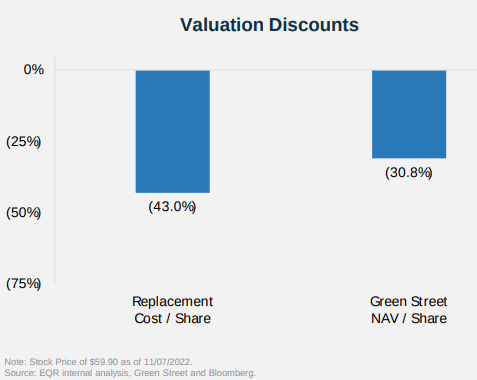

Net asset value

In its November investor presentation Equity Residential pointed out that their share price was ~43% below the replacement cost per share, and roughly 30% below the Green Street net asset value estimate. As the share price was $59.9 at the time, this would imply a replacement cost per share of ~$105 and NAV/Share of ~$86. Given that the share price is currently ~$64, this leaves a very nice margin of safety for investors.

Equity Residential Investor Presentation

This is something that CEO Mark Parrell addressed during the Q&A session of the most recent earnings call. An analyst asked a question about potential buybacks, and Mark Parrell replied that given the large discount to NAV it at least means they will be more careful about issuing new equity at these prices.

When we see our stock price when it’s trading at such a material discount to NAV like it is now as, is a signal not to use the equity markets to fund growth. That’s what we see it as. And that’s very clear to us. But we do talk to the Board about buybacks periodically, and it’s not like sort of categorically off the table. But again, it’s more of a financial maneuver. And if you don’t do it in size, it’s not terribly meaningful. And the last comment is I’ve watched a lot of REITs buy back meaningful amounts of stock usually away from our sector. And it hasn’t proven to have turned out all that well. I think it’s better used as an indicator of when not to issue equity than it is to go whole hog on some giant share buyback.

Balance Sheet

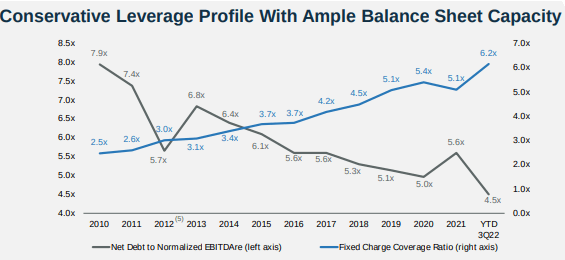

Equity Residential continues to have one of the best balance sheets of the REITs we follow, and this is reflected in its strong credit ratings (A-/A3). It also has low floating rate exposure, the lowest leverage in its history, and significant liquidity/debt capacity. This positions Equity Residential well to act on potential attractive acquisition opportunities if they present themselves.

Equity Residential Investor Presentation

Valuation

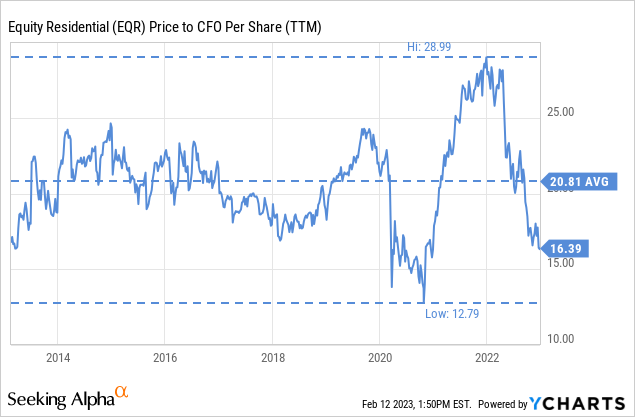

Equity Residential is trading with more than a 20% discount to the ten year average price to cash flow from operations per share. Similarly, it is trading at a more than 20% discount to the estimate NAV per share of ~$86, and an even bigger discount to the replacement cost per share.

The dividend yield is close to 4%, while the ten year average is closer to 3%. The forward price to normalized FFO is ~17x based on the company’s recent guidance. As a result, we believe shares are currently trading with a margin of safety of more than 20% to fair value, and can therefore be considered a ‘Strong Buy’ at the moment.

Risks

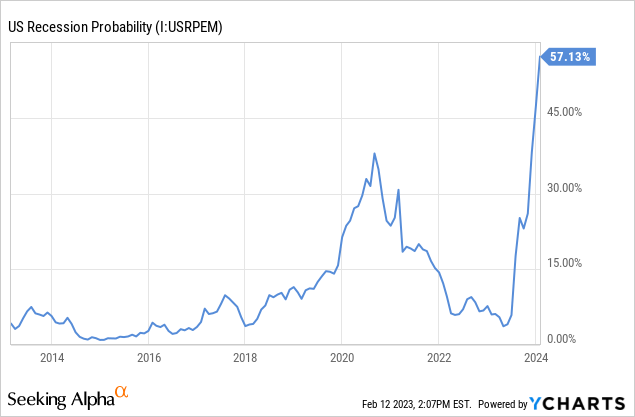

A severe recession would make it difficult for the company to meet its guidance, putting pressure on rents and occupancy. Some recession models are putting the probability of a recession arriving soon very high, such as the Estrella Mishkin model. That said, Equity Residential has a very solid balance sheet and an affluent tenant base that would likely mitigate the impact and allow the company to navigate through the downturn.

Conclusion

Equity Residential delivered record results for 2022, and gave very solid guidance for 2023. Despite this, the share price has remained relatively weak, and we now see the shares as significantly undervalued. This was further confirmed by the CEO commenting during the earnings call that they will likely avoid share issuances at such large discount to NAV. There is the risk of a recession arriving soon, but even if that happens the company has a strong balance sheet and an affluent tenant base that would mitigate the impact. We are upgrading our rating to ‘Strong Buy’ based on the recent results and the valuation being considerably more attractive compared to that of our last article.

Be the first to comment