Gearstd

Investment Thesis

EQT (NYSE:EQT) is a cheaply priced natural gas player. That’s the headline. The more nuanced analysis describes the bear and bull case facing natural gas.

On the bearish side, we have unseasonably warm weather, together with analysts lowering their near-term revenue estimates for EQT.

On the bull side, there’s the great energy transition and governments’ call for energy security.

This is my core argument, EQT is priced at 4x free cash flow. It’s this cheap due to the prevailing view of the natural gas market in 2023 will not be as strong as it was in 2022.

However, I declare that contrary to popular opinion, as long as natural gas averages around $5.00 per mmbtu, EQT is going to be a very strong investment this year.

A Mismatch in Understanding

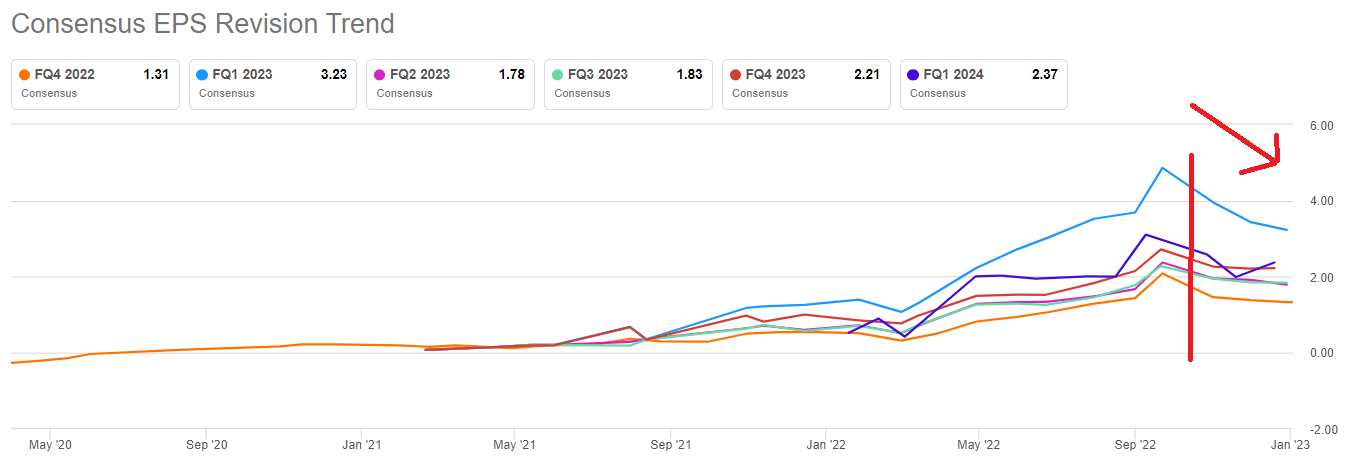

There are a couple of elements that I believe we should discuss. In the first instance, consider the graphic that follows showing analysts’ expectations for EQT’s revenue growth rates.

EQT’s revenue estimates.

What you see above is that in the past several weeks, analysts have been downward revising EQT’s revenue estimates. And I make the case that these downward revisions don’t make much sense.

Particularly the ones for Q2 and Q3 2023. And I’ll get to why in a moment. But before that, I wish to put a spotlight on another headwind facing EQT’s prospects. A that is of unseasonably warm weather.

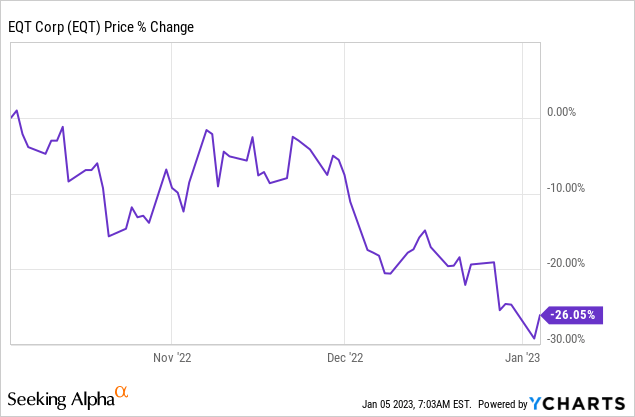

Clearly, these two drivers, when combined, are too much for investors and these have weighed down on the share price.

As you can see above, in the past 3 months, EQT has lost a quarter of its market value. Now, this is where I disagree with the bear thesis.

I’m going to talk about the great energy transition. Then, I’m going to talk about energy security. And after that, I’m going to particularly address how EQT valuation and how shareholders should think about their investment.

The Great Energy Transition

I’m not a demagogue. I have no interest in remarking on the seemly futile efforts of the green agenda. Similarly, I’m not here to blame anyone for trying to make the world better by reducing carbon emissions.

In fact, this is what I declare. Natural gas is the cleanest of the fossil fuels. It’s a bridge that will empower our transition from a stronghold dependency on coal and fossil fuels to cleaner energies.

This will include onshore wind, solar panels, and nuclear energy, as primary components, plus natural gas as a backup baseload provider.

With this context in mind, I want to now discuss the all-important aspect of energy security.

Energy Security, an Unquenchable Thirst

In the past five years energy was cheap. Energy was abundant. We all benefitted from access to reliable energy. Today, the same cannot be said.

There’s a direct correlation between access to cheap energy and quality of life. Or put another way, poor access to energy leads to energy poverty and low quality of life.

Governments around the world are recognizing this as a fact. And the only way to tackle this is by working hard to increase supply. And yet, for now, it appears that governments are coming around to the idea of the importance of cheap energy, but working through a balancing act of increasing fossil fuel production and a green agenda.

Hence, this is my point, we will continue to need more and more energy to service our unquenchable thirst for energy.

With all this in mind, I would like to believe that I have succeeded in articulating and laying out for readers, that the demand for natural gas isn’t about this week or next week, and how the natural gas market will navigate through the unseasonably warm weather.

As a point of fact, natural gas is a secular growth story. And EQT is very well positioned to benefit from this tailwind. Consequently, I now turn our discussion to EQT’s stock valuation.

EQT Stock Valuation — 4x Free Cash Flow

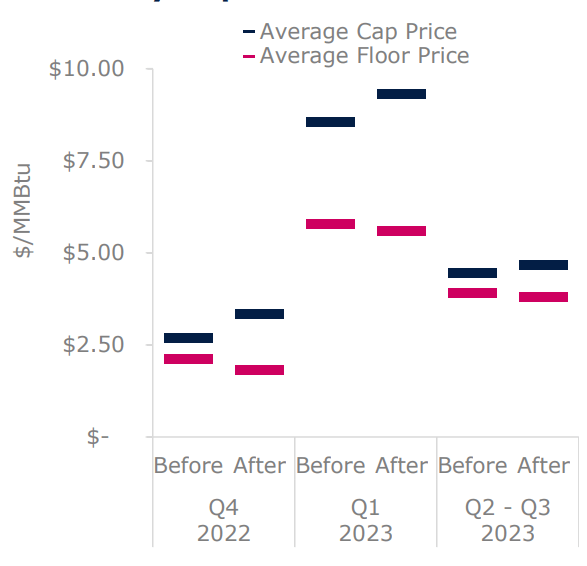

Before going much further we should keep in mind that EQT’s 2023 book is approximately 60% hedged at $5.65 per mmtbu.

EQT Q3 2022 presentation

That means that its ability to forecast its 2023 free cash flows is relatively straightforward and predictable.

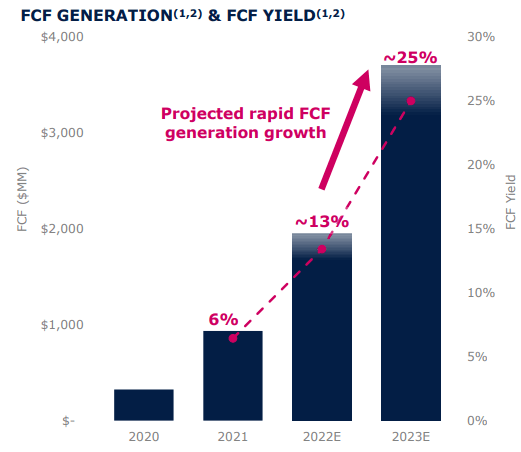

Accordingly, as you can see in the graphic that follows, EQT’s free cash flow is guided for approximately $3 billion in 2023.

EQT Q3 2022 presentation

Thus, the stock is being priced at somewhere close to 4x free cash flow. Outside of energy, I believe that investors will not find many sectors that offer investors a more than compelling risk-reward profile.

The Bottom Line

In sum, natural gas demand is going to continue to move higher over the next year. It’s not about the warm weather next week.

Meanwhile, the one blemish to the bull thesis is that EQT carries just under $5 billion of free cash flow.

What that means in practice, is that EQT will have to continue to shore up cash so it can chip away at its debt, before its able to commit to higher dividends.

Be the first to comment