Mongkol Onnuan

Enterprise Products Partners (NYSE:EPD) is the 3rd most followed pipeline company on Seeking Alpha, which has amassed 130,320 followers. Stability is one of the most important aspects for income investors as the investment thesis is geared toward dependable income production. EPD has just provided its 24th consecutive year of distribution increases and continues to reward its investors by increasing the amount of capital returned. In addition to increasing the distribution by 3.2%, Wolfe Research raised its outlook on units of EPD to outperform with a $27 target. There isn’t much to dislike as management is aligned with investor interests, owning 32% of common units, while EPD has a distribution yield of 7.74%. I believe the future looks bright for units of EPD as the energy landscape sets up well for their operations. Investors can rest assured that the distributions will continue to flow into their accounts as traditional sources of energy are not disappearing anytime soon.

Enterprise Products Partners

Investors just received a 3.2% Distribution increase from EPD

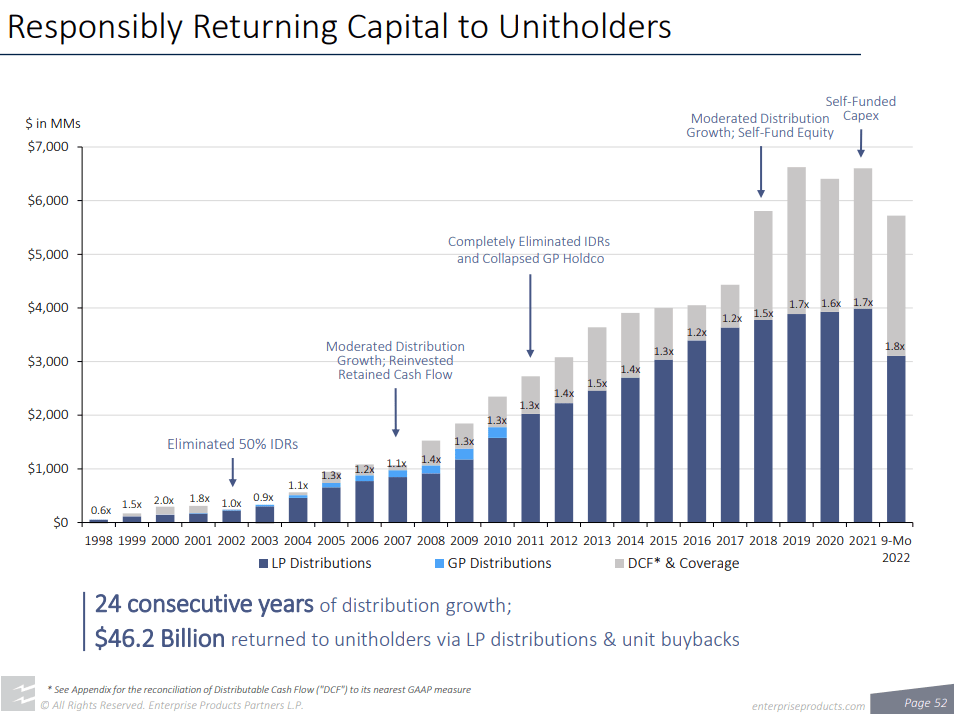

EPD has become a quintessential income-producing asset that can find a place within any diversified portfolio. Since going public in 1998, EPD has provided investors with 24 years of consecutive distribution growth. In many years, the distribution growth came at a quarterly rate rather than annually, which increased the compounding effects of reinvesting the distributions. EPD has returned $46.2 billion to unitholders through distributions and buybacks since 1998. Over the past decade, EPD has operated at an average DCF coverage ratio of 1.49x, and over the past 5 years, this has increased to an average DCF coverage ratio of 1.66x.

The grey portion of the bars in the chart below is important to incorporate into an investment analysis. Buybacks, distributions, and growth projects are financed from EPD’s distributable cash flow (DCF). After the distributions are paid, the retained distributable cash flow is the bucket of capital used to finance future growth. EPD self-funds its expansion into new projects with the goal of increasing the amount of DCF it generates over time. The areas I look at are the actual coverage ratio of the distribution and the level of annual DCF generated. EPD has increased its margins which enhances the margin of safety in its distributions as its producing much more DCF than it distributes to unitholders. When the coverage ratio increases, this also means that the pool of capital left over increases since EPD’s distribution hasn’t fluctuated to the downside. In the first 9-months of 2022, EPD’s coverage ratio was 1.8x, the largest ratio since going public. If EPD can maintain or exceed this ratio after the Q4 results, I believe it will have a positive impact on the unit price itself.

Enterprise Products Partners

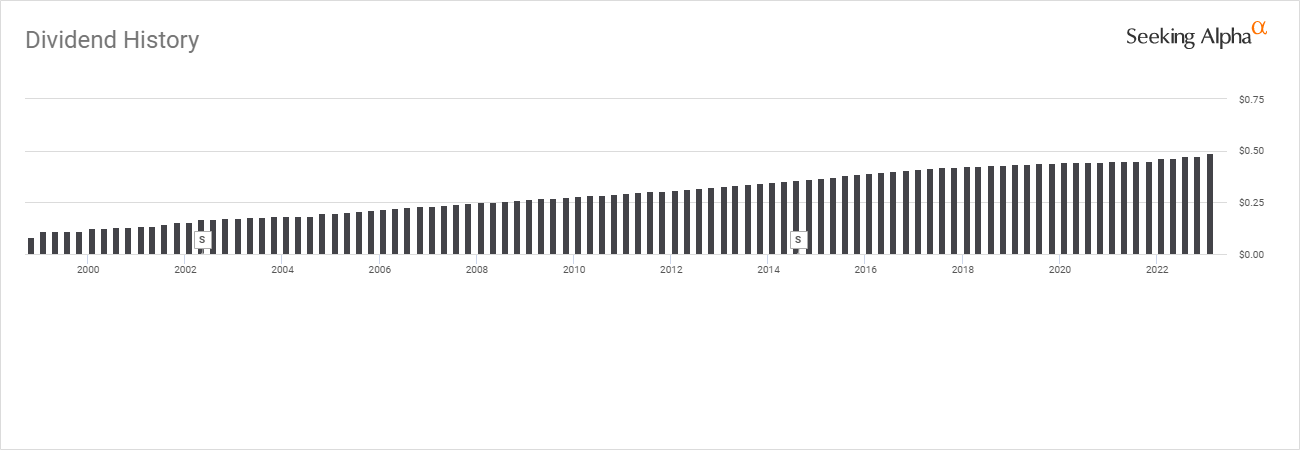

Since going public in 1998, EPD’s quarterly distribution on a split-adjusted basis has increased by 512.5%. The quarterly distribution grew from $0.08 in 1998 to $0.49 after the recent increase. Unlike many companies that raise the distributions or dividends on an annual basis, the chart below illustrates that most of the distribution growth came from quarterly increases. Based on the DCF growth and the current coverage ratio, there is no reason to believe that this trend will stop or reverse course anytime soon. EPD generated a 1.6x distribution coverage ratio in 2020 when several oil & gas companies filed for chapter 11, reduced their dividends, or halted future increases.

In a macro environment that has caused significant headwinds for companies, and yield is easy to find, EPD is well positioned for the future. The Fed has eradicated the yield-starved environment that investors were used to, and now anyone can achieve yields that exceed 4% without risk being associated with the investments through 2-year treasury notes or CDs. There is less of a reason for income investors to invest in equities that generate less than 4% as they’re taking on additional risk for no reason. EPD’s price will fluctuate, but from an income perspective, income investors can be confident that the distributions will continue flowing into their accounts every quarter from EPD, and the yield will exceed risk-free assets for the foreseeable future.

Seeking Alpha

The world needs fossil fuels, and EPD is positioning itself to benefit from 8 projects coming online in 2023 and several others in the following years

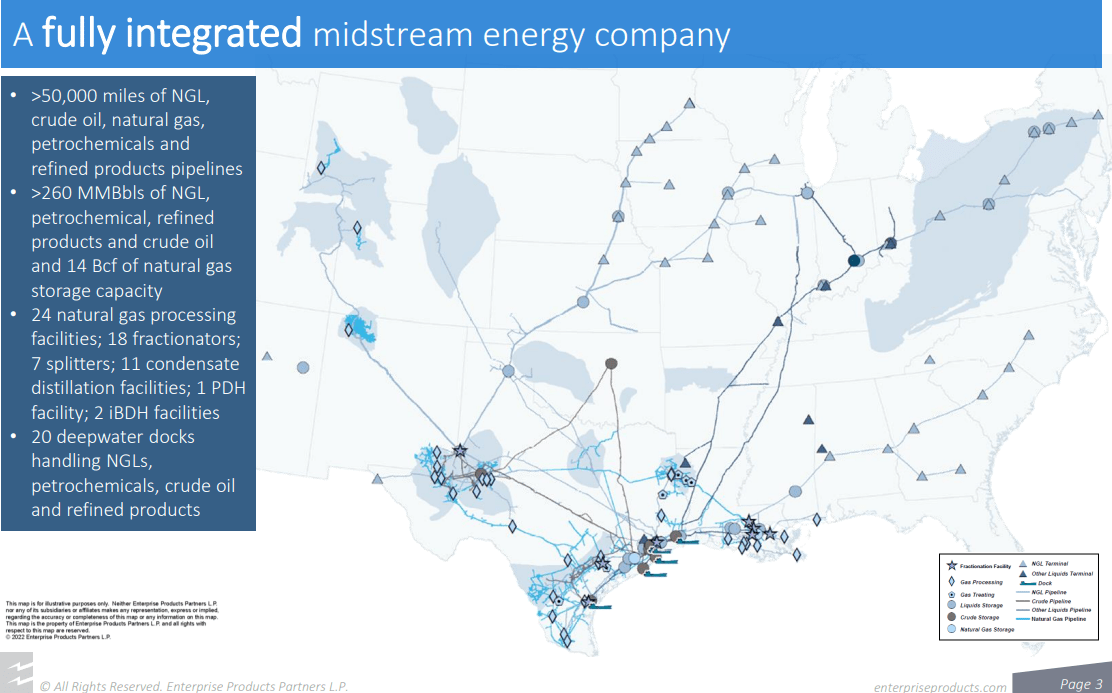

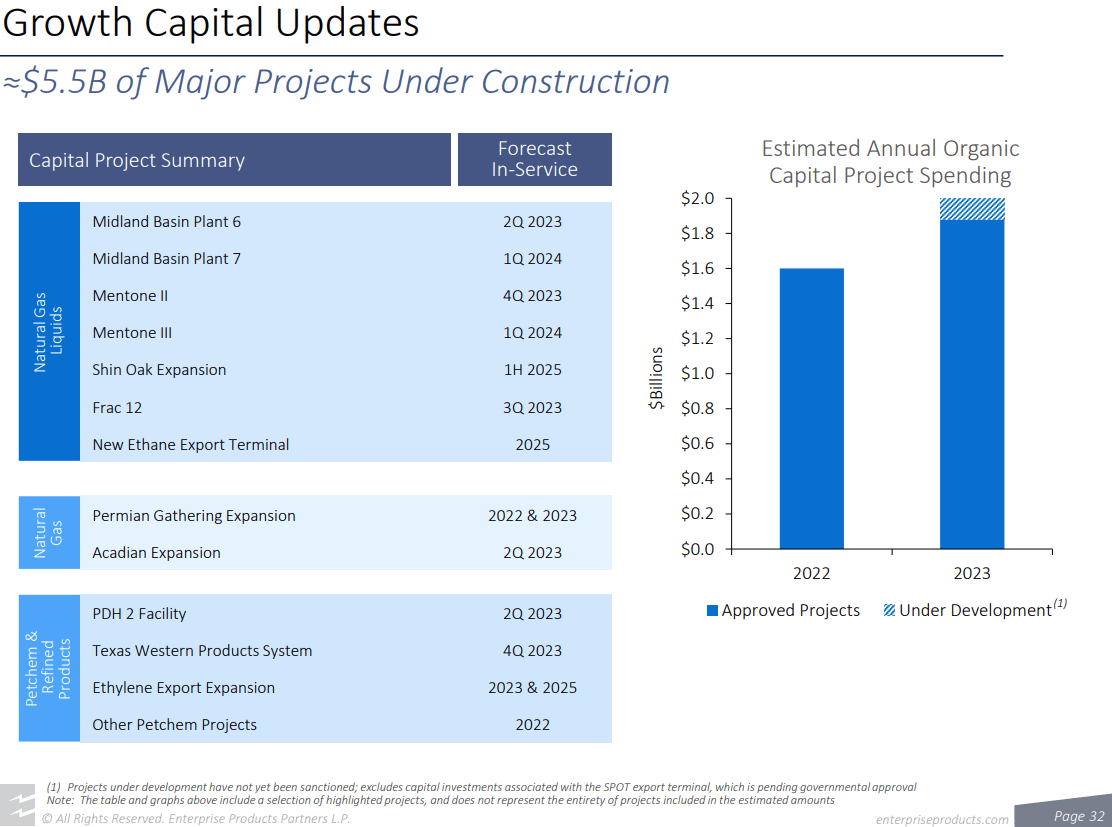

EPD has over 50,000 miles of pipelines carrying crude, natural gas, petrochemicals, and refined products. Within its expansive network, EPD has 260 MMBbls of NGL, petrochemical, refined products, and crude storage, in addition to 14 Bcf of natural gas storage capacity. EPD also has 24 natural gas processing facilities, 18 fractionators, and 20 deepwater docks providing exporting capabilities. In 2023 EPD has 3 NGL projects coming online, 2 projects from their natural gas segment, and an additional 3 products in petrochemical and refined products.

EPD has returned over $45 billion in capital to its investors since its IPO

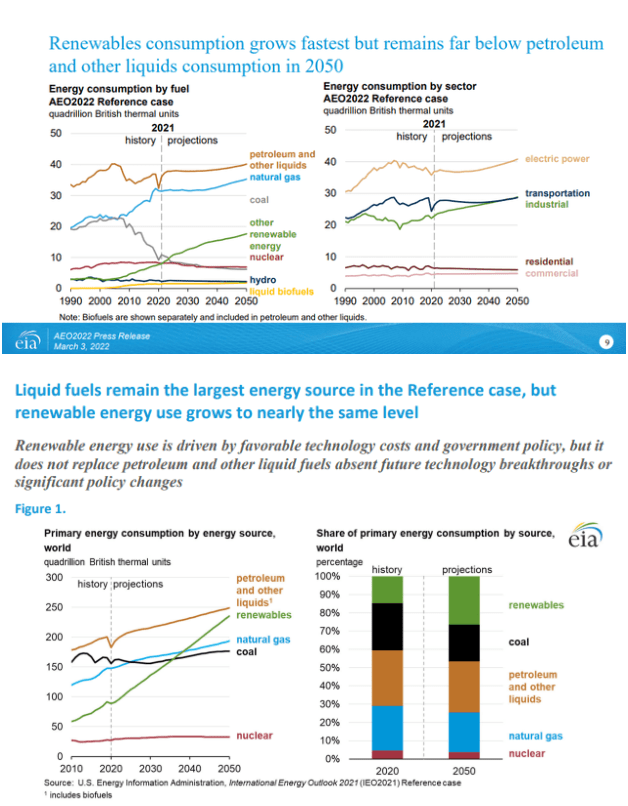

On 3/3/22, the EIA released its 2022 Annual Energy Outlook and concluded that petroleum and natural gas remain the most consumed sources of energy in the United States through 2050 (1st slide below). The EIA publishes its international energy outlook every 2 years, and the last one was published prior to the war in Ukraine. In their baseline case, the global energy demand would increase by 50%, growing from 600 quadrillion BTUs in 2020 to 900 quadrillion BTUs in 2050. In 2050 the global energy mix per the EIA isn’t a scenario where renewables replace or displace oil & gas but an energy mix that incorporates all sources of energy. Petroleum and other liquids are projected to remain the largest energy source, followed by renewables, then natural gas. From now through 2050, oil & gas will both increase their consumption rates in the global energy mix.

EIA

In Q3 of 2022 EPDs Crude pipeline volumes increased by 6.35% YoY while marine terminal volumes increased 13.33%, natural gas pipeline volume increased 19.86%, NGL fractionation increased 7.69%, Propylene plant production increased 5.21%, fee-based natural gas processing increased 30%, and equity NGL-equivalent production increased 21.33%. EPD achieved a record of 11.3 million bpd/e of NGLs, crude oil, natural gas, refined products, and petrochemicals being transported.

The projected growth in natural gas is critical to boosting EPD’s DCF. In Q3 EPD’s gross operating margin from the NGL Pipelines & Services segment was $1.3 billion, an increase of 27% YoY. Over the past 12 months, NGL Pipelines & Services has accounted for $4.96 billion of EPD’s $9.07 billion in total segment gross operating margin. There are 3 NGL projects coming online in 2023 and 2 in 2024 and will continue to separate EPD from other midstream operators.

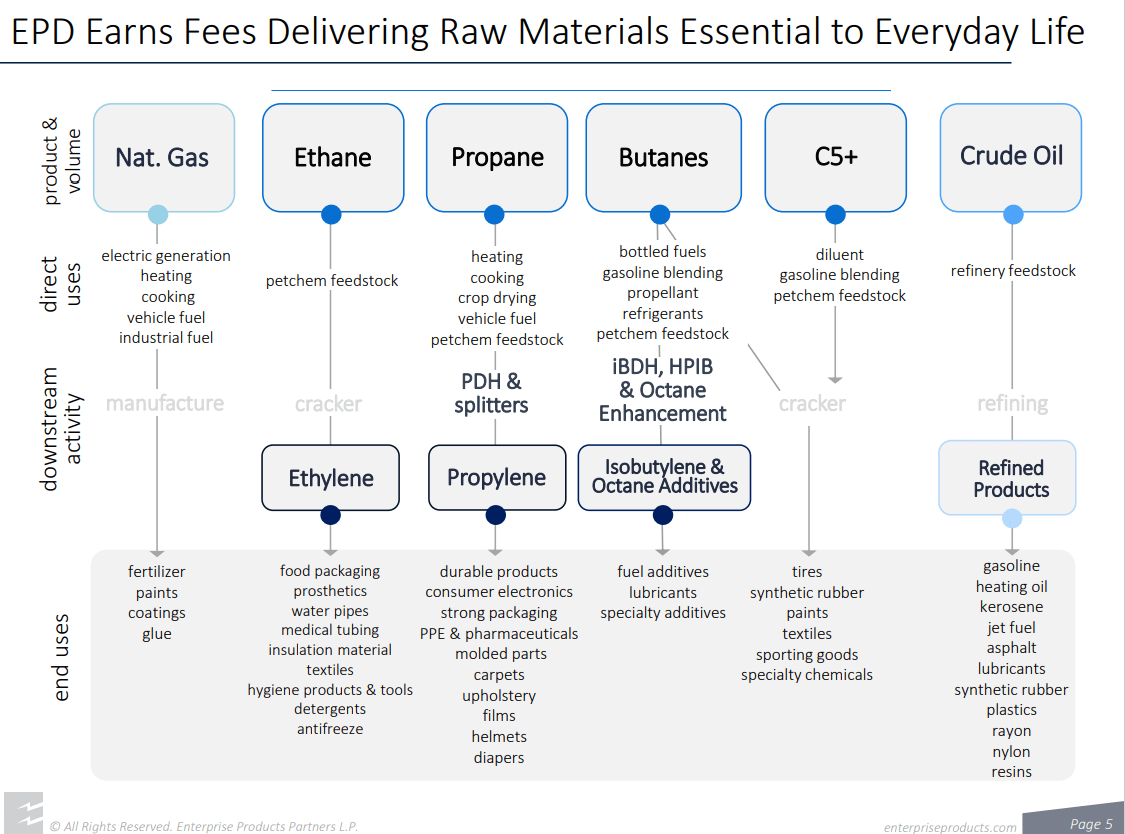

The natural gas streams containing NGLs and other impurities is useless to the LNG process until it’s been treated and processed. This becomes a profit center for EPD as the contaminated natural gas runs through EPD’s facilities and then gets transported to its final destination points, leaving behind the NGLs. This becomes a critical component for EPD as NGLs have greater economic value as a feedstock for petrochemical and motor gasoline production than as components of a natural gas stream. The primary use cases for NGLS become:

- Ethane is primarily used in the petrochemical industry as a feedstock in ethylene production. Ethylene is one of the basic building blocks for many plastics and other chemical products.

- Propane is used for heating, as an engine and industrial fuel, and as a petrochemical feedstock in ethylene and propylene production.

- Normal butane is used as a petrochemical feedstock in the production of ethylene and butadiene (a key ingredient of synthetic rubber), as a blendstock for motor gasoline, and to produce isobutane through isomerization.

- Isobutane is fractionated from mixed butane (a mixed stream of normal butane and isobutane) or produced from normal butane through the process of isomerization and is used in refinery alkylation to enhance the octane content of motor gasoline, in the production of isooctane and other octane additives, and in the production of propylene oxide.

- Natural gasoline, a mixture of pentanes and heavier hydrocarbons, is primarily used as a blendstock for motor gasoline, diluent in crude oil to aid in transportation, and as a petrochemical feedstock.

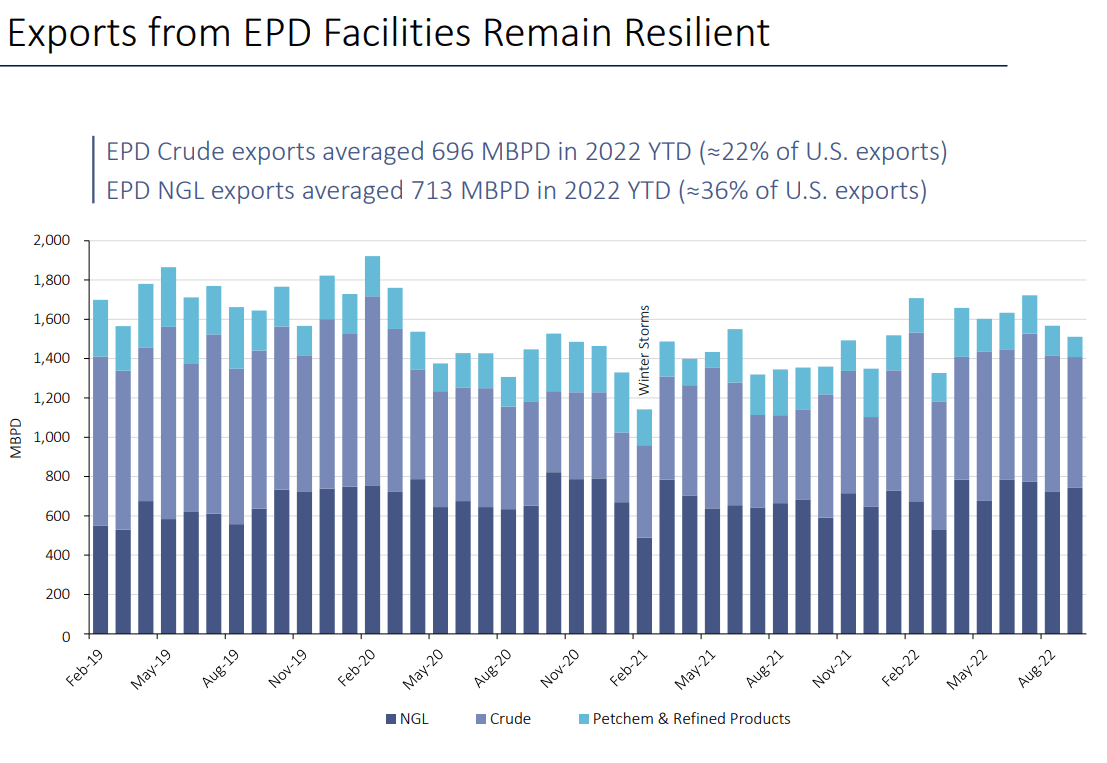

EPDs natural gas processing utilizes service contracts that are either fee-based, commodity-based, or a combination of the two. The commodity-based contracts include keeping whole, margin-band, percent-of-liquids, percent-of-proceeds, and contracts featuring a combination of commodity and fee-based terms. This means that EPD will retain all or a portion of the extracted NGLs as consideration for their processing services. EPDs marketing activities for NGLs allow them to not only sell Ethane, Propane, Butane, and Isobutane on the open market they also control 33% of U.S NGL exports. EPD will get paid twice on the same product as they will accumulate these NGLs as part of their processing contracts, then be contracted to export them globally.

Enterprise Products Partners

EPD has expanded its position in NGL exports to 36% of all U.S. exports and 22% of all crude exports from the U.S. I am becoming more and more bullish on EPD as the current energy landscape plays directly into EPDs wheelhouse. EPD’s operational growth through its major projects under construction should be well received throughout the oil & gas industry as it will add additional throughput capacity as demand for fossil fuels continues to increase. As more throughput occurs, revenues will increase, and the trend in EPD’s DCF should continue upward.

Enterprise Products Partners

Conclusion

EPD isn’t a flashy company, but its infrastructure plays a critical role throughout the U.S. economy. The barriers to entry are immense, and it’s almost impossible for new competitors to enter the space. EPDs track record is hard to replicate, its distribution has stood the test of time, and its DCF distribution ratio and trajectory indicate that future increases are inevitable. From an income investor standpoint, EPD provides a yield that has outpaced risk-free investment vehicles and is an interesting alternative to low-yielding equities for income. I think more investors focused on income will gravitate toward higher-yielding assets if they are willing to take on risk due to risk-free 4% yield options in the current landscape. There is a lot to be bullish on in regard to EPD, and I think income investors could benefit from unit appreciation in 2023 while collecting a distribution yield that exceeds 7.5%.

Be the first to comment