Sundry Photography

I upgraded my thesis on Enphase Energy, Inc. (NASDAQ:ENPH) in April, urging investors to consider its steep Q1 earnings selloff to add more positions. However, following this week’s decline (including ENPH’s post-Q2 after-hours earnings selloff of -13%), we are back to square one and possibly lower when the regular session starts later today (July 28).

ENPH investors have endured a torrid 2023 if they added at its overly-optimistic highs at the end of 2022. That proved to be an astute sell level for investors to cut exposure as it also marked the peak in Enphase’s near-term operating performance.

The company’s Q2 earnings scorecard yesterday (July 27) corroborated that the growth normalization phase in Enphase is not over, as management offered hugely disappointing guidance.

Accordingly, Enphase updated investors that it expects revenue of $575M at the midpoint of its guidance range, much lower than analysts’ estimates of $744M. Accordingly, it indicates a YoY decline of 10%, a pivotal development in Enphase’s significant growth trajectory over the past two years. In addition, the company’s gross margin profile is also expected to suffer from the near-term impact, as management guided to a GAAP gross margin of 42.5%, below analysts’ estimates of 43.2%.

Hence, the post-earnings decline should not be unexpected, given the tepid guidance. Market operators who fear worse is yet to come for Enphase and its solar peers likely took the “sell first, ask questions later” approach. However, I assessed it has also opened up the opportunity for long-term investors to consider, as ENPH is no longer overvalued.

Management upgraded its stock repurchase program to $1B after consummating its previous $500M authorization. Notably, the company exercised the remaining $200M of its previous program in Q2, as it bought back its shares at an average cost of $159.4. I also gleaned company insiders buying ENPH shares between late April and early May at a range of $157 to $167.

As such, I believe it suggests that management likely assessed that its stock is considered undervalued at these levels, lifting investors’ confidence in adding more exposure. Also, management’s decision to initiate a new authorization of $1B at its earnings release suggests that the company likely anticipated a sharp reversal in its stock price, offering opportunities to be more aggressive with its buyback. CEO Badri Kothandaraman offered his views on the company’s buyback program as he articulated:

Enphase will only buy back stock at a value below the conservatively estimated intrinsic value of the stock. The company aims to be disciplined and not overly aggressive in its buyback strategy. – Enphase FQ2’23 earnings call

The company offered a clear assessment of excess inventory in the current quarter, as inventory levels in the channel remain high. As such, the company’s decision to take a “one-time” adjustment in Q3 is expected to drive a faster normalization in the channel inventory, allowing Enphase to return to the growth phase subsequently.

Enphase bears will likely point out that the company’s premium valuation suggests that any form of weak execution/guidance will probably be scrutinized. It makes sense as growth investors worry about whether the uncertain macroeconomic conditions could worsen further, coupled with a still hawkish Fed that increased the Fed Fund rates by another 25 bps this week. Worsened by the uncertain regulatory impact of the introduction of NEM 3.0, Enphase investors are faced with several growth risk factors.

However, astute growth investors also know that the best opportunities in highly volatile stocks like ENPH are likely found when the market priced in significant pessimism, as reflected in ENPH’s price action.

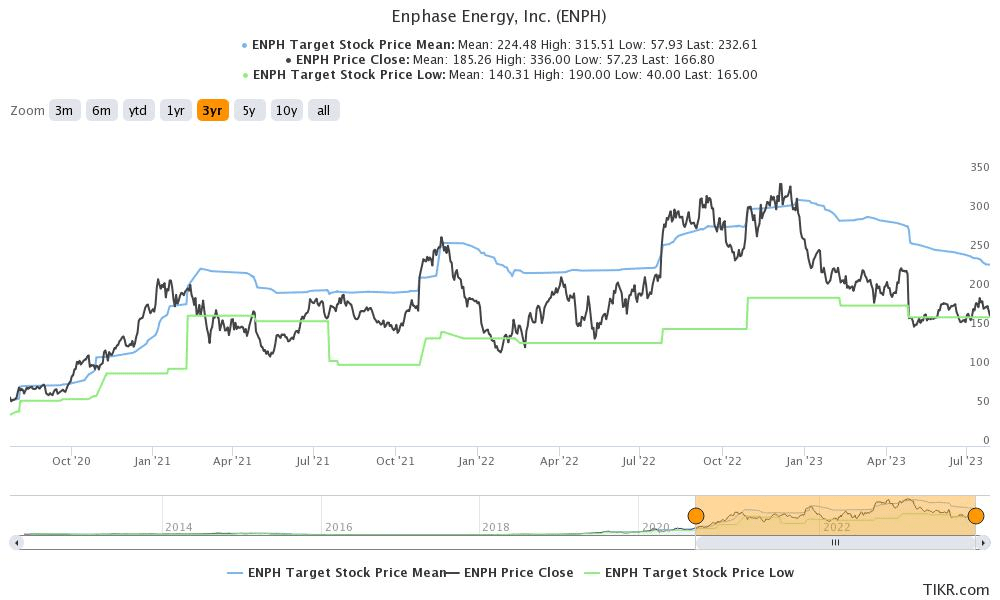

ENPH analysts’ price targets (TIKR)

Notwithstanding the steep selloff, ENPH should still be valued as a growth stock, as rated by Seeking Alpha Quant’s growth grade of “A.” Notably, ENPH is still consolidating close to the lower bound of analysts’ price targets or PTs, which also saw dip buyers returning confidently over the past three years.

However, depending solely on such a historical trend could be perilous as the market is not backward-looking. The critical question is where buyers are expected to defend the selloff as ENPH holders look to add more positions.

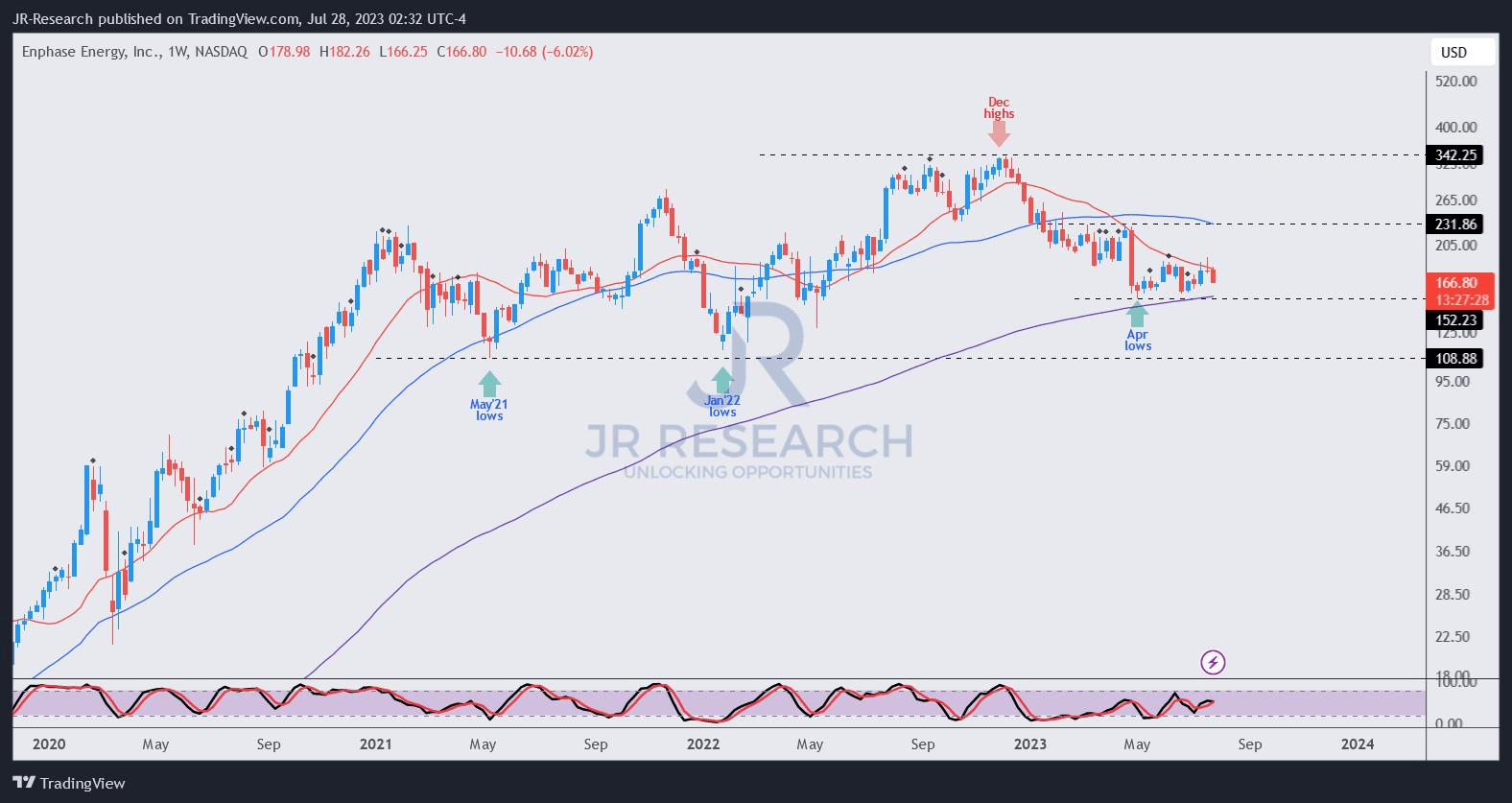

ENPH price chart (weekly) (TradingView)

ENPH has been consolidating constructively at the $150 level since the selloff after its first-quarter earnings release. Momentum buyers have not returned in force, but ENPH dip buyers didn’t give up these levels since then.

With the expected post-earnings selloff from yesterday’s release, I expect that level to be re-tested again, allowing us another opportunity to assess buying support.

That said, I assessed that buying support should remain robust, with the market likely pricing in the impact of its lowered guidance quickly. High-conviction investors expecting the normalization phase to be completed in the second half should find the sold off levels attractive.

Rating: Maintain Buy.

Important note: Investors are reminded to do their due diligence and not rely on the information provided as financial advice. Please always apply independent thinking and note that the rating is not intended to time a specific entry/exit at the point of writing unless otherwise specified.

We Want To Hear From You

Have constructive commentary to improve our thesis? Spotted a critical gap in our view? Saw something important that we didn’t? Agree or disagree? Comment below with the aim of helping everyone in the community to learn better!

Be the first to comment