putilich

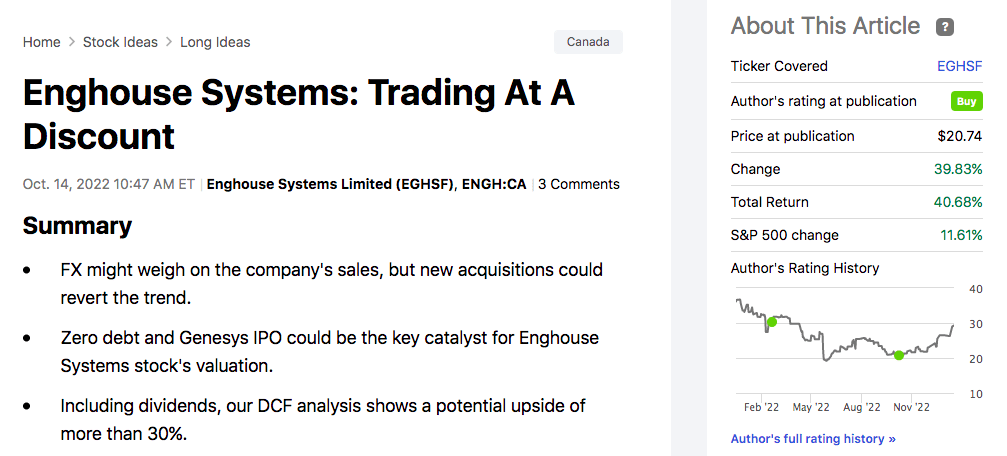

In our last publication called Enghouse Systems (OTCPK:EGHSF): Trading At A Discount, we were pretty positive about the company investment thesis. Taking into account Enghouse Systems’ dividend, we were forecasting a potential upside of more than 30%. Speaking of numbers, the company delivered a 40.68% compared to the average S&P 500 return of 11.61%.

Mare Evidence Lab’s previous publication

Last time, we emphasized how

the company’s FY 2020 was outstanding, as the COVID-19 health crisis accelerated Enghouse Systems’ top-line sales trend based on clients’ smart working and digitalization. These factors positively influenced revenue and margin; however, the company was currently not able to match Wall Street analyst expectations. Q3 results were an additional confirmation, and today we can clearly say that Q4 accounts were in line with 2022 development.

In Q4, Enghouse Systems reported a turnover and an adjusted EBITDA of $108.1 million and $35.8 million respectively. The EBITDA margin stood at 33.1% compared to the 37.2% achieved in the same period last year. On a yearly basis, top-line sales reached $427.6 million versus $467.2 million recorded last year, and EBITDA negatively followed the trend. Enghouse Systems’ revenue line was negatively influenced by lower Vidyo sales, and as reported last time, by unfavorable currency development for a total amount of approximately $16 million. Here at the Lab, we are forecasting a negative FX development in 2023 due to the dollar strength compared to the € evolution. However, going down to the P&L, the company’s yearly net income was up by 1.8% from $92.8 million to $94.5 million. This was due to lower corporate tax and non-operating expenses.

In our last analysis, we also analyzed Enghouse Systems’ M&A optionality. We commented on the latest three acquisitions, and with the Q4 numbers the company announced a new target. As a recap:

- VoicePort is a SaaS-automated solution based in New York;

- NTW Software is a company ubicated in Austria and Germany;

- Competella AB is a SaaS-provided contact center located in Sweden;

- New acquisition of Qumu Corporation to expand its SaaS video proposition. It was an all-cash transaction for a total consideration of US $18.0 million. Qumu is a leader in cloud-based enterprise video technology.

Despite the latest M&A, Enghouse Systems’ cash and cash equivalents reached $228.1 million versus the $229.5 million recorded in the Q3 results. In the press release, the company is still actively looking to pursue acquisition opportunities. To support the company’s M&A optionality, valuations are generally decreasing in the enterprise software market and Enghouse Systems believe that the reduced ability to raise capital and higher debt servicing costs will add a new phase of inorganic growth. The company commented that is “closely monitoring acquisition opportunities as valuations become more aligned with our financial and operating criteria“.

Recent M&A

Conclusion and Valuation

Despite the acquisition optionality, we now believe that Enghouse Systems’ valuation is justified on a P/E basis.

Enghouse Systems’ PE evolution

Based also on our DCF model, the company reached our target price of CAD $38.67 per share and is currently trading at CAD $39.12. Despite the fact that the company is expanding its SaaS offerings at the global level, we should price in the negative trend on sales as well as the higher WACC estimates now at 8.38%. In our numbers, we derive a 2023 EPS of $1.72, and using a 23x P/E, in line with the company’s past trading, we reached a valuation of CAD $39.25. Therefore, we decide to decrease our rating to a neutral rate.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment