Joe Raedle/Getty Images News

Energy Transfer (NYSE:ET) has had an impressive, if almost a boring year. For me as an investor, boring is great, as ET has mostly disappeared from headlines as controversial projects have been completed and put into service.

ET has finished a significant number of projects in 2022, some of which were inherited from the Enable acquisition, with only a few smaller projects ongoing into 2023.

I’m hoping for a similar year in 2023 and believe ET units will outperform the market again. Here is what I think we’ll see happen as this year progresses.

Distribution returns to $1.22/unit

Continuing on the regular cadence, I believe the distribution will return to $1.22/year, or 0.305/quarter, at the next announcement. This announcement should happen on the last Tuesday in January, if history is a guide.

ET has 3.11 billion units issued. At $1.22, this costs them $3.8 billion/year, or roughly half of their DCF.

As of Friday’s closing price of $12.15, this will put the yield of ET units over 10% with over 2x coverage.

2023 EBITDA Guidance

In February 2022, ET guided 2022 EBITDA at $11.8 – $12.2 billion. They’ve steadily increased this guidance throughout the year as volumes and commodity pricing have strengthened, arriving at a final guidance of $12.8 – $13.0 billion. At the low end, this is a billion dollar increase since the beginning of the year. The performance of this business has been outstanding, and for all the criticism ET’s management gets, they’ve built an impressive franchise.

ET has completed a number of projects this year that will have a full year of EBITDA contribution in 2023, including

- Cushing South Pipeline (In Service Q1)

- Permian Bridge Pipeline project (In Service Q1)

- Mariner East Pipeline System (In Service Q1)

- Ted Collins Link (In Service April)

- Gulf Run (In Service mid December)

Other smaller projects that should complete in 2023 will also add to EBITDA

- GreyWolf processing plant (Q1)

- Bear processing plant (Q2)

- Oasis pipeline expansion (early Q1)

- Frac VIII processing plant (Q3)

ET has guided to a 6x build multiple on their projects. Given the roughly $2 billion spend for 2022, we could see an EBITDA tailwind of $350 million from projects completed this year. There is also a $126 million legal settlement on the crude oil segment in 2022 that should not reoccur in 2023 (fingers crossed!)

So 2023 should have a ~$500 million tailwind compared to 2022. There may be additional tailwinds from inflation indexed contracts and recontracting at equal or higher rates. That’s the good news.

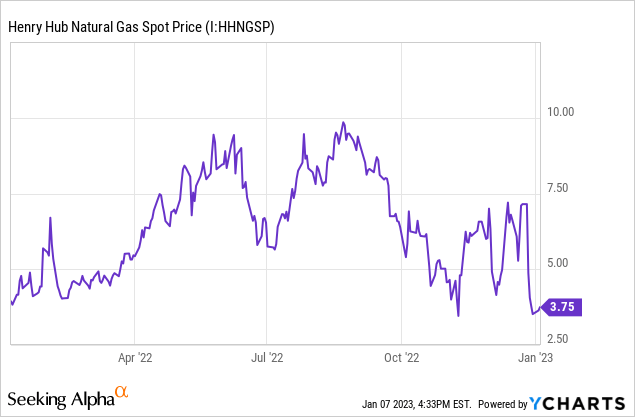

The bad news is that commodity pricing has weakened significantly in the past 6 months, which will act as a small drag on results. ET’s operating performance has been driven by both increased volumes and higher natural gas and crude pricing. Natural gas has been driven down recently primarily by a warmer winter. NGL prices, which are correlated with crude pricing, have also been weaker.

No one knows what 2023 pricing will bring, but it is off to a weak start, and as a result I believe ET management will be conservative in their forecasts. I am not expecting initial 2023 guidance to be higher than 2022 results, even with all the new projects coming online, because of how strong commodity pricing in 2022 was. I expect ET to initially guide 2023 in line with 2022, and then raise guidance throughout the year if commodity pricing strengthens, similar to what we saw this year.

Ultimately, I expect initial 2023 guidance to be near the final 2022 performance, in the $12.8-13.2 billion range, with strengthening commodity pricing providing upside as the year progresses.

CapEx spending in 2023

As recently as November 2021, ET had guided to $500-700 million in growth capital spend for 2022.

This was changed to “Legacy ET 2022E and 2023E Growth Capital: ~$500-700 million per year, expect to provide 2022 growth capital update including Enable in early 2022” in December 2021. ET will ultimately spend around $2 billion on growth capital in 2022.

The Enable acquisition added some of this. The recently completed Gulf Run pipeline was a $500 million project inherited from Enable, nearly all of which was spent in 2022. There was also $200 million in capital spend that got deferred from 2021 into 2022.

ET will provide official 2023 guidance with the Q4-22 results in February, but they’ve already given some hints in response to analyst questions. From the Q3-22 earnings call, co-CEO Tom Long said

You’ve got everything from the Lake Charles LNG to the Warrior to several other items, petchem, et cetera. So it’s really difficult probably to give you that right now.

That’s the reason we wait till the end of the fourth quarter to be able to provide that. But we’ve talked about pretty much everything that’s out there that we’re seeing. So if you really kind of go back to what guidance we give this year, the $1.8 billion to $2.1 billion, there’s not a lot of additional guidance we can give you for next year until we have a little more visibility into those. But as you can see, it’s not going to be a really large number.

There are only two major announced proposed projects discussed heading into 2023

- Lake Charles LNG liquefaction facility, with construction cost estimates anywhere from $6-10 billion.

- Warrior pipeline, a new $600 million Permian natural gas takeaway pipeline.

Lake Charles was originally to be a joint venture with Shell (SHEL), but Shell withdrew in 2020. ET has guided to reaching FID (Final Investment Decision) in Q1, but has also stated that there will be minimal capital spending in 2023 even if they move forward.

Warrior’s FID has been guided to happen in “the next couple of quarters.” With the latest crash in natural gas prices, as well as tempered expectations from growth in the Permian, I would not be surprised to see ET hold off longer on this project.

Even if both projects move forward, 2023 spending on them should be small. I believe 2023 is the year where ET ramps down growth capital spending further.

I’ll estimate we see $1 billion in growth capital from ET in 2023.

What could ET do with the excess $3-4 billion?

Even after the restoration of the distribution back to $1.22, ET will have significant excess cash flow. Absent any cash M&A, which I believe is a low, but not zero probability, there are 3 main ways ET could use its excess cash flow.

1. Continue Paying Down Debt

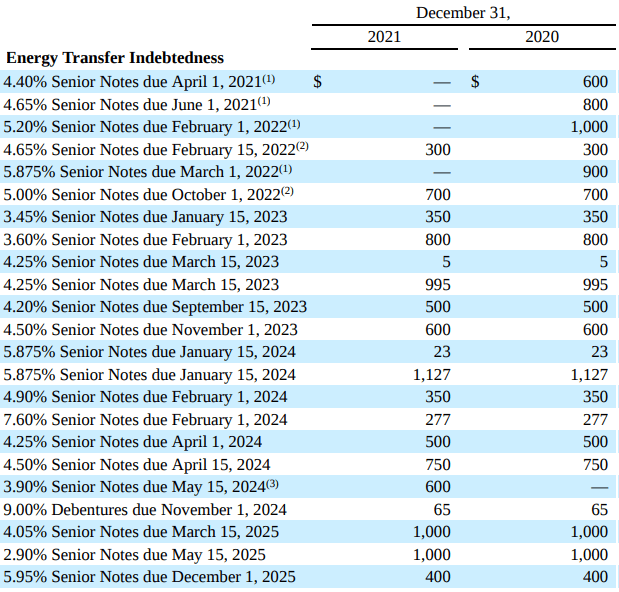

ET is fast approaching the 4.0x Debt/EBITDA target level, but there are still a significant amount of near-term maturities.

- $3.3 billion in 2023

- $3.7 billion in 2024

- $2.4 billion in 2025

Energy Transfer 2023-2025 Debt Schedule (Energy Transfer 2021 10-K)

ET was recently able to price $1 billion in 5 year notes at 5.5% and $1.5 billion of 10 year notes at 5.75%. I believe that receiving pricing this favorable, along with approaching their stated targets, is going to shift ET management towards more accreditive uses of its cash flow. From here out, I believe ET will look to refinance, rather than pay off, most of its maturing debt.

2. Call Preferred Units

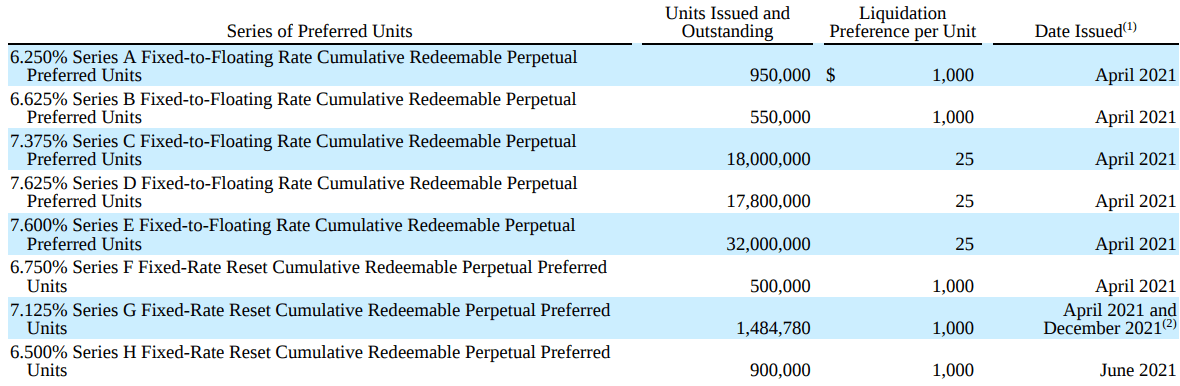

ET has $6.1 billion of preferred shares outstanding, the majority of which were issued in 2021 to focus on debt repayment, as the credit rating agencies view preferred shares as half equity, half debt. When these were issued, short term rates were near zero.

Few people thought we’d see short term interest rates in the 5% range in 2023, and ET management likely planned on these resetting down. But here we are, and as rates for the Series C-E start resetting over 2023 and 2024, they will reset significantly higher.

Energy Transfer Preferred Shares (Energy Transfer 2021 10-K)

Of the publicly traded units

- ET-C (NYSE:ET.PC) will reset to LIBOR+4.53% on 5/15/23

- ET-D (NYSE:ET.PD) will reset to LIBOR+4.74% on 8/15/23

- ET-E (NYSE:ET.PE) will reset to LIBOR+5.16% on 5/15/24

The current 6 month LIBOR sits at 5.15%, so these preferred units will all reset into the 10% range. When they reset, ET gains the option to redeem them at par. I think there’s a very good chance that they will.

3. Repurchase Common Units

With common units trading at a DCF yield of over 20%, repurchasing common units at this level is extremely accreditive. 2022 was the first year ET really started discussing repurchasing common units within their capital allocation framework during conference calls, but have remained non committal to any definite timelines or dollar amounts.

My Prediction: ET uses the excess cash flow primarily to repurchase preferred shares in 2023. It removes an expensive form of funding, and is still a credit positive in the ratings agencies view.

That said, I would be pleasantly surprised if we got a mix of preferred and common unit repurchases.

Conclusion and Recommendations

Energy Transfer enters 2023 as a transformed company. Concerns over debt levels, high risk projects, recontracting rates, poor ROIC, and various governance issues are slowly fading away.

The reasoning as to why one of the most diversified and best performing midstream companies should trade at a significant discount to peers is becoming weaker by the day.

2022 was the year the market began to notice, but we’re still not near what I consider to be a fair valuation for ET considering the stability of its cash flows and the replacement value of its assets, both from a physical construction cost standpoint as well as a political/project risk in trying to build some of their assets today.

| Energy Transfer |

2019 |

2022 |

|

Net Income / Unit |

$1.80 |

$1.90 |

|

DCF / Unit |

$2.32 |

$2.57 |

| EBITDA / Unit | $3.91 |

$4.00 |

|

Growth Capital Expenditures |

$4B |

$2B |

|

Unit Price1/3/2020 vs. 1/3/2023 |

$13.68 |

$11.56 |

Despite enduring an unimaginable black swan event in COVID, Energy Transfer has already eclipsed its 2019 performance on a true apples-to-apples basis (I break these numbers down per unit, as there are 15% more units now due to the SemGroup and Enable acquisitions.)

Energy Transfer has a distribution almost restored back to its pre-pandemic levels and the most free cash flow in its history. I think ET is an unimaginable value near $12/unit, and don’t believe it will stay near these levels for much longer.

Be the first to comment