tum3123

As we head further into 2023, our Franklin Templeton Emerging Markets Equity Team finds many reasons to be constructive about emerging markets.

Three things we’re thinking about today

We are optimistic that emerging markets, in particular Chinese equities, can post positive returns in 2023. Drivers of our optimism include:

1͏. China dismantles its zero-COVID policies: The removal of almost all COVID-19 restrictions in China is resulting in a wave of infections, with up to 80% of people in urban areas contracting the virus. As the wave subsides, economic activity is expected to normalize. Durable goods and financial services are likely beneficiaries of a resumption in normal patterns of human interaction and trade. A recovery in outward-bound tourism is expected to benefit economies in Asia, which prior to 2020 were the prime beneficiaries of a large number of Chinese tourists.

2. Peak in US interest rates: Consensus expectations1 point to two further increases in the US federal funds rate in 2023. While the timing of eventual rate cuts remains uncertain, the peak in rate hikes is the first step on this journey. The US dollar has already reacted to expectations of a peak in interest rates in 2023, trending lower in recent months. US dollar weakness should benefit emerging market fund flows, reversing the outflows of recent years, which in turn is supportive of emerging market equities.

3. Acceleration in renewable energy investments: The “new normal” of elevated fossil fuel prices is likely to incentivize emerging markets to accelerate decarbonization efforts in order to reduce energy costs and meet their Paris Climate accord targets. This will create potential opportunities for emerging market investors. The battery industry – for both electric vehicles and battery electric storage systems – as well as the solar industry, stands out. China and South Korea are at the forefront of new battery technologies, commanding 83% global market share between January-October 2022.2 India is also investing heavily in the solar industry as it seeks to become self-sufficient in photovoltaic panel production.

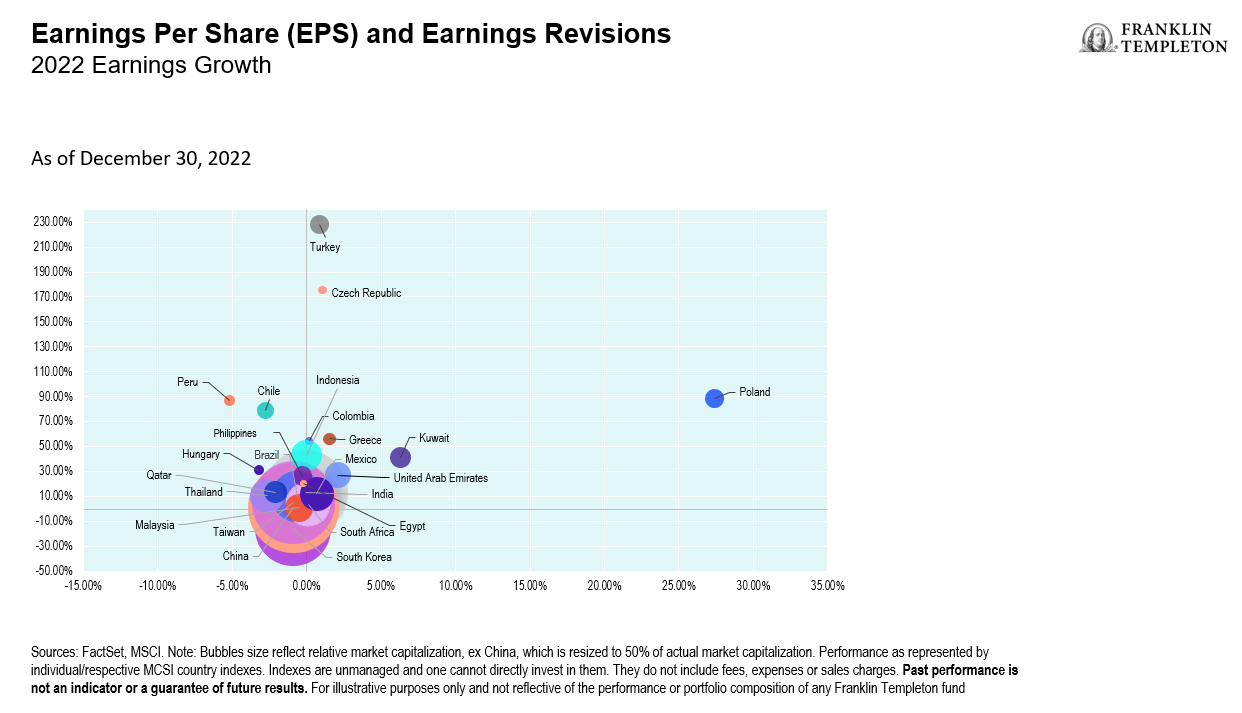

Outlook

As we head further into 2023, we find many reasons to be constructive about emerging markets (EMs). Markets such as Chile and Indonesia have started to pause interest-rate hikes or scale back the magnitude of their rate hikes. We expect a policy pivot to revive consumption and spur economic growth as inflation slows. In addition, after a slowdown in earnings in 2022, there is a prospect for a recovery in earnings growth in 2023. We view China as a leader with a near-15% estimated growth, based on consensus expectations.3 However, we are of the view that earnings may continue to still be relatively weaker in China in the near term, with a recovery timed toward the end of 2023 instead. Nonetheless, a pickup in earnings revisions in EMs would signify better times ahead for earnings and in turn, equities.

Although a weakening global outlook appears to be on the horizon, economies with a greater focus on domestic demand are better placed to weather a challenging environment. These markets include EM countries such as India, Brazil, and Indonesia.

India has attracted investors looking to diversify their manufacturing bases from China. Similarly, the Middle East is experiencing an upturn in consumption, due to a spillover from high energy prices.

China’s recent policy changes and low equity valuations have created opportunities locally as well as in Asia more broadly, as China is the largest driver of economic activity in the region. China’s reopening could benefit EMs outside of Asia as well. As mobility in China bounces back to pre-pandemic levels, its demand for oil will also likely increase. This benefits several non-Asian EMs which supply crude oil to China, including Saudi Arabia, Kuwait, and Colombia. While the risks of 2022 have abated slightly, we remain watchful for developments that could change our overall EM outlook, including China’s relationship with Taiwan and the United States.

As the investment environment evolves, an important feature that we seek in EMs is resilience, in terms of both economies and companies. A particular area of focus for us is the sustainability of corporate earnings, whether in the face of COVID-19, policy changes, technology disruption, or other challenges. We see companies with structural growth drivers aligned with digitalization, decarbonization, and premiumization emerging as long-term winners.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Special risks are associated with investing in foreign securities, including risks associated with political and economic developments, trading practices, availability of information, limited markets and currency exchange rate fluctuations and policies; investments in emerging markets involve heightened risks related to the same factors. Investments in fast-growing industries like the technology and health care sectors (which have historically been volatile) could result in increased price fluctuation, especially over the short term, due to the rapid pace of product change and development and changes in government regulation of companies emphasizing scientific or technological advancement or regulatory approval for new drugs and medical instruments. China may be subject to considerable degrees of economic, political and social instability. Investments in securities of Chinese issuers involve risks that are specific to China, including certain legal, regulatory, political and economic risks.

1 Source: Bloomberg, January 5, 2023.

2 Source: SNE Research.

3 Source: Bloomberg, January 5, 2023.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment