Scott Olson

Billionaire SpaceX, Tesla (TSLA) ,and Twitter (TWTR) CEO Elon Musk recently predicted that “stormy times” are likely in store for the next 18 months or so:

It does seem like we’re headed into a recession here in 2023…My best guess is that we have stormy times for a year to a year and a half, and then dawn breaks roughly in Q2 2024

He went on to mention that – while he does not yet know how severe the downturn will be – he thinks it could very possibly be as severe as the downturn that followed the Great Financial Crisis in 2009. As a result, he encouraged investors to take a very conservative approach to investing, including hoarding cash, stating:

From a cash standpoint, keep powder dry.

For those that do continue to dip their toes in the stock market, he strongly cautioned against the use of margin debt:

I really advise people to not have margin debt in a volatile stock market. If there’s mass panic in the stock market, then you’ve got to really be careful about margin debt.

In this article, we will share our thoughts on Musk’s comments, our approach to the current environment, and some of our top picks to outperform the market in 2023.

Our Thoughts On Musk’s Advice

In our recent Market Outlook report, we came to a similar best guess as Mr. Musk as to what is likely to transpire in the coming 1-2 years: recession.

However, unlike Mr. Musk, we are not market timers. We subscribe to the view that time in the market (SPY) matters far more than timing the market. For those with low risk tolerance and/or who lack the stomach to handle volatility, it certainly could make sense to build up a large stockpile of dry powder right now. Furthermore, for those who have major expenses coming up in the near future, we certainly think it is prudent to hold that purchasing power in cash rather than gambling with it in the stock market.

That said, for the rest of us who have a long-term time horizon with our invested capital and who can psychologically withstand the volatility of the stock market, we think it is always prudent to remain fully invested in the market. As Berkshire Hathaway’s (BRK.A)(BRK.B) Warren Buffett said:

if you don’t feel comfortable owning a stock for 10 years, you shouldn’t own it for 10 minutes

and

Games are won by players who focus on the field, not the ones looking at the scoreboard.

Finally, we strongly agree with Mr. Musk’s stance on use of margin to buy stocks. Here Mr. Buffett once again offers us some sage advice, stating in his 2019 letter to shareholders:

[When it comes to margin debt,] even if your borrowings are small and your positions aren’t immediately threatened by the plunging market, your mind may well become rattled by scary headlines and breathless commentary. And an unsettled mind will not make good decisions… There is simply no telling how far stocks can fall in a short period…The light at any time can go from green to red without pausing at yellow

If you take on a lot of margin debt, a stock market crash will have an outsized impact on your portfolio’s market value. This in turn – at a minimum – may scare you into selling at or near the bottom (the worst possible time to sell stocks). Even more destructive is the risk that you may be forced to sell at or near the bottom due to a margin call. This locks in losses and permanent destruction of the intrinsic value of your net worth.

If instead you are able to hold through the crashes, you preserve the long-term compounding power of your investment and – as long as you hold quality investments purchased on a value basis – your wealth will almost certainly continue to compound over the long-term at an attractive rate. Leverage may look like a free lunch during a bull market, but it can deal your long-term wealth building process a fatal blow during a bear market.

Our Approach And Top Picks

Given our bearish outlook for the economy, we are placing a stronger emphasis on balance sheet strength and underlying business quality as we believe that if the downturn gets serious enough, those businesses with sound balance sheets and sufficient business strength will emerge in better shape whereas many of their overleveraged and weaker positioned competitors may suffer permanent impairment or not even survive the downturn.

On top of that, we view holding companies with strong balance sheets as a more attractive way of holding cash in our portfolio because the businesses themselves have substantial liquidity which they use to buy low on dips instead of we ourselves. Why is this preferable to holding cash ourselves? Well, for one their cost of capital is generally much lower than ours and having a stronger balance sheet generally insulates them better against market crashes than companies that do not have strong balance sheets. It also means that they earn better returns on the leverage they do apply to their equity since stronger credit ratings often result in lower interest rates on corporate debt.

Some defensively positioned stocks with strong balance sheets that we particularly like in the current environment include:

- Enterprise Products Partners (EPD) which has a rock solid balance sheet with an industry-best BBB+ credit rating and a 3.1x leverage ratio that is among the lowest in the industry and well-below their already conservative long-term target range of between 3.25x and 3.75x. It also has substantial liquidity ($3.3 billion) and an incredibly long weighted average term to maturity on its debt of 20 years. Thanks to a primarily fee-based, commodity price resistant business model, it generates stable cash flows and high returns on invested capital in pretty much all economic environments and its 1.8x distribution coverage ratio makes its 7.9% current yield look very safe even if a deep recession were to hit. EPD is also close to becoming an Aristocrat with 24 consecutive years of distribution per unit growth.

- ATCO Ltd. (OTCPK:ACLLF) is an A- rated regulated utility business that also owns some faster-growing ancillary infrastructure businesses like structures and logistics, renewable power production, and ports. The company has been extremely consistent at growing its dividend per share, with a track record of 29 years of consecutive dividend growth. With a very strong balance sheet, a recession resistant business model, and a well-covered 4.3% dividend yield that should continue growing for many years to come, ACLLF is a great place to take shelter while a recession rages without giving up exposure to current income and growth.

- W. P. Carey (WPC) is a BBB rated triple net lease REIT that generates the majority of its rent from industrial and warehouse real estate along with high quality retail, personal storage, and office assets. It has raised its dividend every year for about two and a half decades now and enjoys a recession resistant business model that is also inflation resistant given its low CapEx and significant exposure to CPI-linked leases. With a near 5.5% current dividend yield that is safely covered by cash flows, WPC looks like a very safe income bet that should outperform during a recessionary period.

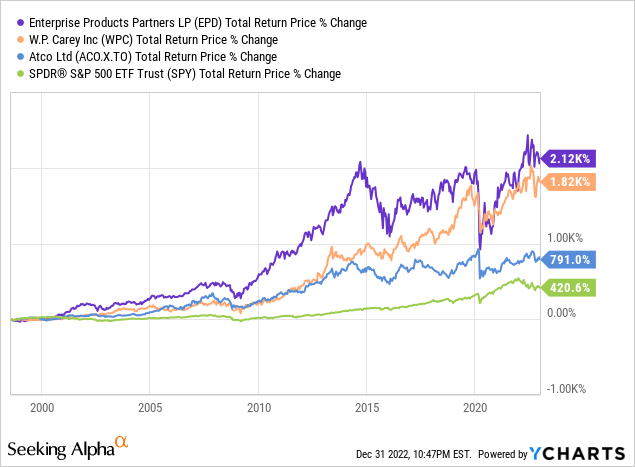

Something else to like about all three of these picks is the fact that they have outperformed SPY over the long-term, reflecting their superior management and business models:

Investor Takeaway

As a new year dawns, these are challenging if not terrifying times for investors. When leading businessmen and thought leaders like Elon Musk are telling investors to build up a cash position and that stormy times are ahead and likely to stick with us for a while, investors would be prudent to take notice.

At High Yield Investor we are diligently researching the best high yield opportunities to ride out a recession with and after interviewing these three companies (which you can read EPD’s here, ACLLF’s here, and WPC’s here), we have strong conviction in their ability to not only survive, but thrive during difficult economic times. As a result, they serve as cornerstones of our Retirement Portfolio alongside some other high yield lower risk picks:

Retirement Portfolio , HYI

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment