Sean Pavone/iStock via Getty Images

Elme Communities (NYSE:ELME) is a multifamily real estate investment trust (“REIT”) with an interest in properties located in the Washington metro and the Sunbelt region of the United States. In Q3 of fiscal 2022, the company rebranded to their current name from Washington Real Estate Investment Trust.

This rebranding was intended to mark their strategic shift away from commercial properties to pure-play residential. This was achieved through the disposition of their office and retail portfolios, the proceeds of which were then recycled into newly acquired apartment communities.

At present, the company has an interest in 27 communities containing approximately 8,900 total homes. These properties are primarily value-oriented at mid-market price points in both urban and suburban environments. Currently, in-place rents on these properties are more than 6% below market prices, a historical high for the company.

Favorable market tailwinds in the multifamily sector have begun to provide accretive benefits to ELME, though there are signs they are late to the party. While rents are still increasing, growth rates have exhibited notable moderation.

In addition, the company expects a pause on additional acquisitions through the remainder of the year and into 2023. This is likely due to broader market uncertainty and price discovery challenges. And at current trading multiples, the upside potential appears to be limited. Though the stock has made significant headway in their transformation, the benefits are unlikely to produce market-beating returns.

Recent Performance

In the third quarter ended September 30, 2022, ELME posted solid operating metrics in both their same and non-same store portfolios.

In same stores, they logged effective blended lease rate growth of 10.3%, with equal strength in signings of both new and renewal leases. While the growth rate is 90 basis points (“bps”) lower than Q2’s 11.2% growth rate, it is elevated in relation to quarters prior to Q2.

After quarter end, however, effective rent growth slowed further to 7.1%. And this represents a noteworthy comedown from the growth rates achieved over the past year.

Their non-same store portfolio held up slightly better during the quarter, with effective blended rent growth of 16.3%. But this moderated significantly following quarter end to 9.7%.

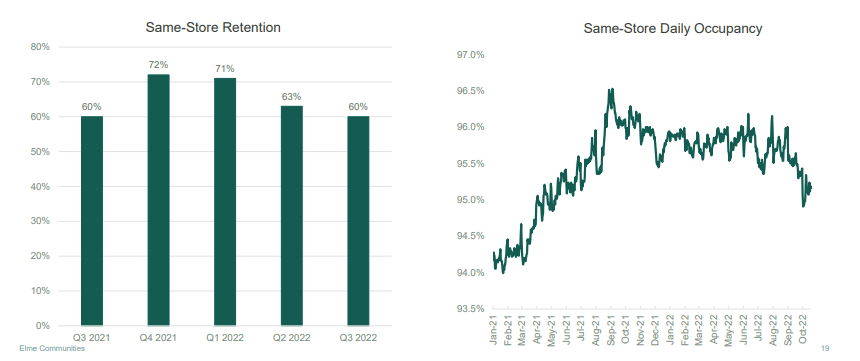

Though the pace of rental rate growth has slowed, ELME is still benefitting from high retention rates and occupancy levels. At 60%, retention was unchanged from the prior year and above historical averages, albeit down from the levels experienced at the end of 2021 and the first quarter of 2022.

November 2022 Investor Presentation – Graphical Display Of Same-Store Retention And Occupancy Trends

Higher rents and lower concessions contributed to 10.4% YOY growth in same-store net operating income (“NOI”). Growth, however, was offset by slightly lower occupancy levels. And while occupancy declined 20bps during the quarter from prior year levels, it’s worth noting that it recovered back up to 95.7% by the end of October.

Looking ahead to the remainder of 2022 and to the full-year outlook in 2023, management maintained their midpoint for core funds from operations (“FFO”) for the remaining months of 2022 but did tighten the range. And in 2023, same-store NOI is expected to build on 2022’s strength, with 10% targeted growth at the midpoint.

Liquidity And Debt Profile

ELME is well capitalized to meet their reoccurring cash requirements, which includes their debt servicing obligations and dividend payouts.

At the end of the quarter, the company had available liquidity of more than +$650M in the form of cash and availability on their revolving credit facility. In addition, they are on pace to generate nearly +$70M in operating cash flow for the full 2022 fiscal year.

Through nine months of the year, they have expended over +$200M in net real estate acquisitions. While this has tied up available cash flows, they still have the ability to acquire another +$125M in assets without exceeding their targeted leverage range.

Despite the capacity for further growth, ELME is currently guiding for no acquisitions in 2023. Their total debt load, therefore, is likely to remain low in the new fiscal year. At present, total debt represented just 26% of their total capitalization.

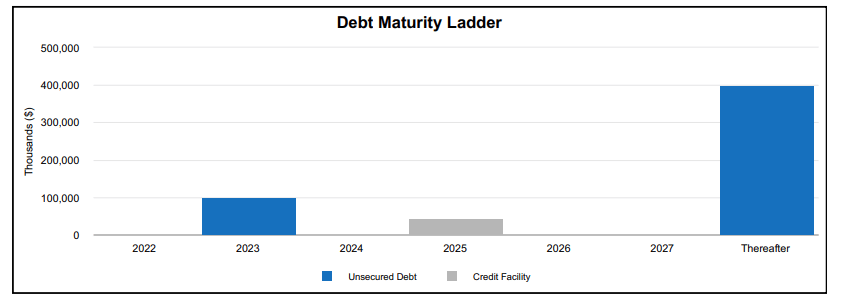

In addition, their debt load was fully unencumbered at period end, with no maturities until July 2023. In fact, prior to 2027, the company has just +$143M maturing. This represents just a fraction of their current available funds.

Q3FY22 Investor Supplement – Debt Maturity Schedule

Adequate coverage of their fixed charges that has remained consistent with prior periods, in addition to ample cushion on their required covenants further provides confidence of the company’s ability to meet their reoccurring obligations.

Dividend Safety

ELME currently provides a quarterly payout of $0.17/share. This is 43% lower than what they were paying in the first half of 2021. The cut was due not necessarily to their inability to continue covering the payout but instead to preserve capital necessary for their significant transformation into a pure-play multifamily REIT.

Given their current liquidity position and the limited amount of transactions expected in 2023, it’s unlikely the payout will experience any further cuts in the near-medium term.

In its current form, the payout represents about 80% of their core FFO through nine reported months in 2022. Moreover, the payout ratio has declined sequentially to 74% from Q2, where it stood at 81%. Compared to sector averages, coverage is on par with the sector.

Q3FY22 Investor Supplement – Dividend Payout Summary By Quarter

At a current annualized yield of 3.7%, the dividend doesn’t offer much draw to income-focused investors. And at the current run-rate in core FFO, there is not enough room to return the quarterly payout to its previous $0.30/share level, which would provide an annualized yield of over 6%.

Over time, the dynamics may begin to change as the company realizes the accretive benefits of their transition into the multifamily sector. But for now, the payout is likely to remain fixed at current values.

Main Takeaways

The rebranding to Elme Communities from Washington Real Estate Investment Trust marked the culmination of ELME’s multifamily portfolio transformation and geographic expansion into the critical Sunbelt region of the country.

The strategic shift away from the commercial sector to the residential sector via the dispositions of their office and retail portfolios was timely in a sense, especially considering the current state of offices. In addition, the sales enabled the company to deleverage their balance sheet, while also improving their current liquidity position.

But at the same time, one can reasonably question whether the shift came too late in the cycle. While rents are up, there has been a marked moderation from peak growth rates logged earlier in the year. In addition, the market environment has become more uncertain, which is perhaps one reason why the company expects to hold back on additional acquisitions in 2023.

And at 20x forward FFO, shares aren’t exactly a bargain. Similar sized peers, such as NexPoint Residential (NXRT) and Centerspace (CSR), by contrast, trade at about a 14x multiple. In addition, their current dividend payout doesn’t offer much appeal to income-focused investors, and there appears to be limited upside for further payout growth, at least until the company begins to realize the synergies of their transformation.

For prospective investors, ELME is just one of many competitors in the multifamily arena and one that is unlikely to provide meaningful shareholder rewards.

Be the first to comment