ArLawKa AungTun

The Investment Thesis

Elevance Health Inc. (NYSE:ELV) is one of the largest health benefits companies in the United States. They have grown their business at a rapid pace in the last several years and continue taking more market share of the large total addressable market (“TAM”). With a large customer base, they serve consumers, families, and many communities. They help out with the entire process around health care, and help with finding resources and support.

Right now, Elevance Health is trading at a discount to my valuations. I, therefore, think it is at a good entry price. In the long term, I have strong conviction that Elevance Health will be a good buy.

Last Earnings Report Highlights

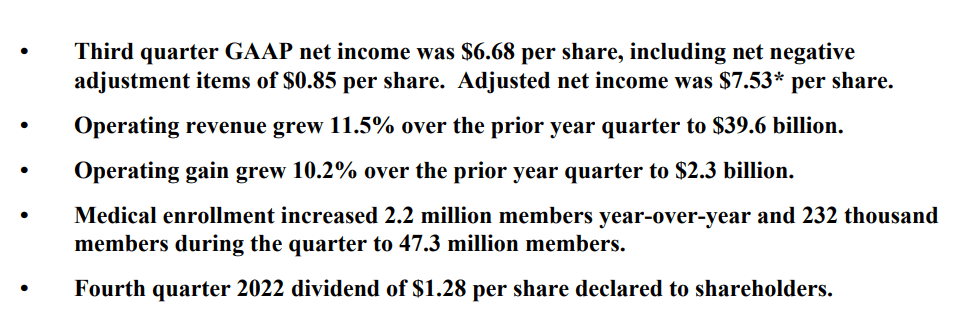

In the latest earnings report, Elevance Health provided another stellar performance for the quarter. Revenues came in at $39.6 billion, which represents an 11.5% increase YoY. The company noted that the increase was driven by a higher premium revenue as memberships in Medicaid and utilization among prescription drugs increased, among other revenue streams.

Earnings Highlights (Q3 Earnings Report)

Cash flow remained incredibly strong during the latest quarter, landing at $4.9 billion. That is an impressive increase of $2.4 billion from last year’s same quarter.

Apart from strong revenue growth and great cash flow, the company managed to return a lot of value to investors by both buying back shares and distributing a dividend. During the quarter, 1.2 million shares were purchased, while Elevance Health Inc. paid out a dividend of $1.28 per share.

The management has remained optimistic about the future. The CEO, Gail K. Boudreaux, said during the Q3 earnings call:

“Broad based momentum across Elevance Health continued in the third quarter, driven by the focused execution of our strategy and the dedication of our over 100.000 associates.”

Sector Outlook

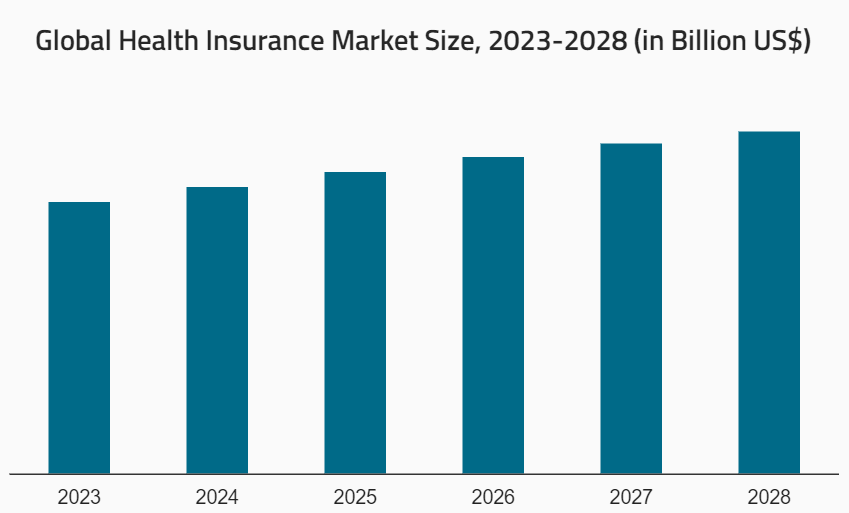

The global health insurance market has a bright future ahead of it. In 2022, the market reached $1.714 billion. By 2028, it is estimated that the market will reach $2.599 billion, which would be an annual growth of 7.11%. As Elevance is one of the leading companies in the American market, I see no reason they will be able to follow this growth in terms of top and bottom line growth.

Insurance Market Outlook (imarcgroup.com)

As insurance is a vital part of people’s life, there will always be customers willing to pay. This means Elevance is able to pass on some costs to customers and keep good margins. As ELV offers premium insurance, they will most likely be able to maintain their customer base, as they are a leading provider of this service.

Competition

The health insurance space has several different companies competing against each other. There are many different niches and sizes of these companies, but in my opinion there are some notable competitors like Cigna Corporation (CI) and Humana (HUM) posing a risk.

What Elevance needs to focus on is maintaining their customer base whilst also continuously offering a superior product to their competitors. So far, they are still seeing more and more members joining, and the total has now reached 47.3 million. This represents a market share of about 14% in the United States. In my opinion, Elevance Health has the opportunity to take more market share and increase their presence and become an industry leader. Leveraging their premium insurance services whilst also offering a superior and more cost effective product will be the edge.

The Balance Sheet

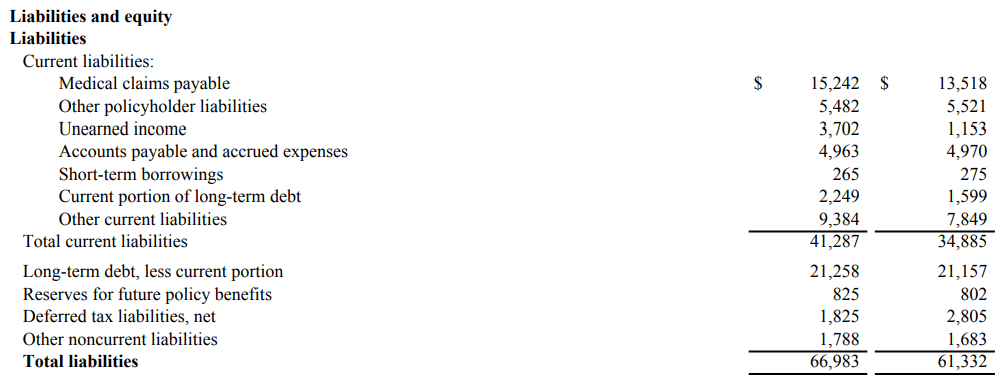

Looking at the balance sheet, Elevance Health has made some very impressive steps towards having a better financial base to stand on. The cash position has increased 81% YoY, ending up at over $8.8 billion. Looking at the debt the company holds right now, they have a current portion of $2.2 billion. I have confidence that they can manage to pay this down. I also think the long-term debt of $21 billion won’t be a problem, as they have TTM cash flow of over $10 billion. This is a very good position to be in as we are heading into a recession, and the economic environment will become increasingly more difficult.

Balance Sheet (Q3 Earnings Report)

Right now, the liabilities are growing faster than the assets are, driven by current debt increasing and also unearned income. But I am not worried about this shaking up the company too much.

Balance Sheet (Q3 Earnings Report)

Moving over to the cash flow the company has, they have steadily been increasing it over the last several years. In the latest quarter, they managed to achieve $4.9 billion, which puts any risk of share dilution to rest. The management is prioritizing giving back to shareholders by either buying back shares or dividends. Looking ahead, I think investors will continue paying a lot of attention to how the cash flow is increasing, as it will directly reflect the potential return to investors.

Outstanding Shares (SeekingAlpha)

The shares outstanding has been steadily declining at an average of 1.63% each year since 2017. I think this trend will keep up and further boosts each shareholder’s piece of the company. All in all, I think that Elevance Health is in a very strong financial position to weather any storms ahead. With a loyal membership base, revenues will continue coming in and cash flows will remain strong. As an investor, I think there are many years ahead of growth.

Valuing The Company

Elevance Health has an incredibly strong balance sheet and is a part of a growing industry. Health insurance will always be a priority for people to have, and with the strong brand recognition and loyal membership base that Elevance has, I think the future is very bright.

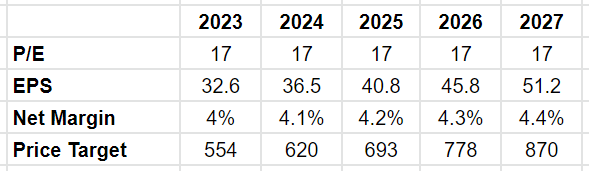

Future Estimates (Author’s Own Valuations)

Right now, Elevance Health is trading below my estimates, and also by quite a lot. In my valuation, I don’t have the dividends included or any share buybacks. On average, the company has bought back more than 1% of shares each year, which would further boost the long-term returns of an investment.

I believe an AP/e of 17 is fair to have for a company like this. Growth isn’t expected to plateau, and with a magnificent balance sheet a higher valuation is deserved. This is even slightly below the sector average of 19.

In the future, I think it will be important to see how many members the company is able to take on, and the retention rate of them, too. A focus will always be on taking more and more market share, but I don’t expect extreme growth from Elevance Health Inc., as the market is already dominated by some very large companies.

All this leads me to having a buy rating for the company right now. I think having exposure to the insurance industry – and especially with such a strong company as Elevance Health – is a great option.

Conclusion

Elevance Health Inc. is a massive insurance company, with over 47 million members, but they haven’t slowed down their growth. The industry is poised to continue growing, as insurance is something people won’t give up on as macroeconomic challenges start to mount.

The balance sheet is incredibly strong, and any danger of debt isn’t there. They also have around $10 billion in TTM free cash flow, which the management has made clear will go towards providing investors with value in the shape of share buybacks or dividends.

At the current price, I think that Elevance Health Inc. has a great risk/rewards ratio. Buying now would be at a good entry point, and Elevance Health could be a great addition to most portfolios.

Be the first to comment