Murdock48/iStock via Getty Images

I wrote about Electrovaya (OTCQB:EFLVF) in May, describing them as a risk worth taking; following the article, the share price increased by 80%, making the investment one of my best in 2022.

Electrovaya has come a long way in the last nine months, and they are now my top pick for 2023.

Electrovaya manufactures lithium batteries for forklift trucks, and this is a large industry that is transitioning from lead acid batteries to Lithium. Raymond Toyota, the world’s leading producer of forklift trucks, signed an exclusivity deal with EFL (MDA 2022 page 6 para 2, link below) that has transformed the company’s prospects. Raymond Toyota published a white paper explaining the many advantages of the EFL battery system. They include improved safety, lower cost of ownership, faster charging times, and longer between charges.

RaymondCorp_LithiumIon_Batteries_Whitepaper_1202022.pdf

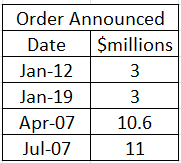

During 2022 Electrovaya repeatedly announced large-scale orders. Total revenue for 2021 was only $11 million.

Major orders 2022 (Electrovaya MDA Q4 2022)

I said in my first article, “if a company has sales, then everything else can be fixed”; in EFL’s case, it is the balance sheet that needs fixing. The company has been in a negative equity situation for some time, has had great difficulty raising finance, and has had to pay extraordinarily high-interest rates as it is judged as being of high risk. The CEO had to sign personal guarantees on several occasions to the company’s lenders for bridging loans. I presented a timeline of the debt in my previous article.

However, with sales revenue, this high-risk status is falling. On November 9th EFL sold over 17 million shares at $0.85 (Canadian), raising C$14.8 million (MDA Q4 2022 P9 subsequent events para 2). Its primary lender increased the revolving credit facility from $11 million to $16 million and reduced the interest rate payable by 1%. EFL has used the proceeds of the stock issue to pay off the high-interest (over 20% in some cases) short-term loans and end the personal guarantees from the CEO (2022 financial statement note 10 b, P26). The balance sheet is not perfect, but it is much better than it was when I last wrote, and if the sales continue as forecasted, things are about to get much better.

For a more detailed explanation of what Electrovaya does and to read a copy of the Raymond White paper, please see my first article, as this one will concentrate on what has happened since and what I forecast will happen over the next five years.

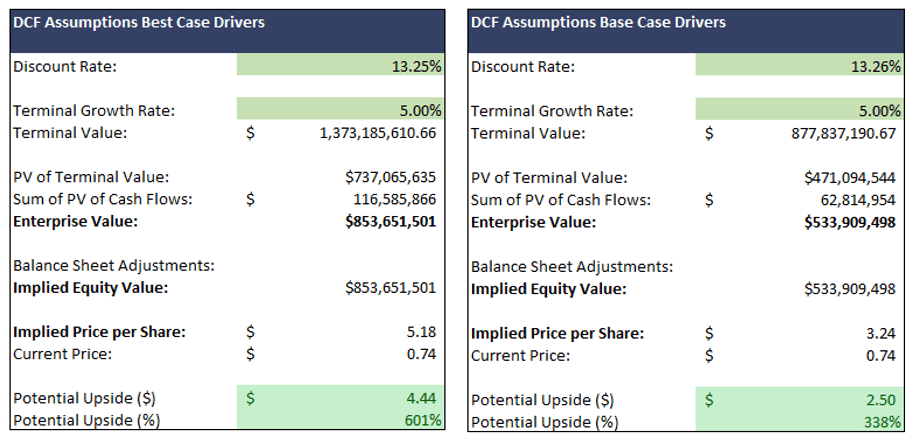

My trading plan is based on competitive analysis of disruptive technology, trying to choose which companies are likely to be successful and then following their progress. When I have enough information, I start to build a company’s financial model. I chose EFL as a likely winner amongst the new battery companies mainly because of the Raymond Toyota agreement, and I have now developed the first draft of the financial model. It suggests that the majority of the rise in share price is still to come.

Model Outputs

The final output for the model is shown below. The remainder of the article will explain how I got to the figures.

EFL Valuation (Author Model)

All figures above are in US Dollars for the share price.

The remainder is in ‘000s of US Dollars and historical figures are provided by Wisesheet. The model is designed and built by the Author.

Modeling the Future for EFL

I have used three scenarios, Best, Base, and Worst case.

All Drivers and assumptions for the model can be viewed in this file.

3-Statement_Model__EFL_Dec_22_V1__Inputs.xlsx

The other two key files are the 2022 Management discussion and the Annual Financial Statement.

EFL produces comprehensive documents each quarter, and each one includes previous information. I will reference the page and document for all key facts presented below.

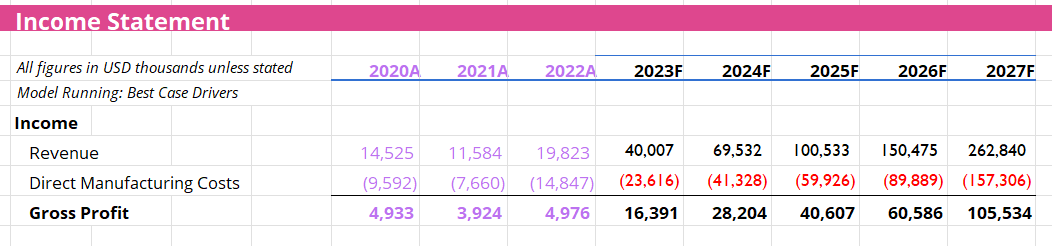

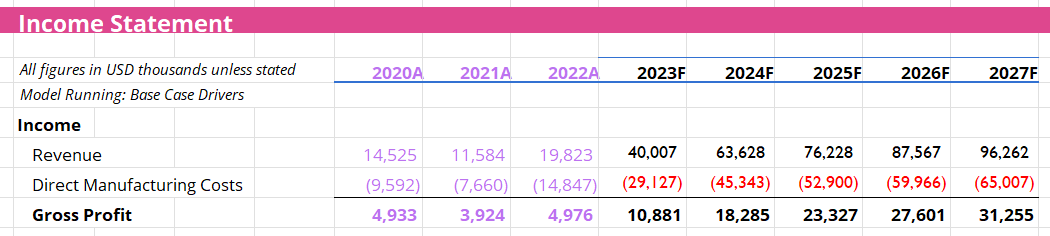

The Base case follows management guidance from the 2022 full-year accounts. It assumes that the Toyota deal continues and sales grow accordingly. By the end of 2022, EFL batteries were in use at 80 different sites in the US (MDA 2022), which is a tiny proportion of the market; the growth potential is enormous, and as long as Raymond continues to sell EFL as its top-of-the-range battery revenue is going to continue to rise.

The Best case assumes that the solid-state batteries currently under development come to market in 2026 and provide another boost to sales growth by providing a sales channel in the Electric Vehicle market. EFL has already proven that it can bring new battery tech to market and manufacture at scale. EFL is investigating solid-state Lithium metal batteries at the Electrovaya labs division. In April 2022, they announced excellent performance results in line with the best announcements from their larger, better-funded competitors. It is also possible that Electrovaya adapt their current battery range to the EV market, something they have been hinting at for two years.

The Worst case assumes that the Toyota deal collapses and revenues return to 2021 levels. If this happens, EFL will fail. It does not have the cash to survive any significant negative impact. I will not present any further figures for this worst case.

The worst case could be flagged by a few developments. EFL is, in my opinion, an honest company that will signal the cancellation of any orders or the cancellation of the contract entirely. We may get an early warning sign if Toyota signs a deal with a different battery producer or EFL show reduced revenue in their quarterly reports.

The Top Line

Best Case Revenue (Author Model)

Base Case Revenue (Author Model)

Under both scenarios, EFL will exceed its manufacturing capacity by mid-2024. On October 3rd, EFL announced that they had signed a deal on a 137,000 square-foot factory in Jamestown, NY, that they will build out in stages and end up with a capacity of 1GWh, current capacity is a quarter of a GWh.

Management guidance is for $75 million in total CAPEX requirements to build out this facility. The purchase structure is similar to the Electrovaya Labs facility, which EFL rents from the family of the directors. An unusual related party transaction.

From the 2022 MD&A note 8 (which also covers the Electrovaya Labs deal) we get

On November 1, 2022, the Company entered into an agreement with Sustainable Energy Jamestown (“SEJ”), a party related to shareholders of the Company for the purchase of the building at 1 Precision Way, Jamestown, NY. The purchase agreement sets the purchase price at $5,500 less any expenses incurred on behalf of the related party to date and the repayment of the deposit of $550. The purchase is expected to be finalized on or about June 30, 2023

I am unclear who will own the new property and how it will be financed; however, where the money is going does not affect the cash flow, which is the main output of the model. I looked up the repayments of a $5.5 million commercial property mortgage on the internet, added 15%, and put this in as a lease payment. EFL gave SEJ a loan of $0.5 million to pay for the deposit on the property. The loan bears no interest and has no redemption date, I adjusted cash and put the debt on the balance sheet.

Accounting for the new facility (Author)

In 2019 Electrovaya moved to a 62,000-square-foot facility in Ontario. The facility was producing batteries by the middle of 2020, and despite the well publicised supply chain problems in the industry, EFL delivered 97% of orders on time in 2020 and 100% in 2021 (page 3 MDA Pt4). I have a lot of belief in EFLs ability to get this new facility up and running on time and within budget.

The model also predicts a negative cash balance in 2023 and 2024. I have used the revolving credit facility as if it were an overdraught to cover this. However, it is unlikely that management will fund it this way and the model will need to be adjusted later. The cash generation is unaffected by this balance.

Forecasting Costs

Direct Manufacturing costs

EFL has proven its ability to manufacture at volume. In 2022 they were awarded ISO 9001:2015 certification for the design, manufacture, and repair of Lithium-ion Batteries. Their ability to manufacture and deliver a significant increase in product is excellent, but it has impacted cash.

COGS generator (Author Model)

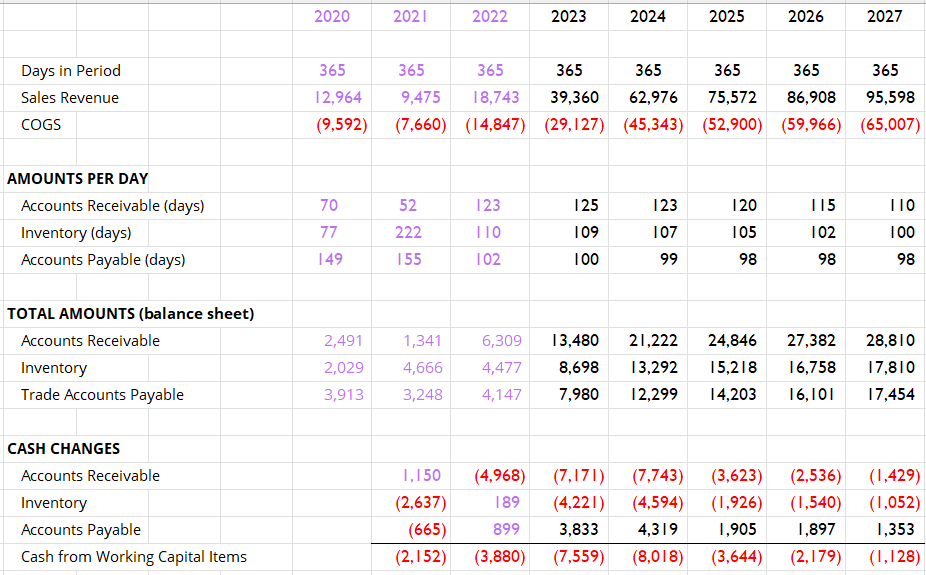

Accounts receivable days have blown out to 123 from 52. At the same time accounts payable days have fallen from 155 to 102. That has squeezed cash flow. I have assumed that these metrics will improve over the coming years, but it might be challenging to make big customers pay early, and the figure might represent the deal signed with Toyota. Will suppliers wait for longer for their cash? Management will have to look at this area.

Other Costs

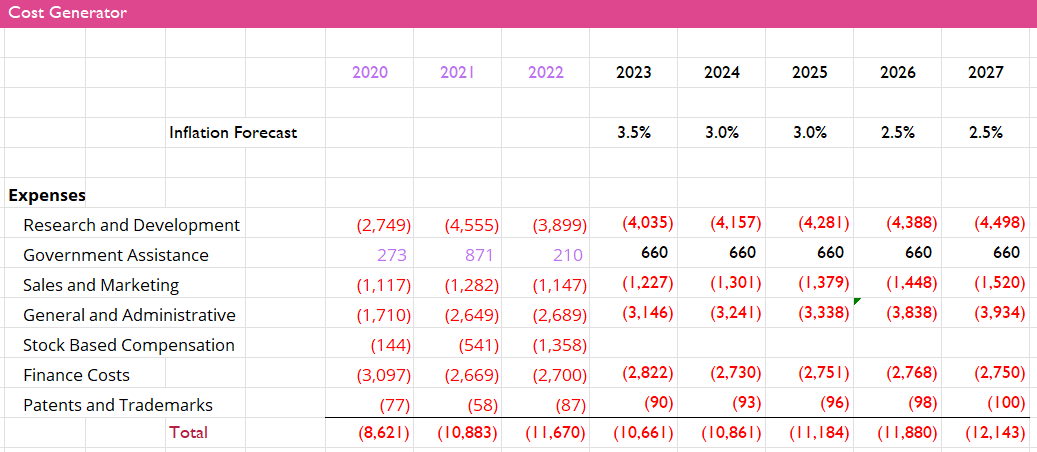

I have used inflation data from the Federal Reserve to generate the following

Expenses Generator (Author Model)

The increase in government assistance figures come from management guidance regarding incentives for the New York building. Although they are unlikely to be equally spread, the total is correct. I have ignored stock-based compensation throughout (non-cash) and have assumed that Sales and marketing will grow at twice the inflation rate (they have been relatively stable) and that General and Admin will have an additional 10% bump in 2023 and 2026. (the opening of the new facility and the potential arrival of solid-state batteries)

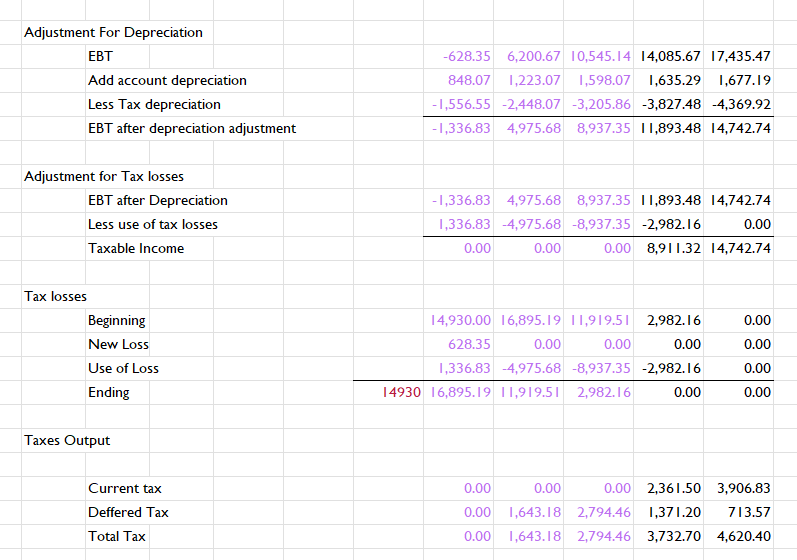

Tax and Depreciation

EFL has not been paying income tax as they have been lossmaking; however, the model suggests that this is likely to end sooner rather than later. I used the Tax losses in the notes to the 2022 annual reports as a starting point to get the following by the end of the forecast period, all Tax Losses have been used. Depreciation was calculated according to the figures in the inputs file,

Tax Generator (Author Model)

Conclusion

The mathematical model explained in this article leads to two valuations in EFL both represent a significant increase from the current share price. If EFL continues to meet its sales and delivery guidance then the forecast changes in valuation are very likely to come to play.

The model is based on the revenue growth guided to by management. They have a deep understanding of the current order book and will be discussing with Raymond on a regular basis. Management have committed to a new factory and the resulting investment. They clearly believe and I will continue to believe them as long as they continue to deliver.

I will update the model with each new quarterly report and report on any material changes but right now I see Electrovaya as the golden egg for 2023 as it was for 2022.

2023 Timing an entry point

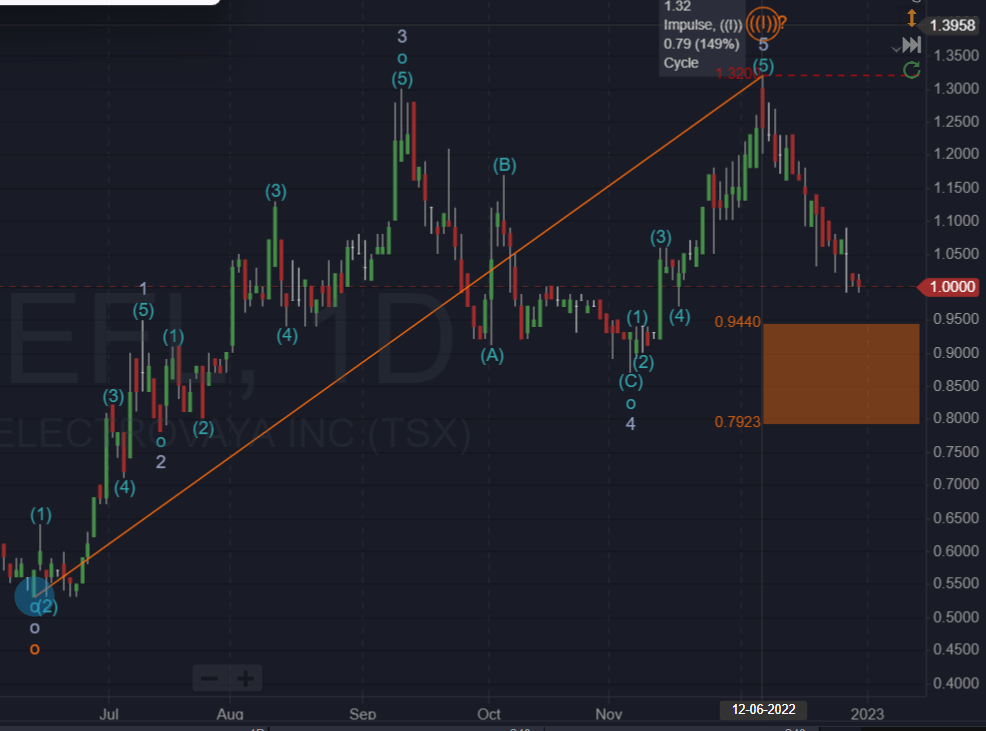

If you are a regular reader of my work, you may already know that I use Elliot Wave Theory to time entry and exit points. It continues to offer great insights into when to buy and sell, and suggests that an entry point is near.

The chart is in Canadian Dollars (that is because my UK-based broker only allows me to buy EFL on the TSX exchange). The (I)? High point might be the end of the first of 5 waves higher and suggests that the corrective wave (2) should end in the orange box before price moves significantly higher. Obviously, there is no guarantee, but I believe that the share price will move from these levels to the ones predicted at the beginning of this article. I intend to buy EFL in the identified area and will update with a comment when I do.

Potential Buying Zone (Author EW)

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment