imaginima

Thesis

The European Equity Fund (NYSE:EEA) is a closed end fund focused on European equities. The vehicle seeks long-term capital appreciation, and at all times at least 80% of the fund’s assets will be invested in equities of issuers domiciled in Europe. This CEF is not necessarily oriented towards income seeking investors since it has only semi-annual distributions (June and January respectively). The fund has had a stable NAV in the past decade, with the valuation hovering around the $9/share mark.

Just like with any other geographic concentration, there are risks and disclosures to be made around the underlying exposures:

This Fund is diversified and primarily focuses its investments in equity securities of issuers domiciled in Europe, thereby increasing its vulnerability to developments in that region. Investing in foreign securities, particularly of emerging markets, presents certain risks, such as currency fluctuations, political and economic changes, and market risks. Any fund that concentrates in a particular segment of the market or a particular geographical region will generally be more volatile than a fund that invests more broadly. War, terrorism, sanctions, economic uncertainty, trade disputes, public health crises and related geopolitical events have led and, in the future, may lead to significant disruptions in U.S. and world economies and markets, which may lead to increased market volatility.

We are glad the fund makes this disclosure because there are jurisdiction specific risks that pertain to Europe. Let us take for example Total (TTE), which is a holding in the portfolio. Total is a French Oil & Gas major which suffered significant impairments due to the geopolitical issues associated with the Russia / Ukraine conflict. An Oil & Gas major from a different jurisdiction (say China or India for example) would not have exhibited the same political risk which translated into an actual loss. All the large multinationals present in the EEA portfolio are subject to the political decisions and train of thought that are prevailing in Europe, starting with sanctions and ending with windfall taxes.

The fund’s performance is in line with plain vanilla ETFs in the space, namely the iShares MSCI Eurozone ETF (EZU) and the Vanguard European Stock Index Fund ETF (VGK). That is a bit disappointing. The fund does not run leverage (only 2.3%), hence we would expect to see an outperformance versus a low cost structure like an ETF. Long term a retail investor should expect around a 5% annualized total return from EEA.

EEA Analytics

AUM: $0.06 bil

Discount to NAV: -14%

Z-Stat: -0.16

St Dev: 19

Sharpe Ratio: 0.1

EEA Performance

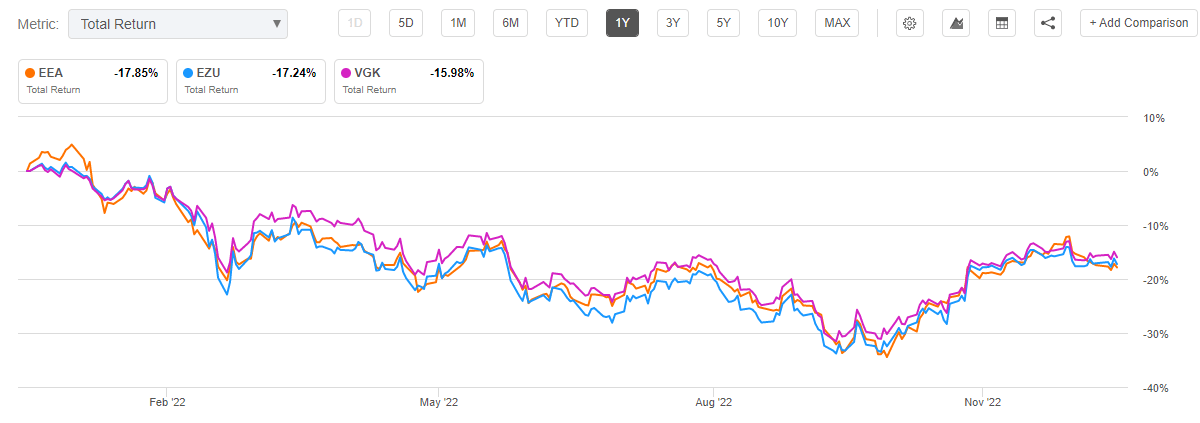

The fund is down approximately -18% in 2022 from a total return perspective:

Total Return (Seeking Alpha)

Its performance is poor, but in line with plain vanilla ETFs in the space, namely the iShares MSCI Eurozone ETF and the Vanguard European Stock Index Fund ETF. Neither instrument has had a good performance in 2022, or outperformed the other tickers.

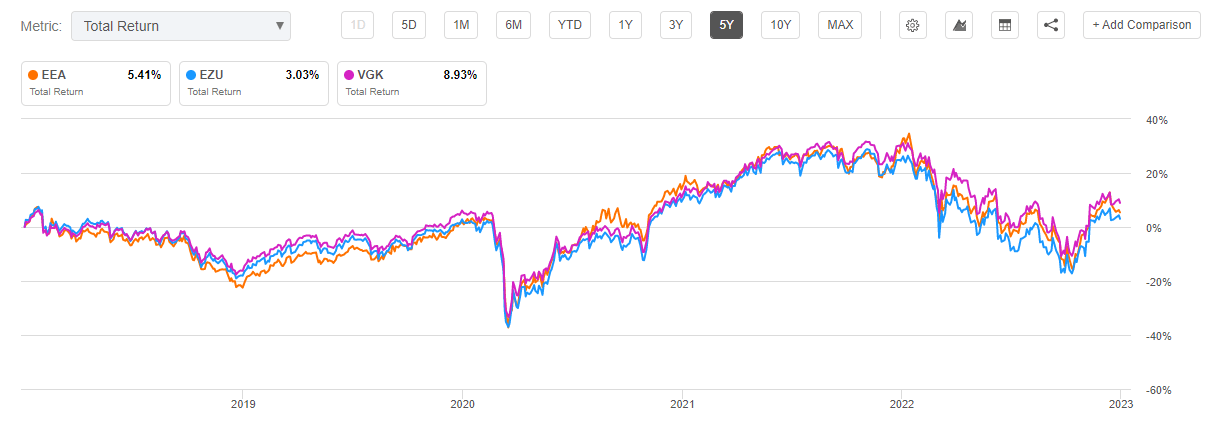

On a 5-year basis the story is similar:

Total Return (Seeking Alpha)

We can see the total returns for the CEF and ETFs pretty much moving in-sync throughout the period. It is a bit disappointing to see an actively managed fund such as EEA not outperform, but that speaks to what we should expect going forward as well.

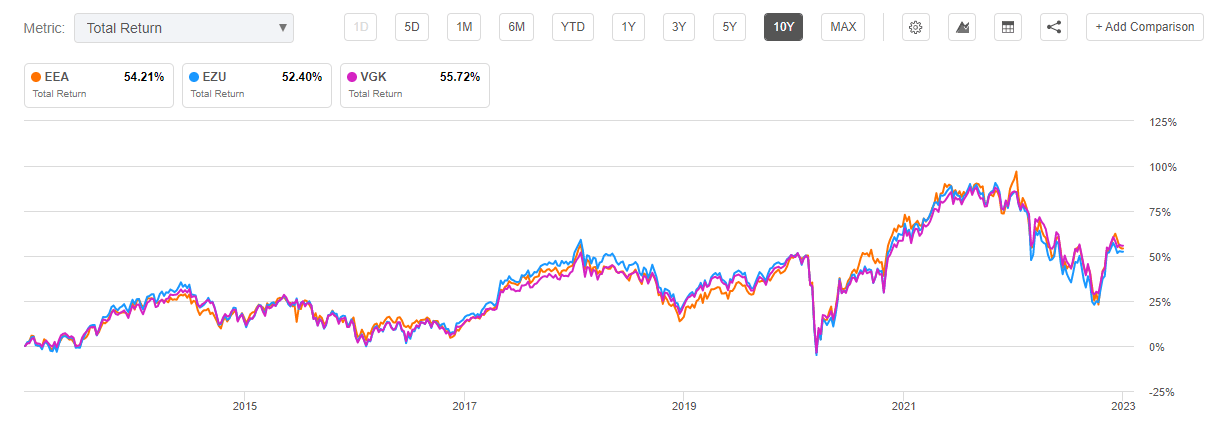

The story is similar on a decade long basis:

Total Return (Seeking Alpha)

If we look at annualizing the fund’s decade-long total return, we get a number close to 5%. This is what an investor should expect from this asset class long term, obviously with cyclicality in between (i.e. following a year with such a big drawdown in 2022 we will see an above average bounce next).

EEA Holdings

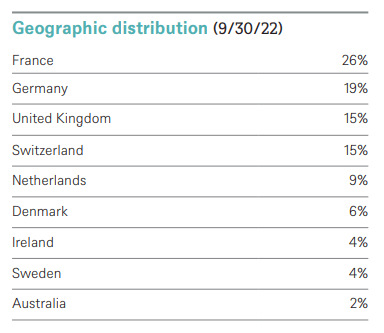

The fund currently contains only European names:

Country Allocation (Fund Fact Sheet)

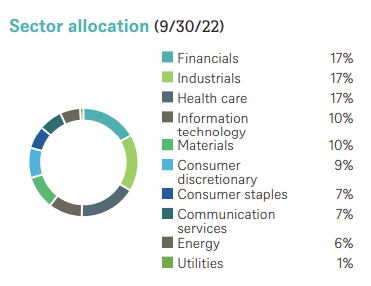

France, Germany, and the UK represent the countries with the highest exposures, as expected. From a sectoral standpoint the fund has a very balanced approach, with the top 5 sectors having above 10% weightings:

Sectors (Fund Fact Sheet)

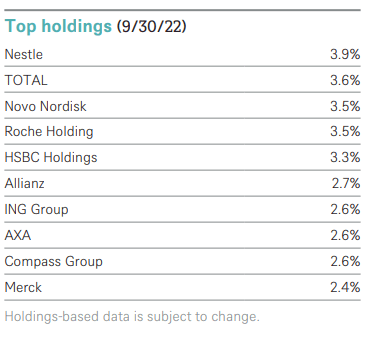

The story is similar when looking at the top issuers in the fund:

Holdings (Fund Fact Sheet)

The top holdings have weightings between 2.4% and 3.9%. There are no outliers as we see in some market value ETFs.

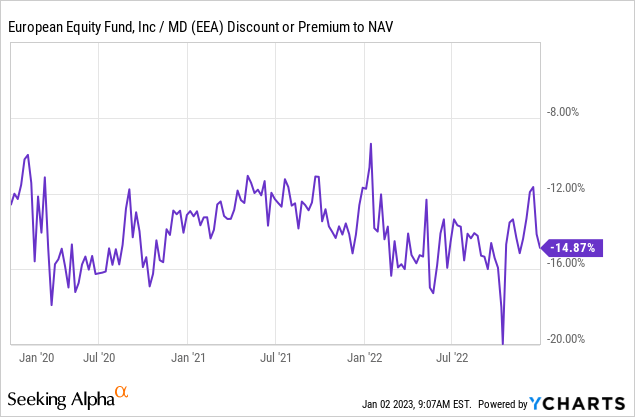

EEA Discount to NAV

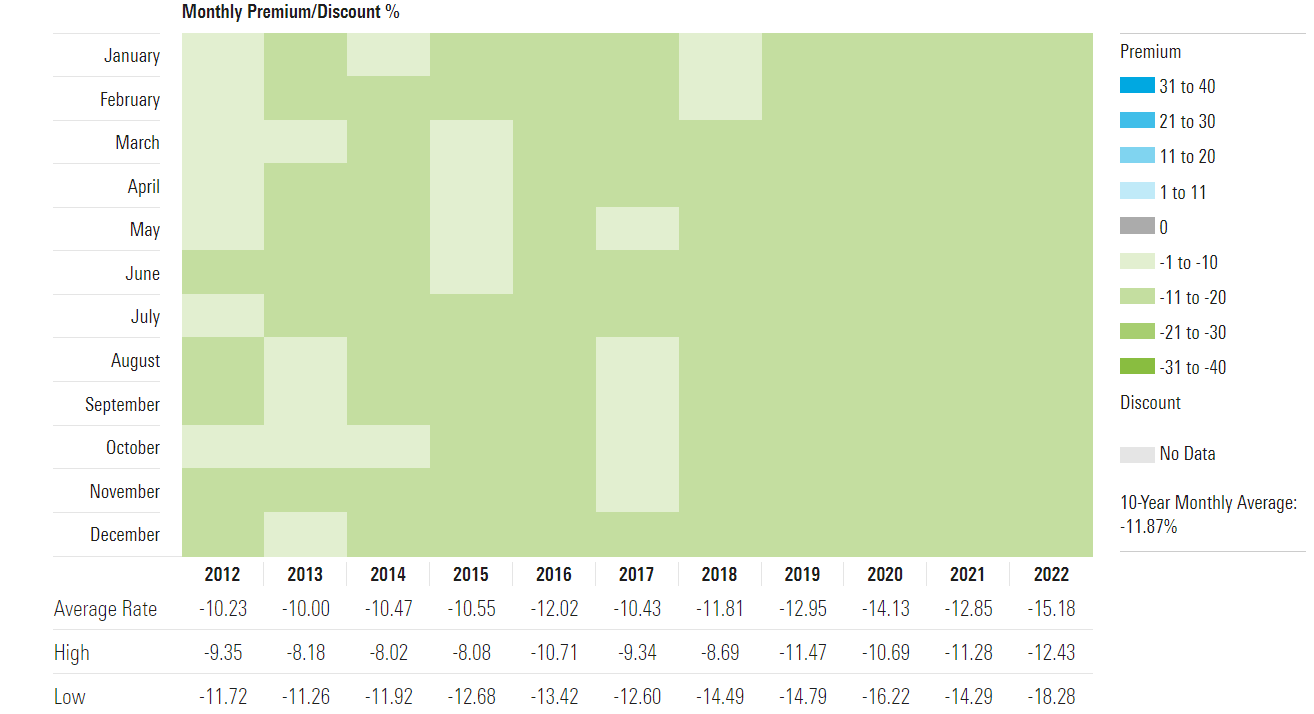

The fund has always traded with a discount to net asset value:

Discount to NAV (Morningstar)

We can see that in the past decade the CEF has always traded at a discount to NAV, discount which averages around -12%. We surmise this is due to the lack of an outperformance for the fund. Why pay high management fees when you can get the same result via an ETF.

We can see that the fund’s discount to NAV has a very narrow, established range:

In the past three years it has been bouncing around in the -16% to -12% range. There is a spike down to -20% during September 2022, which might be on the back of illiquidity and the risk-off move that happened in the wider market. Sharp widenings of the discount can be traded here (as short term trades). There is mean reversion here in the discount, and the market likes this fund at a -12% to -16% discount to asset value.

Can the fund liquidate tomorrow and generate a massive windfall for shareholders via the discount to NAV? Yes, absolutely. Will it? We do not think so since the fees the management clips would be gone.

Conclusion

EEA is a closed end fund focused on large cap European equities. The vehicle has had a disappointing 2022, but its total return is in line with plain vanilla ETFs in the space. The vehicle targets long term capital appreciation and is not extremely well set-up as a CEF: the distributions here are only semi-annual, and there is no managed distribution yield. The fund will only pay what capital gains it musters to make. From a performance standpoint EEA does not impress either – the fund manages total returns in line with less costly plain vanilla ETFs in the space. Lacking the appealing characteristics of a CEF (monthly managed distributions) and the performance metrics to justify its existence, EEA has been trading at substantial discounts to NAV. Currently the discount is -14%, and we expect it to persist. There is not much to like about EEA. A retail investor should expect a long-term annualized return around 5%. Existing shareholders should wait for the 2023 bounce in risk assets before selling, while new money would be better served to look at the vanilla ETFs in the space which offer the same returns with lower management fees.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment