Daniel Balakov

Edison International (NYSE:EIX) has exemplified consistent growth along with solid dividends, providing investors with long-term value. I believe the company is a buy due to its historical outperformance, grid modernization resulting in margin expansion, and undervaluation assuming my DCF figures.

Business Overview

Edison International, and its subsidiaries, operate in the electric power generation and distribution industry. The company serves a vast area of approximately 50,000 square miles in southern California, providing electricity to a wide range of sectors including residential, commercial, industrial, public authorities, agricultural, and others.

In addition to its core electricity supply operations, Edison International is also engaged in offering decarbonization and energy solutions to commercial, institutional, and industrial customers across North America and Europe.

The company’s transmission infrastructure encompasses a network of transmission lines spanning from 55 kV to 500 kV, along with approximately 80 transmission substations. Furthermore, Edison International’s distribution system is comprised of roughly 38,000 circuit miles of overhead lines, around 31,000 circuit miles of underground lines, and 730 substations.

Through its comprehensive electricity transmission and distribution capabilities, Edison International plays a critical role in ensuring the reliable and efficient delivery of power to its customers. Furthermore, the company’s expansion into decarbonization and energy solutions reflects its commitment to providing sustainable and environmentally friendly options to its commercial and industrial clients in North America and Europe.

Company Website

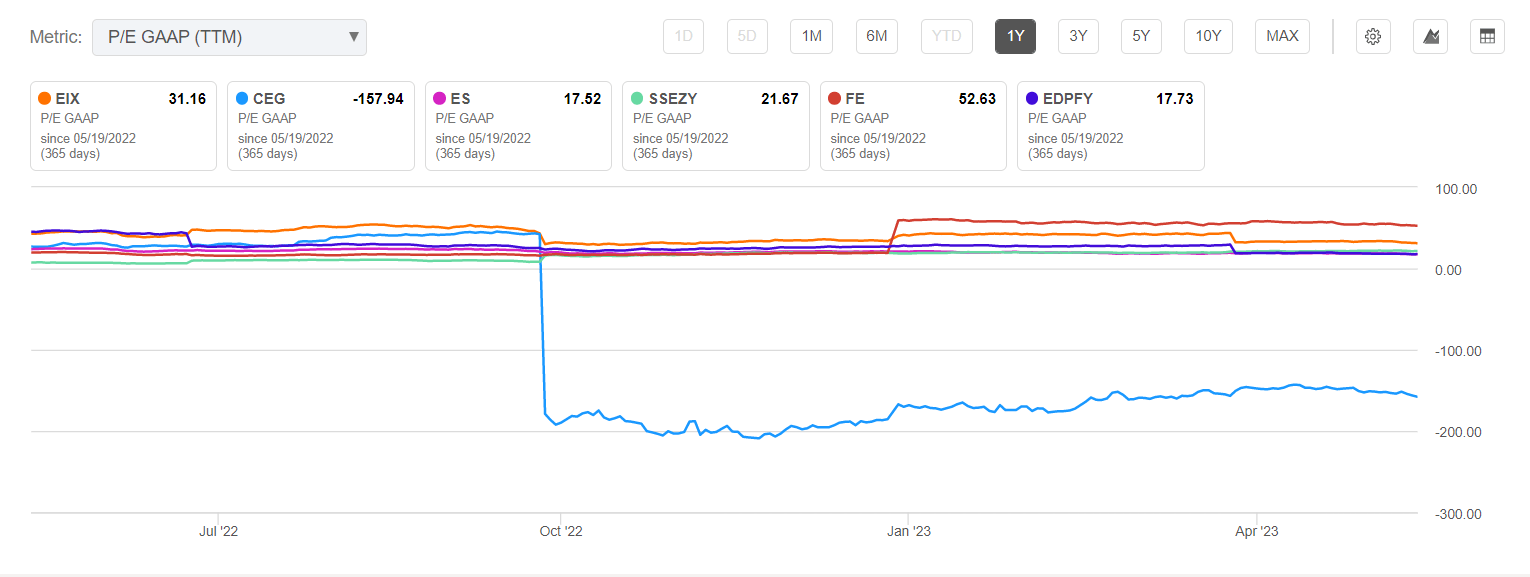

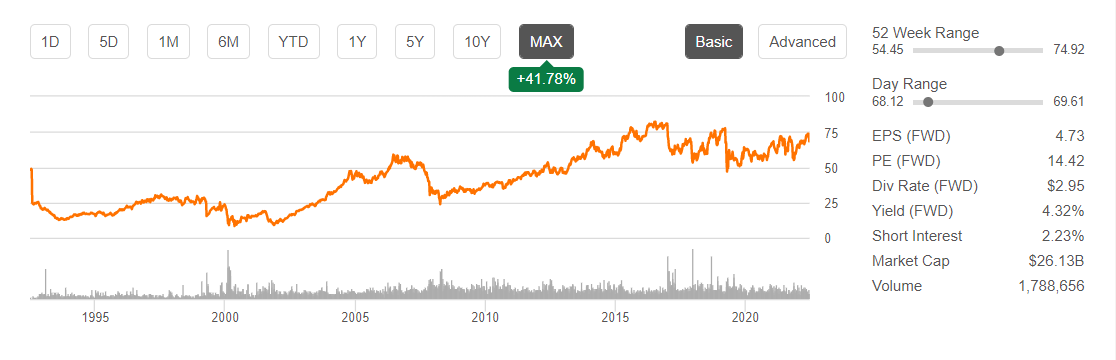

At a market capitalization of $26.135 billion, Edison International has achieved a 52-week high of $74.92 and a low of $54.45. Currently trading at $68.24, the stock’s price is close to its 200-day moving average of $66.48. With a price-to-earnings ratio of 31.16, Edison International is valued higher compared to many of its industry peers.

1Y P/E Compared to Peers (Seeking Alpha)

Edison International also offers its shareholders a robust return through a substantial dividend of 4.32%, which reflects a risky payout ratio of 131.8%. Given its established position as a utility company, Edison International doesn’t require excessive amounts of free cash flow to expand its operations. Instead, it can allocate a portion of its profits to its shareholders while also focusing on its core business objectives. The company has also issued shares over the years, which dilutes shareholders in order to achieve their long-term goals in times when margins are slightly lower. Although I am against the issuance of shares, decreasing a strong dividend for Edison International would be hurtful to their shares as it is known to be an investment that provides stable income along with growth.

Annual Shares Outstanding (Trading View) Seeking Alpha

In Q1 2023, Edison International reported a mixed performance, with earnings per share surpassing expectations by $0.11 at $1.09, while revenues fell short by $30 million at $3.97 billion, showing no year-over-year growth. This indicates that the company has been successful in improving EPS through operational efficiencies, but it is facing challenges in expanding its core business revenues, which could pose long-term concerns.

Furthermore, Edison International provided guidance for EPS in the range of $4.55 to $4.85, with a targeted EPS growth rate of 5%-7% from 2021 to 2025. These mixed earnings result and the in-line guidance suggest that Edison International needs to strengthen its core operations in order to enhance its market share. It is crucial for the company to focus on growth through innovations in order to remain a reliable and successful provider in the industry.

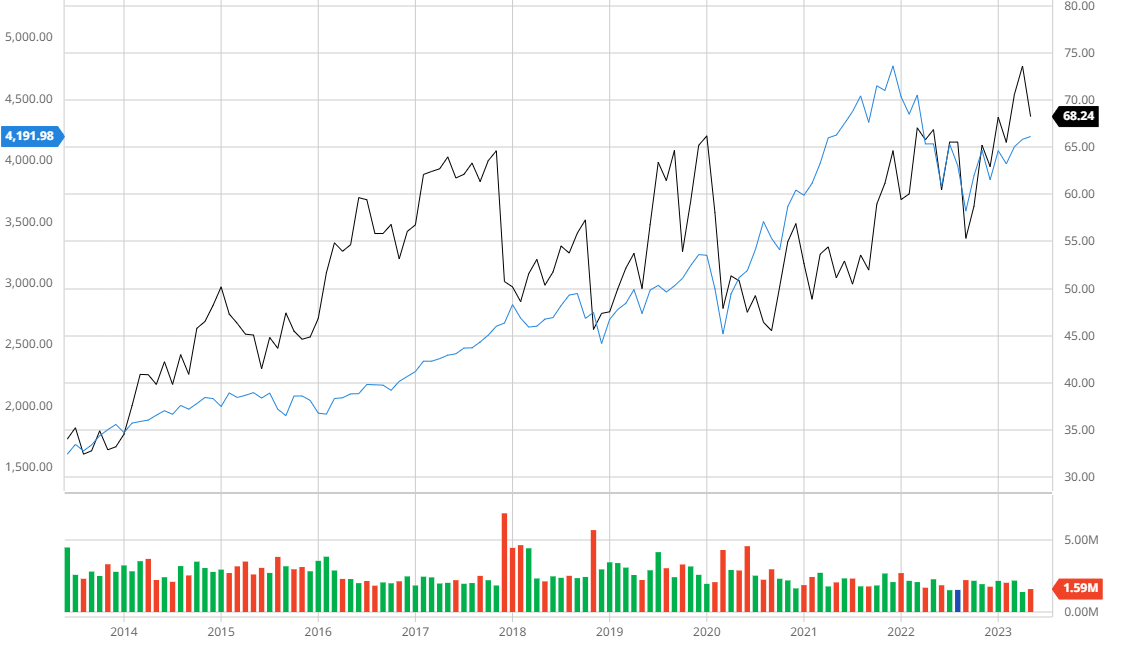

Outperforming the Broader Market

Edison International has demonstrated its capacity to thrive in the long term through consistent growth and its ability to outperform the S&P 500 in the last 10 years when dividends are taken into account. This showcases the company’s enduring value and the steady income it provides to investors.

Edison International Compared to the S&P 500 10Y (Created by author using Bar Charts)

Grid Modernization Fostering Growth

Edison International has consistently worked to improve its grid infrastructure in order to increase overall operational effectiveness. This dedication has led to improved core business stability, better profit margins, and overall growth.

The extensive use of advanced metering infrastructure (AMI) and smart meters is one noteworthy project in Edison International’s grid modernization initiatives. All over the company’s service region, these modern meters have replaced the old analog ones.

Energy usage can be measured accurately and promptly because of smart meters’ ability to communicate with customers and the utility in both directions. Customers now have access to real-time data on their energy consumption, giving them the knowledge they need to choose how much electricity to use, which improves the overall customer experience.

The installation of smart meters has significantly improved the reliability and efficiency of Edison International’s energy system. Smart meters alert the utility right away in the event of a power loss, shortening outages’ durations and increasing the electrical system’s overall reliability. Smart meters have quicker detection and reaction times. Edison International can stay competitive because of the increased dependability, accuracy measures, and less downtime offered to clients.

Furthermore, demand response programs and the integration of renewable energy sources are supported by smart meters. The utility can efficiently manage and balance the supply and demand for electricity thanks to real-time data on energy usage, especially during periods of high usage. In addition to improving grid stability, this maximizes the use of renewable energy sources. Edison International is establishing itself for long-term success by strengthening its core activities and remaining flexible in its adaptation to the changing regulatory environment in the energy sector.

I believe that Edison International’s commitment to improving its grid will result in margin expansion in the future and, with its ability to accommodate renewable sources, will provide long-term security and growth for the company’s cash flows.

Company Website

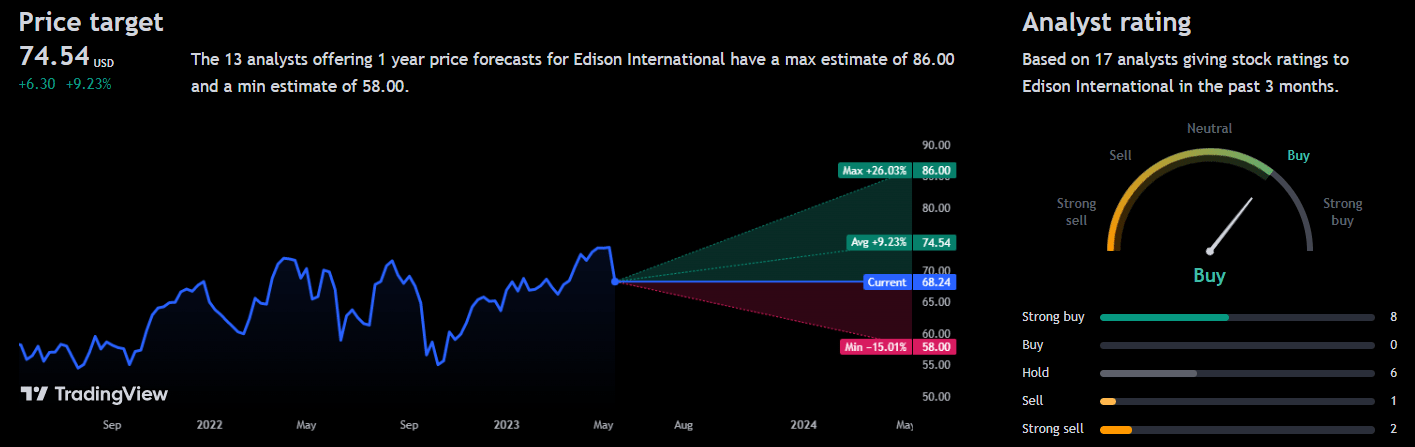

Analyst Consensus

Analysts rate Edison International as a “buy”. The stock exemplifies strong returns and dividends to accompany it with a 1Y average price target of $74.54 which presents a 9.23% upside.

Trading View

Valuation

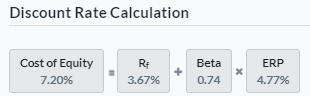

Prior to creating my assumptions, I was able to derive a reasonable discount rate for Edison International by using the Capital Asset Pricing Model method. After integrating a risk-free rate of 3.67%, I was able to attain a Cost of Equity of 7.2%.

Created by author using Alpha Spread

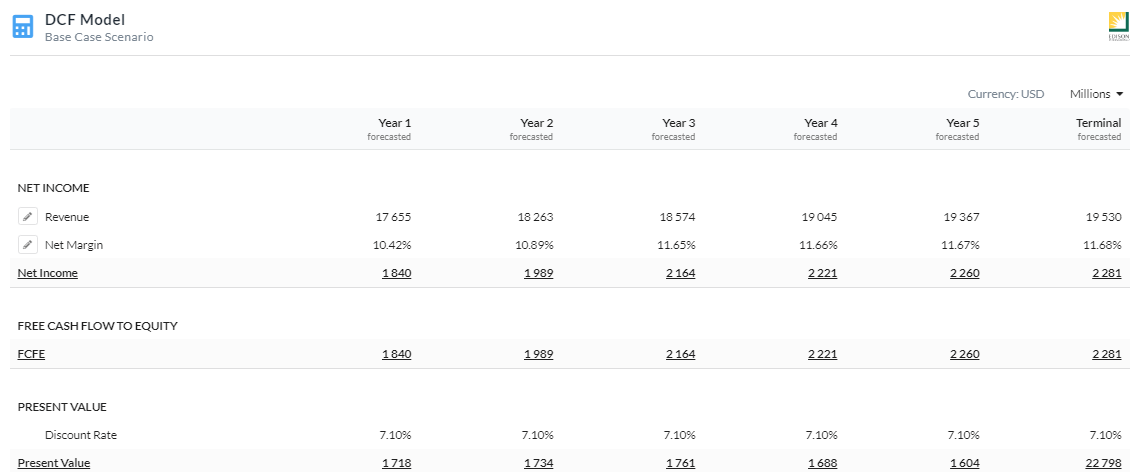

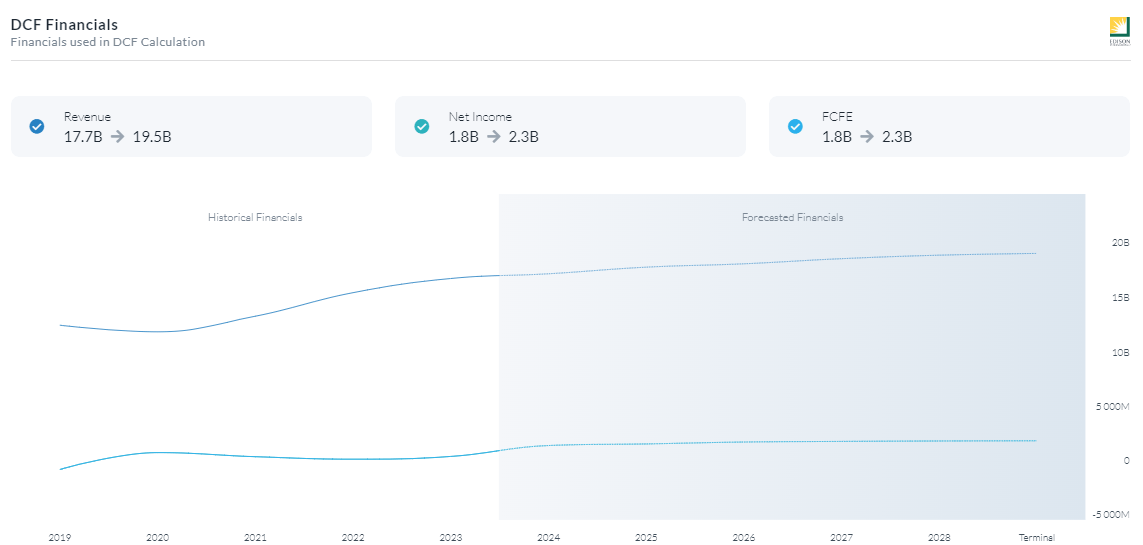

After conducting an Equity Model DCF analysis that utilized net income, I have determined that Edison International’s current value is undervalued by 16% with a fair value estimated at $81.52. This calculation was based on a discount rate of 7.1% for a 5-year period and the assumption of a low-single-digit revenue growth rate beyond 2023 which is in line with company projections. I then assumed that margins would slightly improve due to efficiencies created through their grid modernization upgrades.

5Y Equity Model DCF Using Net Income (Created by author using Alpha Spread) Capital Structure (Created by author using Alpha Spread) Created by author using Alpha Spread

Risks

Operational Risks: Power generation facilities, transmission lines, and distribution networks are just a few of the energy infrastructure components that Edison International manages. Operations can be disrupted, services might be interrupted, and financial losses can ensue from operational risks including equipment failures, accidents, natural catastrophes, and cybersecurity threats.

Regulatory and Policy Risks: At the federal, state, and local levels, the energy sector is subject to a heavy regulatory burden and frequent policy adjustments. The activities, expenses, and profitability of Edison International may be greatly impacted by changes in regulations, environmental policies, and energy pricing.

Conclusion

To summarize, I believe that Edison International is a buy due to its large dividend creating constant income, grid modernization, and undervaluation assuming my DCF figures.

Be the first to comment