Klaus Vedfelt

In this world, personal care is incredibly important. In fact, it may be one of the most important things imaginable. And unfortunately, many people don’t, for one reason or another, put as much care into their own well-being as they should. One company that hopes to change this is Edgewell Personal Care Company (NYSE:EPC), an enterprise that sells a variety of brand-name wet shave products, sun and skin care products, and feminine care products. Like many companies on the market, this particular one has been struggling a bit. Sales have fallen as have profits. Even so, the affordable price that shares are trading for has led to some upside for investors. And if management’s guidance for the current 2023 fiscal year ends up turning out right, we could be due for some additional upside down the road. Because of the upbeat tone the company has provided, I have become a bit bullish about the company, which has ultimately led to my decision to increase my rating on it from the ‘hold’ I had previously to a soft ‘buy’.

Self-care can be profitable

In October of last year, I wrote an article wherein my ultimate decision on Edgewell resulted in a downgrade for the company from a ‘buy’ rating to a ‘hold’. Even though shares of the company still looked cheap at that time, I found the stock pricey relative to similar firms and I was turned off by the mixed results that the company had seen. For context, sales at that time were still rising but profits and cash flows were coming under pressure. So far, my decision to downgrade the company was not awful. But it wasn’t great either. While the S&P 500 is up 2.6% since then, shares of Edgewell have outperformed, rising by 5.4%.

Author – SEC EDGAR Data

To be clear, the troubles cited in my article still persist. To see what I mean, we need only look at data covering the final quarter of the company’s 2022 fiscal year. During that quarter, sales came in at $536.9 million. That’s 1.2% lower than the $543.2 million reported the same time one year earlier. But context is very important when it comes to things like this. Although revenue did decrease, actual organic sales for the quarter rose by 1.2%. The decline, then, was associated with a 6% negative impact from foreign currency fluctuations. The picture would have been worse because of the foreign currency movements had it not been for a $19.6 million contribution that the company had from its acquisition of Billie.

The decrease in revenue was one factor causing profitability for the company to decline. Net income came in at $33.7 million. That’s down from the $44.1 million reported one year earlier. Also problematic was the fact that the company’s gross profit margin fell from 45.1% down to 40.8% year over year. Based on the company’s sales figures alone, this resulted in $23.1 million in reduced gross profit for the company. Management attributed this to higher commodity and transportation-related costs, even though the company benefited from some productivity enhancements. The firm was also hit from a margin perspective to the tune of 1.1% because of a change in product mix and unfavorable foreign currency fluctuations, all net of increased prices that it charged its customers. Naturally, other profitability metrics for the company followed suit. Operating cash flow plunged from $73.1 million to $29.6 million. Though if we adjust for changes in working capital, it would not have been as awful, with the metric falling from $82.1 million to $64.5 million. Meanwhile, EBITDA shrank somewhat, falling from $102.3 million to $94.7 million.

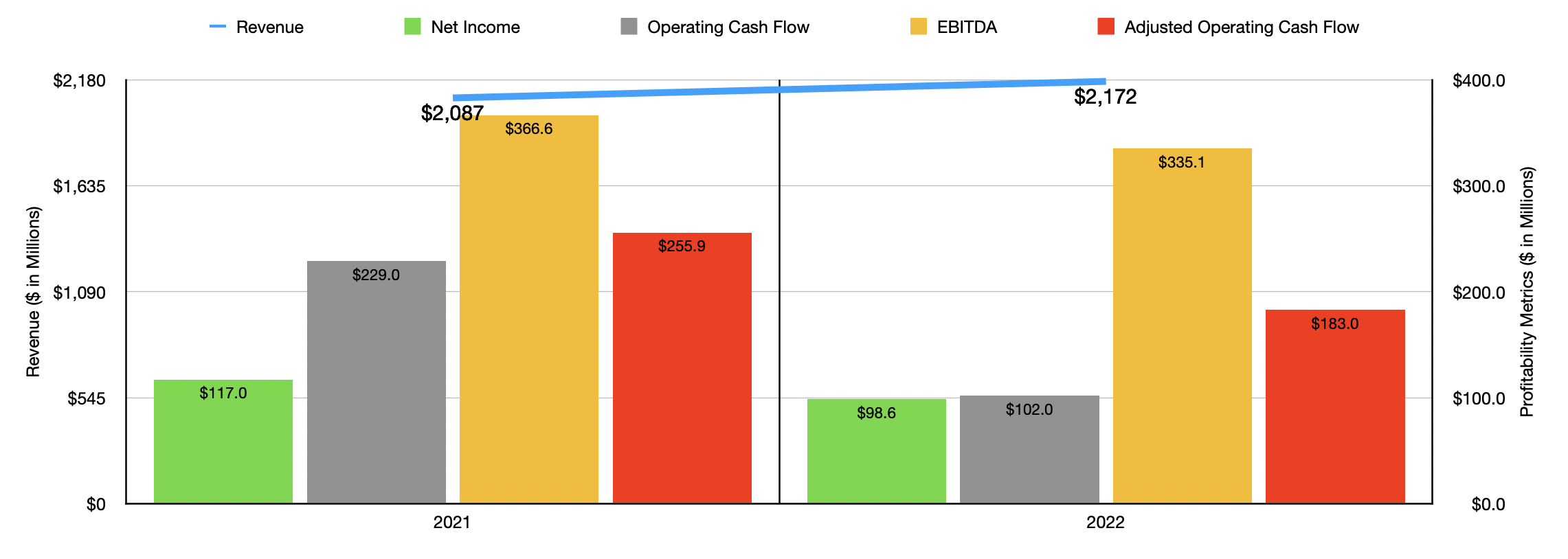

Author – SEC EDGAR Data

What the company experienced in the final quarter of the year was very similar to what it had experienced for much of the year. Sales of $2.17 billion in 2022 actually did come in higher than the $2.09 billion reported in 2021. But margin pressures pushed profits down from $117 million to $98.6 million. Operating cash flow went from $229 million to $102 million. On an adjusted basis, the decline was still steep from $255.9 million to $183 million, while EBITDA fell from $366.6 million to $335.1 million.

Coming into the 2023 fiscal year, I didn’t think that the outlook for the company would be all that great given how 2022 ended up. In particular, the troubles faced in the final quarter showed an acceleration of some of the company’s issues. However, management seems to be upbeat. They currently anticipate overall sales growth to range from 0% to 2%. That should be driven by a 3% to 5% increase in organic revenue. Earnings per share, meanwhile, should be between $1.90 and $2.10, with adjusted earnings of between $2.30 and $2.50. Using the adjusted figures, we would end up with net income for the enterprise of $128.6 million. The company also said that EBITDA should fall by 2% year over year. But actual organic expansion should be 8%. We are looking at a range of between $320 million and $335 million, with the 2% decline fitting right in the middle. No guidance was given when it came to operating cash flow. But if we assume that it will change at the same rate that EBITDA is expected to, we should anticipate a reading of $178.8 million.

Author – SEC EDGAR Data

Based on these figures, the company is trading at a forward price-to-earnings multiple of 16.6. The forward price to adjusted operating cash flow multiple is 11.9, while the EV to EBITDA multiple should come in at 10.2. If we use the data from 2022 instead, which I would say is appropriate given how early we are in 2023, we would get readings of 21.6, 11.6, and 10, respectively. As part of my analysis, I also compared the company to five similar firms. On a price-to-earnings basis, these companies ranged from a low of 14.8 to a high of 95.2. In this case, only one of the five companies was cheaper than Edgewell. Using the price to operating cash flow approach, the range was from 13.5 to 14.7. In this case, our prospect was the cheapest of the group. And finally, using the EV to EBITDA approach, we end up with a range of between 4.5 and 40.6. Two of the five companies were cheaper than our target in this case.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| Edgewell Personal Care Company | 21.6 | 11.6 | 10.0 |

| e.l.f. Beauty (ELF) | 86.0 | 47.1 | 40.6 |

| Coty (COTY) | 95.2 | 13.5 | 12.4 |

| Inter Parfums (IPAR) | 35.1 | 352.4 | 19.8 |

| Olaplex Holdings (OLPX) | 14.8 | 16.6 | 9.6 |

| Natura & Co Holding S.A. (NTCO) | 38.2 | 24.1 | 4.5 |

Takeaway

Fundamentally speaking, Edgewell has shown some weakness, largely as a result of inflation-related margin compression and currency fluctuations. Shares of the company look affordable but not precisely cheap. But they have gotten cheaper relative to similar firms. That’s a big bonus. Add on top of this the mostly upbeat guidance provided by management for the 2023 fiscal year, and I feel as though a soft ‘buy’ rating is appropriate at this time.

Be the first to comment