JHVEPhoto

As with most stocks, eBay (NASDAQ:EBAY) has made a complete round trip to the pre-Covid levels. The online auction service made huge progress in growing TAM and boosting the network effect of the platform, yet the stock has fallen back to $40. My investment thesis remains ultra Bullish on the stock trading at a trough valuation while future prospects are improved.

Back To 2019

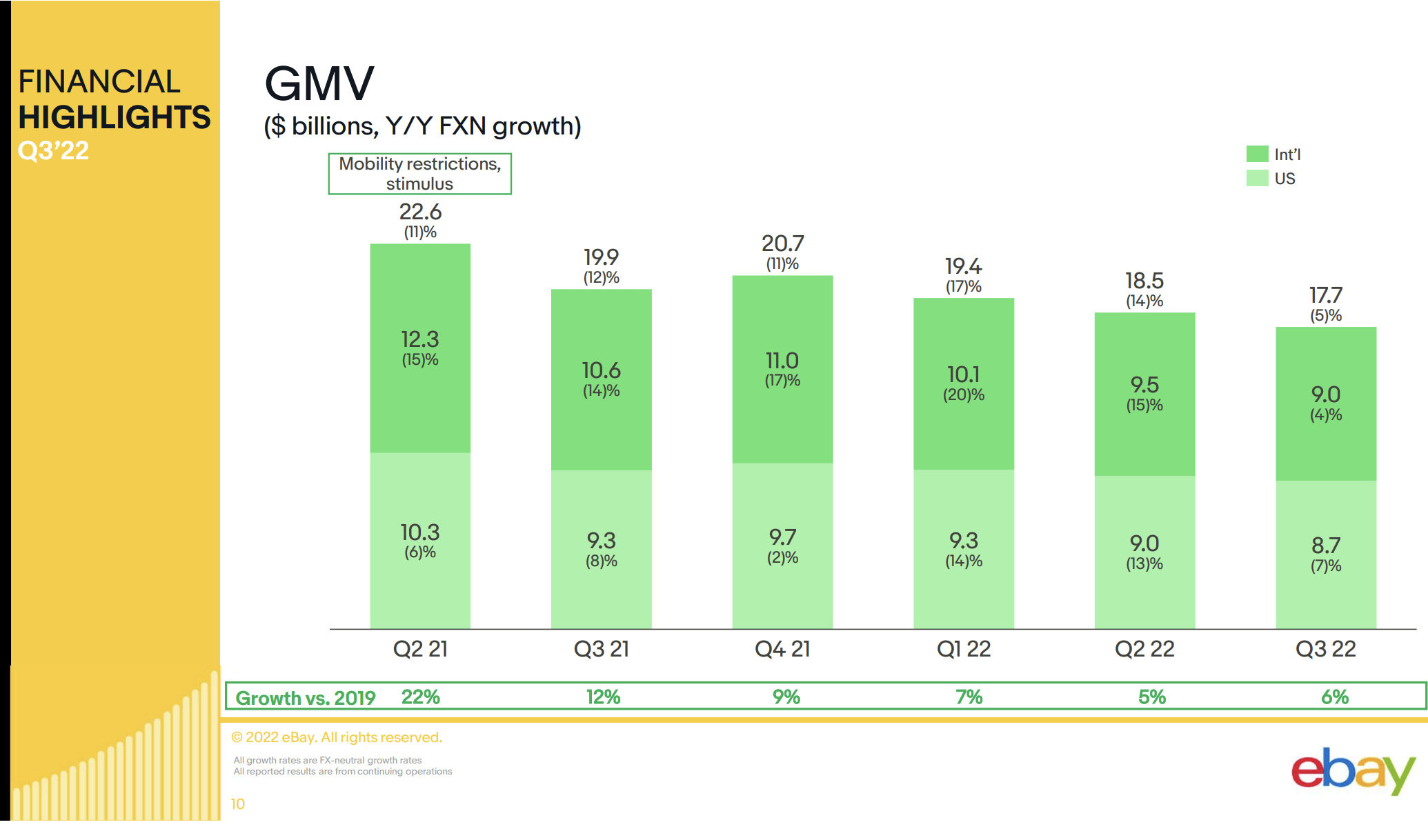

Due to divestments, eBay is hard to compare to prior year periods. The below chart highlights how adjusted GMV grew 22% in Q2’21 compared to 2019 levels with the Q3’22 growth rate slipping to only 6%. The Q1’22 GMV hit $27.5 billion and grew at a 29% clip before the Classifieds business was unloaded to Adevinta (OTCPK:ADEVF).

Source: eBay Q3’22 presentation

The retail sector faces a tough period, so any reported growth now versus 2019 remains impressive. eBay has made great strides in leaning into refurbished items and collectibles in a move to capture niche market opportunities while the prior online auction house just donated market share.

In the trading cards sector alone, eBay has launched a vault to hold valuable collectibles and an authentication service along with buying TCGplayer to further build out a technology platform for the sector. Step by step, the company is working to expand the service offerings where eBay can offer solutions to build upon a simple auction service.

The company provided solid Q4’22 guidance with GMV at $17.8 billion, revenues at $2.46 billion and a solid EPS of $1.06. eBay might actually top the Q4’21 EPS of $1.05 and soar past the $0.81 earned back in the holiday quarter of 2019.

As the Fed slows down on rate hikes, eBay can finally showcase the reimagined platform. The company has now expanded the authenticity service to five categories having recently added fine jewelry costing over $500.

Again, the key here is that eBay continues to build a suite of services to solve problems faced by the basic online auction service of the past. The company has seen these focus categories maintain 20% growth above 2019 GMV levels with trading cards at double the prior levels in a sign of the sustainability of the new model.

Better On A Rebound

The US economy faces a tough 2023 with the potential of a recession around the corner. While the retail environment will likely be tough, eBay is better positioned financially to prosper on the slightest amount of revenue growth in the future.

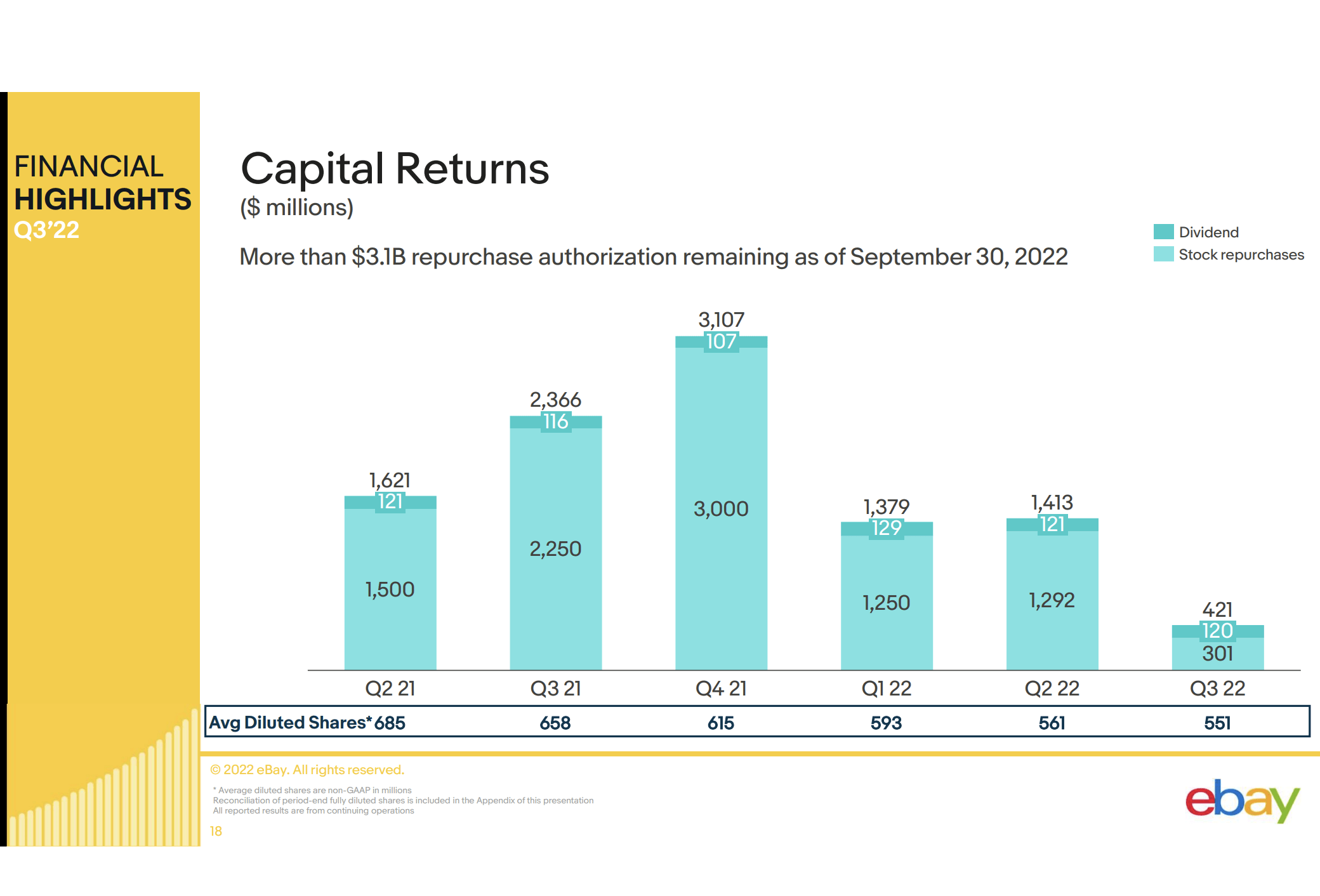

The company has returned $5.3 billion to shareholders in the last 4 quarters alone. The average diluted share count was cut from 685 million shares in Q2’21 to only 551 million for Q3’22.

Source: eBay Q3’22 presentation

A similar income level as the $2.4 billion produced in 2019 would generate a $4.39 EPS in 2023 providing a massive $1.46 EPS boost due to the vastly lower diluted share count of 856 million pre-Covid. The company even pays a 2.1% dividend yield for those waiting for a normal business environment.

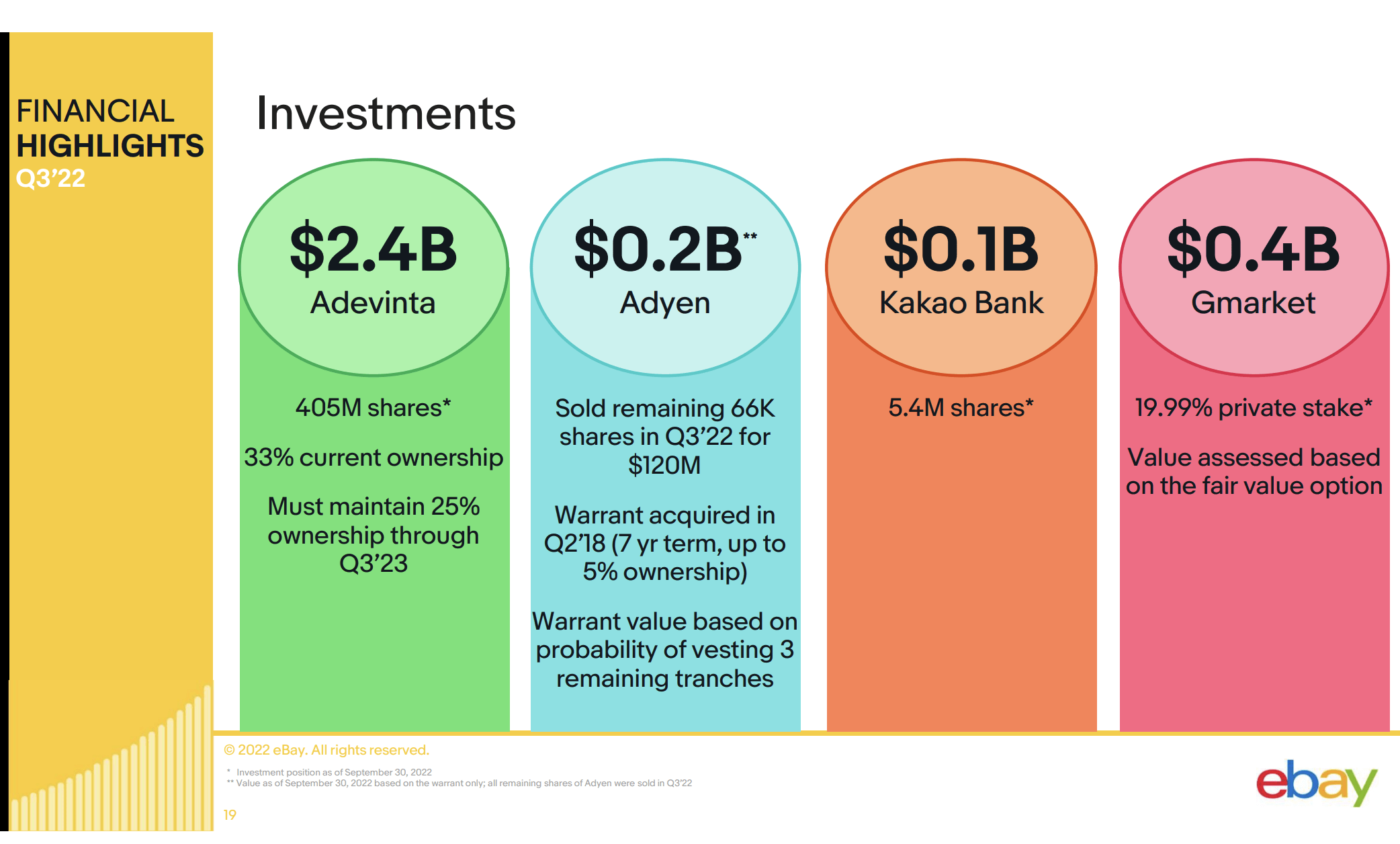

While the company has already utilized most of the cash from selling assets in the last year, eBay still has over $3 billion worth of investments at the end of Q3. The company now has a net debt position of $2.9 billion, but Adevinta has plunged 50% in the last year and the 405 million share position could rally with a market rebound in the new year.

Source: eBay Q3’22 presentation

Investors should be amazed that eBay has maintained a $4+ EPS target in the face of a tough retail environment. The stock trades below 10x 2023 EPS targets of $4.24, though this target actually suggests net income dips below 2019 levels in an unlikely scenario.

Any rebound in growth next year as the business normalizes following the online pull forward during Covid and the stock could easily capture a 15x forward earnings multiple. All eBay needs is a more normal operating environment to highlight the improved business operations for the market to assign a higher multiple on the stock offering a target of $60 to $70 for next year.

Takeaway

The key investor takeaway is that eBay shouldn’t be facing a scenario where the stock trades at pre-Covid levels. The executives have completely reimagined the business, offered growth routes not present prior to 2020 and repurchased millions of shares to provide for a far superior EPS target going forward.

eBay is too cheap at $40 and investors should use this market selloff to load up.

Be the first to comment