JHVEPhoto/iStock Editorial via Getty Images

After several years of repositioning the company, Eaton Corp. (NYSE:ETN) had a relatively quiet year on the M&A front where it could focus on performance. The industrial company sold off its deeply cyclical Hydraulics business in 2021 and acquired several businesses for its Electrical and Aerospace segments. As I have noted in the past, this positions the company to take advantage of secular growth themes related to sustainability, data center growth, and aerospace growth.

Eaton Corp.

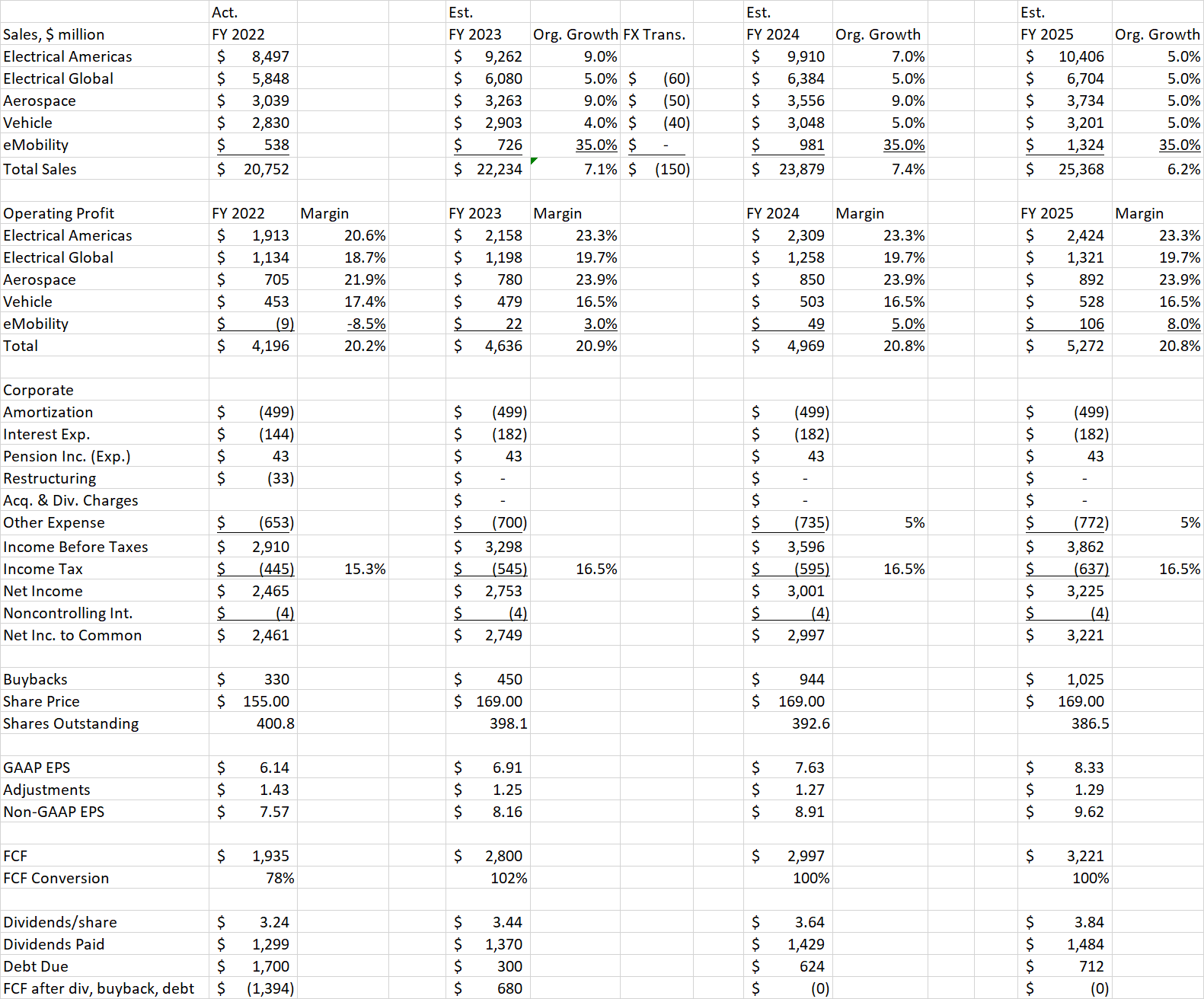

Eaton continued to set sales and margin records in 2022, despite inflation. The company delivered earnings per share of $7.57 (non-GAAP), just above the $7.50 I estimated in my last article. For 2023, the company is planning for about 7% organic sales growth, in line with their longer-term goal of 5%-8%. Operating margins are also expected to grow, with a midpoint of 20.9% forecasted in 2023, up from 20.2% last year.

The Electrical Americas, Aerospace, and eMobility segments are forecasted to grow above the company average. In Electrical Americas, data centers, utilities, and industrial customers are leading this growth, but the company also added commercial and institutional customers to its “solid growth” category this year. Aerospace is benefitting from the resurgence of travel, where more flight hours translate to greater aftermarket parts business. The company noted on the call that they are now also seeing military orders pick up. While Electrical Global is growing just under the company average in 2023, CEO Craig Arnold noted on the call that demand is quickly picking up in China now that they have ended their zero covid policy.

Further amplifying these secular trends, governments in the US, EU, and elsewhere have passed spending programs to encourage sustainability and improve electrical and transportation infrastructure. Eaton believes these programs expand their addressable market by $11 to $14 billion over the next 5 years.

Eaton Corp.

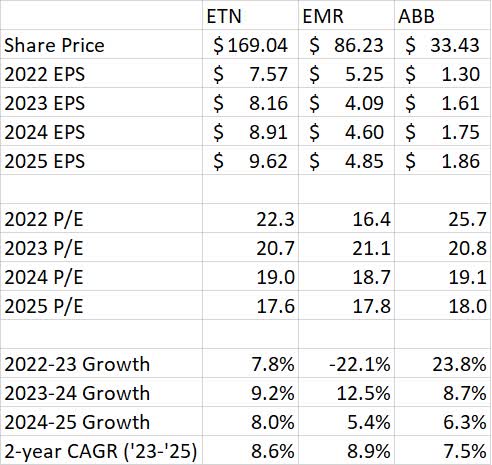

With this sales and margin growth, Eaton expects EPS of $8.04 – $8.44 in 2023. My earnings model below estimates $8.16 which is within the range. That puts the stock in the 20 – 21 P/E range, similar to peers. That is getting expensive for a company that is growing EPS in the 8-9% range. I now consider Eaton a hold following the strong share price performance of the past year.

Earnings Model Update

For 2023, I am using midpoint sales growth and operating margin estimates from the company earnings presentation. Interest expense is higher as the company increased debt in 2022. The main negative compared to my earlier estimates is the “other expense” is now at $700 million in 2023 after finishing at $653 million in 2022, also higher than what I used in my last article. Using the company guided tax rate of 16.5%, I get my non-GAAP EPS estimate of $8.16 for 2023.

In 2024 and 2025, I keep eMobility sales growth strong at 35% for this new segment due to its growing market in the EV and charging area. I conservatively show Electrical Americas and Aerospace sales growth tapering back down to 5% following a strong 2022 and 2023. This results in company average sales growth of 7.4% in 2024 and 6.2% in 2025. Craig Arnold noted on the call that he would be “surprised if sales growth did not exceed the 5%-8%” long-term goal, at least in 2023, so there could be upside to my forecast. The resulting non-GAAP EPS is $8.91 in 2024 and $9.62 in 2025, a growth rate of 8-9% per year.

Author Spreadsheet

Valuation

Eaton’s share price was $169 share price at time of writing, up about 10% from my prior article. Competitors Emerson Electric (EMR) and Swiss company ABB (ABB) are both valued similarly to Eaton based on P/Es whether you look at 2023, 2024, or 2025 earnings. All three companies also have EPS growth rates in the 7.5%-8.9% range over the next two years. While all of these companies are fairly valued compared to each other, they are expensive on an absolute basis with a 2023 P/E in the 20-21 range. This is more than twice the expected growth rate and near historical highs despite the negative effect that higher interest rates should have on stock valuations.

Author Spreadsheet

Capital Management

Eaton had free cash flow of $1.935 billion in 2022, only 78% of net income and below the guidance given last quarter. This shortfall was due mainly to working capital build as higher inventories were needed to manage supply chain constraints but also to work on a large order backlog and prepare for higher future sales. The company paid out about $1.3 billion in dividends and spent $330 million on buybacks. However, they also had to pay off existing debt of $1.7 billion in 2022, so they ended up issuing new debt to replace it.

In 2023, Eaton forecasts free cash flow of $2.8 billion at the midpoint, closer to 100% net income conversion. I expect the company to raise the dividend by $0.05 per quarter, to $3.44 total for the year. This would be a dividend yield of 2% and a payout ratio of 42%. This will consume $1.37 billion of cash. The company also guided to buybacks of $450 million this year at the midpoint. Eaton also has $300 million of debt due this year. This leaves $680 million of cash after these actions, so there is upside for increased buybacks or an acquisition.

In later years, assuming 100% conversion and continued $0.05 quarterly dividend hikes each year, Eaton should be able to afford higher buybacks in the $0.9-$1.0 billion range after paying off debt.

Conclusion

Eaton delivered an impressive 2022 with record sales and operating margins. This is expected to continue in 2023 despite broader macroeconomic worries. This is a result of the repositioning Eaton finished by last year to get rid of cyclical businesses and become more tied to secular growth trends.

At $169, Eaton stock is up about 10% since my last review. It looks fairly valued compared to peers, but at above 20 P/E it is not cheap considering the 8%-9% EPS growth or the higher interest rate environment. Eaton is still worth holding for its long-term secular growth compared to more cyclical companies in the industrial sector. ETN stock is now a Hold due to its high valuation, but I would consider adding at lower levels.

Be the first to comment