georgeclerk/iStock Unreleased via Getty Images

In November 2022, I covered the most recent results of easyJet (OTCQX:ESYJY) and noted that shares were not a buy in my book on softness in fares. The company has now provided Q1 2023 that are pleasing the market as the stock is trading more than 10% higher at the stock market in London.

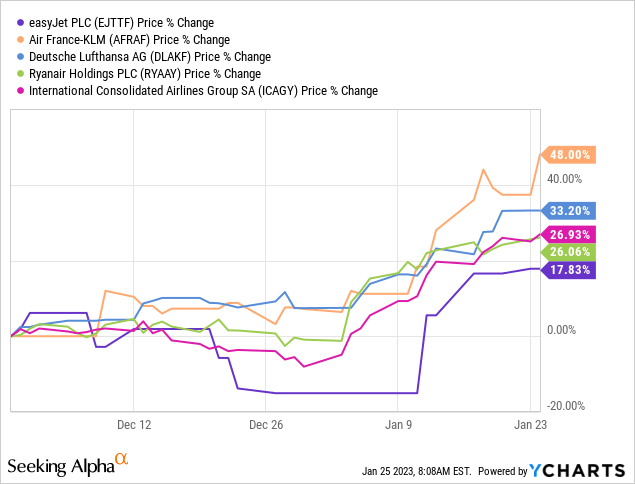

easyJet: Outperforming The Market, Underperforming Peers

Share price performance easyJet (Seeking Alpha)

As mentioned, in my previous report on easyJet I was not particularly impressed with easyJet’s results as base fares were soft when the ancillary revenues are excluded, which I believe is a result of the competitive environment that easyJet is active in. Nevertheless, share prices are up nearly 18% on a 1.5% appreciation for the broader market. So, was I wrong issuing a hold rating instead of a buy rating? I actually don’t think I was.

Looking at the performance at some peers, we see that carriers with exposure to the UK were not among the strongest performers and easyJet was one of the weaker performers and the weakest performer in the basket of airlines that I added to the chart.

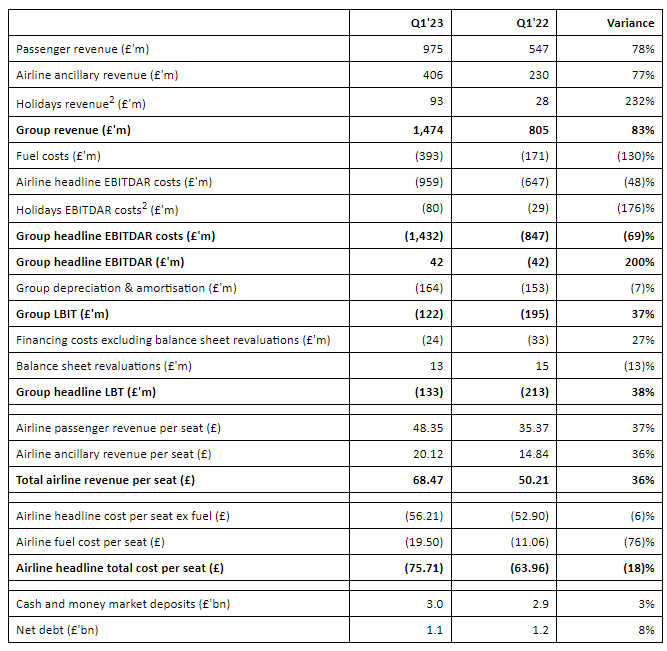

Results Show Improvement

easyJet Q1 2023 results (easyJet)

The results show improvement, overall we see airline passenger revenue per seat and ancillary revenue per seat up by roughly the same percentage and we are seeing some fare strengthening compared to pre-pandemic, which is what you would be looking for at this point. Combined with higher capacity, revenues grew by over 80%. The quarter was profitable on EBITDAR level swinging from a £42 million loss to a £42 million profit. Costs per seat were up 18% driven by inflation and high fuel costs. At the time of writing we don’t have the slide deck from easyJet available yet, but I would say that first quarter results were strong than what one would think bases on previous results and guidance.

Strength Persists

One major concern at this point when assessing the upside for airlines is how long the strong demand environment will persist. What we’re hearing across the industry is that the demand environment continues to be strong with little change expected despite recession fears. The company expects significant improvement in its H1 2023 loss as capacity will grow by 25% year-over-year and a modest increase of 9% in the second half of the year meaning that year-end capacity is 96% recovered compared to pre-pandemic levels. That indicates that unit costs should decline significantly while 78% of fuel usage for H1 has been hedged at a price >25% lower than current prices and 59% hedged for H2 at a price roughly 20% below today’s prices. At current standing that should unlock some fuel hedge gains.

Concurrently, the carrier sees booking strength continuing into the summer and it expects to grow its Holidays customer based by 50% up from >30%.

Conclusion: Upgrading easyJet Stock To Buy

I will most likely revisit the earnings and outlooks once the slide deck has been made available. However, what I can already see is that the fare weakness that seemed to be holding back easyJet is fading, meaning that its Holiday business, recovery in unit costs and manageable net debt become more prominent and appreciable. While there are concerns on the health of the British economy, I do believe the aforementioned dynamics warrant an upgrade to buy from hold.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

If you want full access to all our reports, data and investing ideas, join The Aerospace Forum for the #1 aerospace, defense and airline investment research service on Seeking Alpha, with access to evoX Data Analytics, our in-house developed data analytics platform.

Be the first to comment