grafficx/iStock via Getty Images

Chairman Powell seemingly dispersed his central bank troops yesterday to send a message to investors that they should rein in their enthusiasm for risk assets, which has been loosening financial conditions since last October, until the Fed gives the all clear on the monetary policy front. Powell’s tone on Tuesday was relatively even-handed, which led to another surge in stock prices that he probably wanted to put in check. Therefore, several Fed officials, led by New York Fed President John Williams, warned that if financial conditions continue to loosen, more rate hikes may be needed. This is the game of cat and mouse that the Fed continues to play with the markets, and it erased most, but not all, of the previous day’s gains. It doesn’t change Powell’s ultimate goal, which is a return to pre-pandemic inflation rates without undermining the current expansion.

Finviz

It appears to me that Powell is on track, which is why “fighting the Fed” has been extremely rewarding with the S&P 500 up as much as 16% over the past four months. The market is telling me that the Fed won’t have to raise rates as high, or for as long, as it continues to say it will, largely because the rate of inflation will fall faster than the consensus expects, while the economy continues to grow. Last week’s jobs report raised doubts for many, as reflected by bets in the interest-rate options market that reflect the Fed’s benchmark rate could rise as high as 6%. That is a lot higher than what the consensus was thinking before last week’s blowout jobs report.

Bloomberg

Yet the positive I am drawing from this hawkish turn in sentiment is that stock prices are holding up exceedingly well in light of it. Additionally, when these bets reverse, and market expectations for short-term rates comes back down to levels where they stood prior to last week’s blowout jobs report, it could produce another bullish tailwind for risk assets.

Initially, it was very surprising to see Wall Street pundits make as big a deal as they did about an outsized gain in one monthly jobs report, which was clearly an outlier, but the consensus on Wall Street has been overly bearish this year. When you are on the wrong side of the market, even for a four-month stretch, you are going to grasp for straws that affirm your position. Obviously, bulls like myself are doing the same thing, but I think the incoming data is predominantly in favor of an outlook that leans more bullish than bearish. If the facts change, then I will too.

I think it is silly to conclude that just because we had a spike in low-paying service sector jobs for one month, we are going to see a similar spike in wage growth that undermines the disinflationary trend that started last summer. That is what Fed officials were extrapolating from the report yesterday, but I just see it as part of this ongoing game of cat and mouse to keep speculative juices in the markets at bay. The same thing is being done with the one-month uptick in used-car prices, which hawks are somehow concluding will lead to an end of the disinflationary process. These price declines do not move in a straight line.

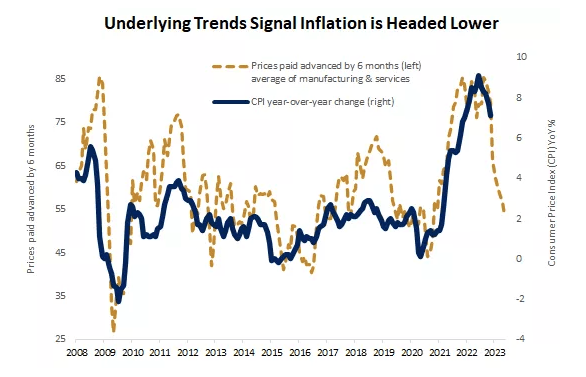

Instead of focusing on a lagging indicator like the monthly jobs report or one-offs that are clearly anomalies, investors should be focusing on leading ones that tell us where the rate of inflation will be tomorrow. I think one of the best is the prices paid index for manufacturing and services companies, which has dropped precipitously in recent months. This tells us where consumer prices are headed.

Edward Jones

I think the stock market’s performance is reflective of the leading indicators, and it happens to be one as well, as it tends to discount macroeconomic events that have yet to occur. The bears on Wall Street are telling us “don’t fight the Fed,” but I suggest they “don’t fight the tape.” The Fed is compromised in its messaging, because it has to manage expectations with its language and its forecasts. The market is not.

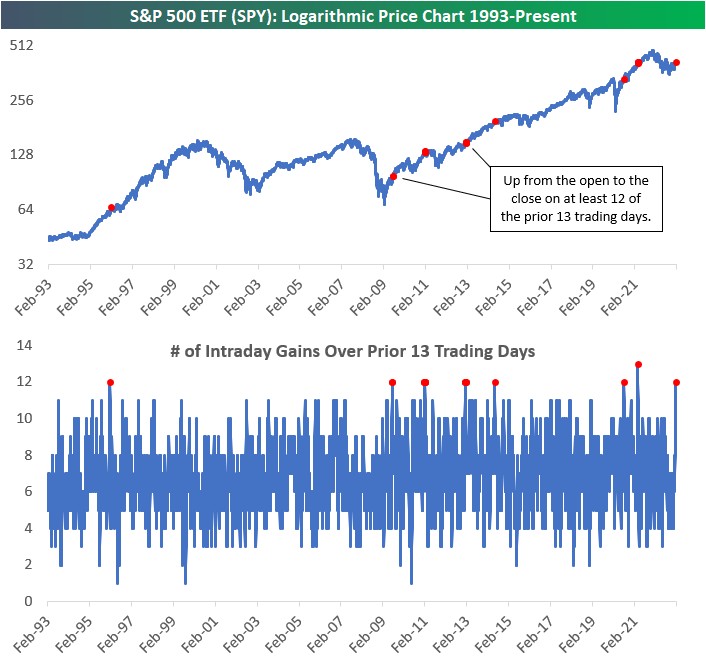

Just as I start to lose track of how many bullish market indicators we have seen since the beginning of this year, Bespoke Investment Group brings another to the table yesterday, noting that 12 out of the past 13 days we realized closing prices for the S&P 500 that were higher than the open. That is an extremely unusual event, as can be seen below in the seven prior occurrences over the past 20 years. As Bespoke points out, none occurred during bear markets. My confidence that we have a new bull market at hand continues to grow.

Bespoke

Be the first to comment