AsiaVision

Investment thesis

I recommend to go long DCGO. There is a growing number of virtual care cases that conventional telehealth services cannot address. To provide this final stretch of medical assistance, DocGo (NASDAQ:DCGO) has developed a unique set of tools and services. Since DCGO has only just begun to scratch the surface of a potentially enormous addressable market, I have faith that it can sustain rapid, profitable expansion.

Business overview

DCGO is a telehealth service provider. It partners with a network of healthcare professionals across the nation and UK to provide such services. As of FY21, 97% of revenue were generated from the US.

Telehealth is fast growing and large addressable market

DocGo is one of a kind because it straddles the line between the healthcare mobility and telehealth industries. It is worth noting that DCGO currently holds only a tiny fraction of this enormous TAM. McKinsey predicts that the telehealth market could be worth as much as $250 billion. With regards to DCGO Mobile’s telehealth offerings, the addressable market is estimated to be around $80 billion (according to the S-1). I think that COVID has accelerated the adoption of services like this because it has drastically changed the way the healthcare system functions and how patients engage with it.

There is also a younger generation that is more tech savvy and a growing elderly population that needs care more frequently. The current healthcare system has undergone a dramatic shift as a result of this. With telehealth, the consumer demand for easier access to care and an improved user experience can be met. However, the capabilities of most current telehealth solutions are inadequate. There is no way for doctors to physically examine or treat patients, and most interactions take place solely online. Because of this dynamic, telehealth loses much of its value and many patients end up seeking treatment through the conventional healthcare system.

Accordingly, the promise of virtual care will never be realized by current telehealth offerings unless they are significantly improved through innovation. DCGO Mobile Health’s “last mile” healthcare solutions, in my opinion, have the potential to close this chasm.

DCGO offers an integrated platform

In my opinion, DCGO is the first company to develop a comprehensive mobile healthcare and medical transportation platform. The goal of this platform is to monitor resources and anticipate effective methods for delivering healthcare on the go. DCGO employs AI to choose and send out the appropriate vehicles and staff according to patients’ medical needs, to deal with the unpredictability of traffic so that patients can get to their appointments on time, and to evaluate the insurance costs associated with each trip.

As one can imagine, transportation within a healthcare system, especially for patients being admitted or discharged, must be reliable and high-quality. When it comes to patient care, DCGO’s platform is fully integrated with some of the largest Electronic Medical Records [EMR] systems in the country. This cutting-edge network integration helps healthcare organizations better track and control their business processes with the help of their business partners. In the past, hospitals’ staff had to call in for transportation and then repeatedly check in to see if the car had arrived. This occupies precious minutes that can be put toward getting ready for the patient’s arrival and providing quality care once they arrive. Until the patient reaches their destination, their whereabouts are typically unknown after they have been picked up. However, with the DCGO system, transportation requests can be made easily with just a few clicks from any devices connected to the web. DCGO’s proprietary algorithms, in my opinion, are the driving force behind its unparalleled on-time performance because they enable smart fleet routing, maximize vehicle utilization, and provide precise arrival and wait time estimates. In addition, DCGO’s EMR integrations streamline everything by importing verified patient data straight from the hospital’s EMR system. Using an EMR provided by a hospital partner is a time-saver because it eliminates the need to collect a patient’s medical history from scratch.

DCGO technology increases the transparency, efficiency, and predictability of healthcare transportation, enabling partners to optimize usage and improve the user experience. DCGO’s proprietary technology also improves fleet deployment and utilization, which in turn leads to lower idle times and higher profits.

Sept 2022 presentation

Partnership model that increases the overall value of the eco-system

DCGO’s long-term partnership model with several of its most valuable healthcare provider clients involves a shared economic stake for both parties. I think this setup is brilliant because it offers substantial incentives for all parties involved. The improved quality of patient care is a direct result of this organizational structure’s facilitation of more consistent service to the provider and its patients.

On the other hand, DCGO stands to gain economically from this setup. DCGO is able to rely on the transportation revenue generated through these partnerships to be steady and reliable in the areas where the partners operate. Through the partnership, DCGO will be designated as the preferred provider and will receive a larger portion of the unit economics that would have been allocated to other companies. I believe there is an opportunity for cross-selling DCGO Mobile Health solutions as a result of this strong relationship.

DCGO’s partners not only benefit from the cost savings and additional revenue streams that come with expanding the partnership, but also from the economic efficiency of DCGO’s advanced technology. Essentially, DCGO’s unique approach transforms medical transportation from a financial burden into a commercial opportunity for its partners.

Sept 2022 presentation

Nationwide presence

DCGO’s national presence is indicative of the success of network development and presents opportunities to capitalize on this foundation in order to fuel its expansion. DCGO currently has over 4,000 employees in the medical field and operates a fleet of state-of-the-art vehicles across 29 states.

This nationwide presence coupled with the brilliant partnership model works like magic, in my opinion. DCGO’s partnership business model is unique, and its solutions are easily scalable to meet the needs of much larger volumes. This bodes well for the company’s ability to grow quickly without taking on excessive financial or operational risk.

Sept 2022 presentation

3Q22 earnings beat and raise is a good indicator of momentum

In September 2022, contracts for Covid screenings expired and were replaced by more extensive mobile health contracts. This successful transition has undermined the negative outlook previously held for the company, as DCGO has exceeded top line expectations and raised projections for the fiscal year 2022. Importantly, commentaries indicate that the company is expected to continue this beat-and-raise trend in FY23. The sudden departure of CEO has raised some concerns, but I have confidence in the company’s plan for transition and anticipate significant growth in the fiscal year 2023.

Also, management raised FY22 revenue guidance from $425 million to $435 million (33%-36% growth) to $430 million to $440 million (35%-38% growth). Strong demand for mobile health services is primarily responsible for the organic growth, while additional M&A activity also contributed to the rise. It’s also important to note that the guidance doesn’t take into account a flu season in 4Q22, which could have disastrous consequences if the United States experiences a severe flu season. Management assumed that revenues from mobile health and transportation would rise during the flu season.

Valuation

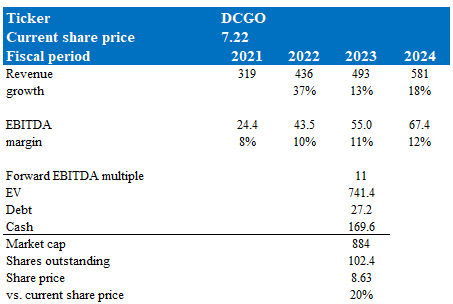

My model suggests DCGO is worth $8.63, if it trades at 11x forward EBITDA multiple in FY23.

Model walkthrough:

- Revenue to follow management full year guidance in FY22, but will face a deceleration in growth in FY23 due to a higher base (pulled forward demand from covid and acquisitions). Revenue should accelerate back to higher growth as it lapses the high base and continue to capture share in FY24

- EBITDA margin should continue to expand as DCGO scales off its fixed cost base and leverage of partners to grow

- DCGO is still trading within its historical valuation range (about 3x off its average). Until such time where DCGO starts showing actual results that growth is accelerating and margins are improving, I believe the valuation would stay at this level for the time being. This is alright as we are not really betting on any positive valuation re-rating to hit my expected upside.

Own calculations

Risk

License could be a regulatory overhang

DCGO may change its expansion strategy and rely more on acquisitions to meet the needs of its partners if the licensing process is delayed. In the short term, the change could increase operating expenses, and in the long term, it could reduce the company’s ability to generate free cash flow.

Conclusion

DCGO is worth more than what it is worth today. More and more people are turning to telehealth for a variety of care needs, but as this field grows, so does the need for supplementary in-person procedures to fill the gaps that telehealth cannot address. DCGO provides this final segment of care with its specialized platform and offerings.

Be the first to comment