Oselote

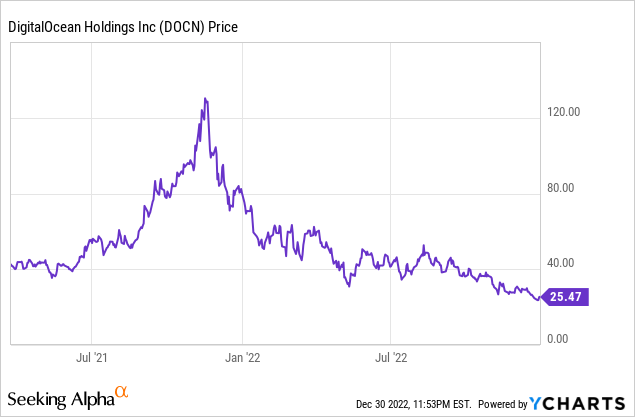

DigitalOcean Holdings (NYSE:DOCN) has taken a beating this year, down 68.29%. I started following this business since its 2021 IPO at $47 a share, but the valuation was always too high for me. The market mania of 2021 took this stock into the stratosphere, and it has since crashed back down to Earth. The valuation looks much more reasonable at current levels.

This is a fantastic business, but management has made some unwise financial decisions during their time as a public company. Even so, I believe that DigitalOcean is a buy at these levels, but prospective buyers must understand the risks involved.

Company Overview

For those unfamiliar with DigitalOcean, they are a cloud computing platform that provides Infrastructure as a Service (IaaS) to businesses and individuals. They offer a range of services including virtual private servers (VPS), storage, networking, and security.

DigitalOcean allows users to create and manage virtual servers, called “Droplets,” in the cloud. These customers can choose from a variety of operating systems, including Linux and Windows, and can also select the desired specifications for their Droplets, such as the amount of memory and CPU. They also provide a range of tools and resources to help users manage their infrastructure and applications, including a control panel, API, and command-line interface.

In addition to their virtual server offerings DigitalOcean also provides a range of other cloud computing services, including managed databases, object storage, and load balancers. These services can be used to build, deploy, and scale applications in the cloud.

DigitalOcean has been focusing on building out their developer and SMB cloud. This includes managed Kubernetes, managed databases, marketplace/app platform, functions, and managed hosting.

Thesis

Many legacy businesses are increasing their budgets for cloud computing and are in the process of transitioning their on-prem systems to the cloud. According to Grand View Research, the global cloud computing market is expected to reach $1,554.94 billion by 2030, which equates to a CAGR of 14.8%.

DigitalOcean is uniquely positioned to capitalize on this industry growth for three reasons:

- DigitalOcean is focused on catering to established SMBs and startups. This focus helps them build an identifiable brand and spend money efficiently.

- DigitalOcean has differentiated themselves from competitors through their commitment to simplicity and ease of use.

- DigitalOcean’s customers don’t have to worry about funding a competitor, which gives them peace of mind.

Organizational Focus

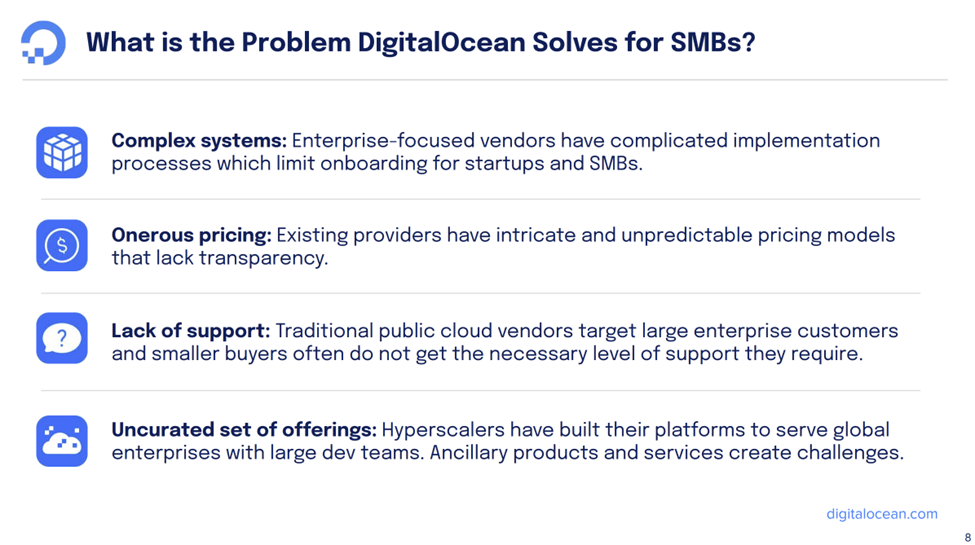

DigitalOcean primarily serves established SMBs and startups. These types of businesses have different needs than larger firms and may not have experienced IT staff. The large cloud providers such as AWS and Microsoft Azure are focused on keeping their large corporate customers happy and may not give much attention to their smaller customers. While the SMB cohort might not have a gigantic budget, DigitalOcean can focus solely on solving problems that these customers face and give them attention and support. This specialization helps DigitalOcean spend money efficiently and brand itself as a niche player. Their goal is to become the go-to solution for SMBs and startups that are looking for a low-cost, simple, and transparent cloud computing solution. Digital Ocean can grow with their customers and expand ARPU by adding more services once enough customers need them.

Slide from DigitalOcean’s 2022 Q3 Earnings Presentation (DigitalOcean)

Differentiated Value Proposition

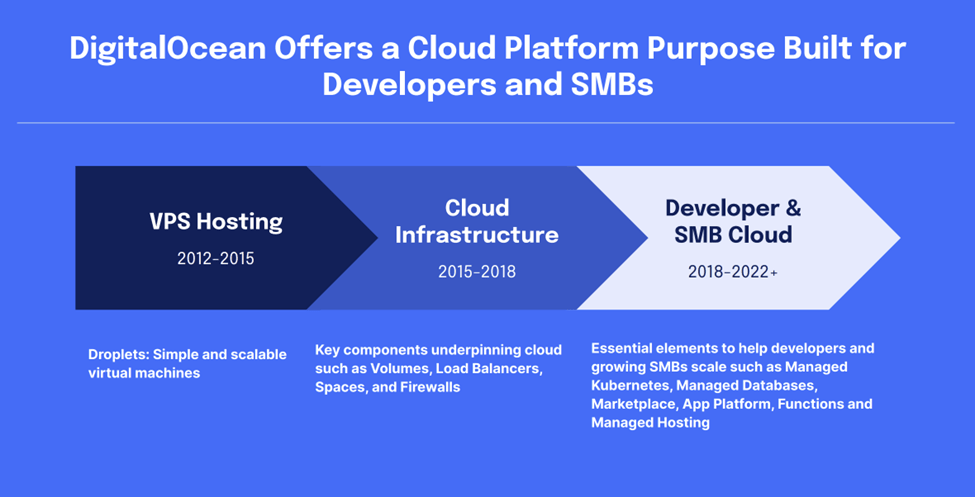

DigitalOcean’s mission statement is “DigitalOcean simplifies cloud computing so builders can spend more time creating software that changes the world.” This pure focus on simplicity and ease of use allows them to deliver to their customers exactly what they want while keeping costs low. Customers understand that DigitalOcean will not have some services that the hyperscalers have, but they choose to use them anyways because they either don’t need the missing services or prefer a simple and easy to use solution. DigitalOcean is continually adding new services and building them from the ground up with a focus on their core values of simplicity and ease of use.

DigitalOcean’s Q3 Earnings Presentation

DigitalOcean’s Q3 Earnings Presentation

Customer Peace of Mind

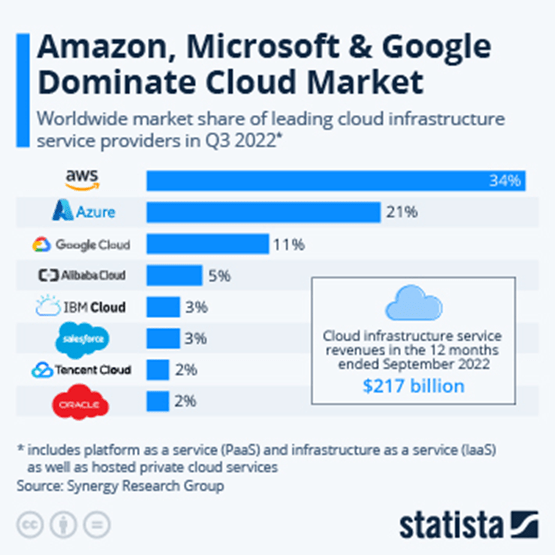

Many companies in the cloud computing industry also have other business segments. Taking a look at the top companies in the industry by market share we can see that none of them are pure-play vendors.

Cloud Vendors by Market Share (Statista)

Users of the cloud probably don’t want to fund their competitors, and it isn’t as simple as a retailer choosing Google Cloud over AWS because they don’t want to fund Amazon’s retail business. Even if Google isn’t a current competitor, due to their size and willingness to expand into other business segments they could become a competitor later. When a customer uses DigitalOcean they know that they won’t be funding a current or future competitor. Some owners of SMBs and startups might also just dislike “big tech” and want to work with a smaller player. Some startups might not want to give big tech companies insight into their operations. While the number of businesses that choose their cloud provider this way are limited, every customer is a big deal. This is especially true for a smaller competitor in the segment. Any way to differentiate and create more value is a positive.

Execution

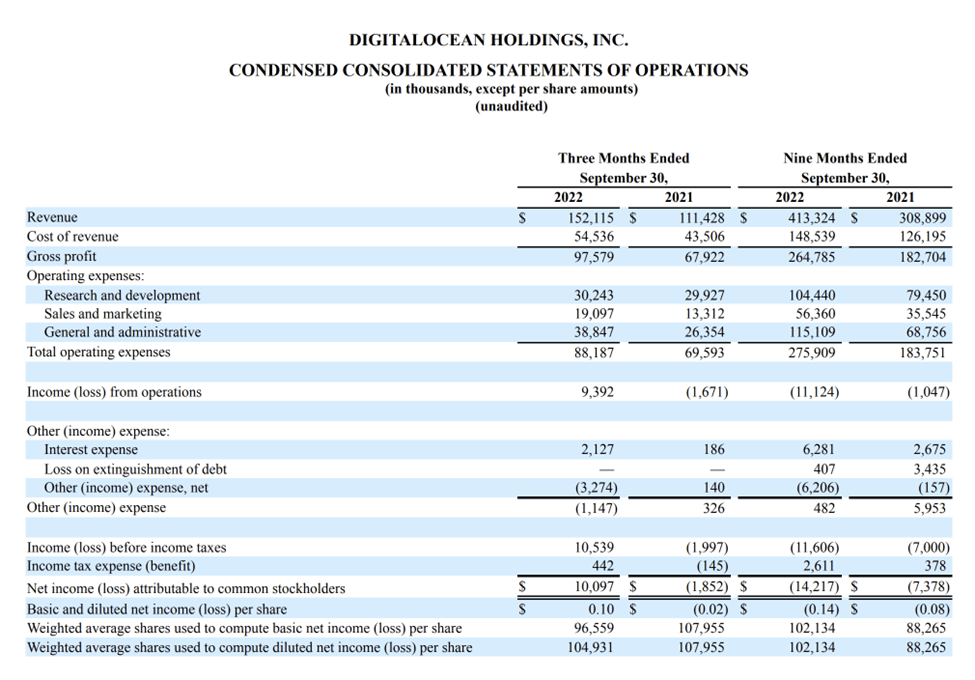

Examining DigitalOcean’s Q3 report there is a lot to like.

DigitalOcean’s Q3 Earnings Report

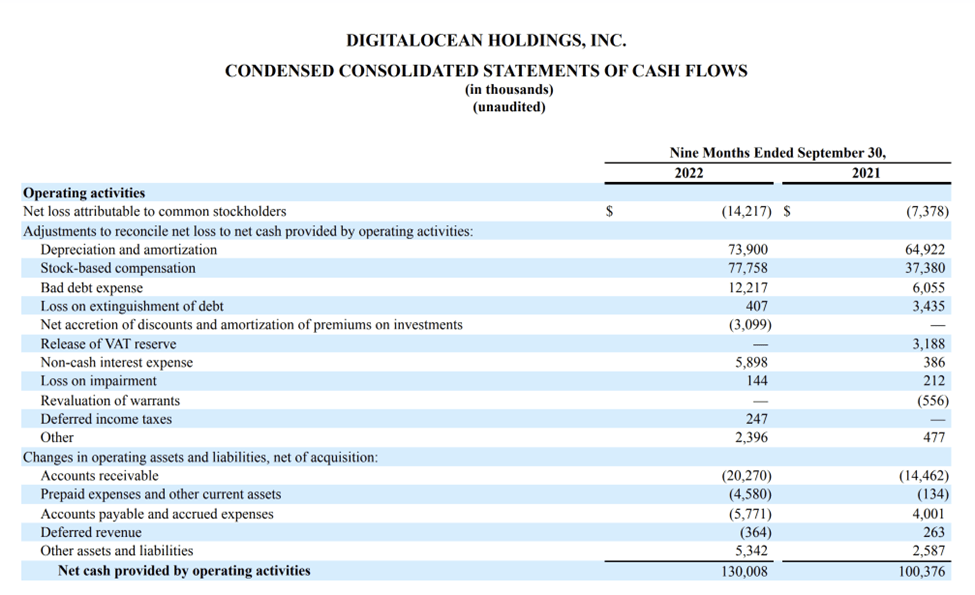

They were able to grow revenue 37% year on year while keeping expenses under control, something that many companies have struggled with in this environment. This helped them to become profitable on a GAAP basis compared with the year-ago period, which shows they are beginning to realize the potential operating leverage in their model. When looking at the cashflows there is even more to like, with DigitalOcean generating around $130 million in operating cashflows over the past nine months.

DigitalOcean’s Q3 Earnings Report

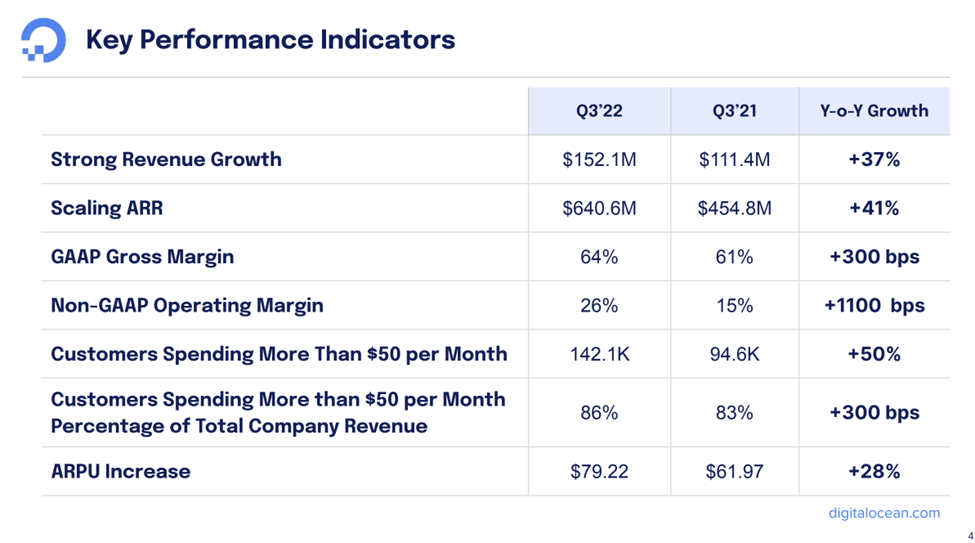

DigitalOcean provides some insightful presentation materials to go along with their earnings and investor days and I encourage everyone to take a closer look at them. When looking at the Q3 KPIs we can see the company is continuing to execute and improve in their financial areas of focus.

DigitalOcean’s Q3 Earnings Presentation

It’s important to note that part of the year-over-year growth in ARPU was due to a price change, which you can read about here. In an ideal scenario ARPU would be increasing because of customers using more of the same service or expanding the types of services they use. In the end, this is a small criticism of an otherwise strong report.

DigitalOcean is executing well on their strategy so far, but it remains to be seen if they can continue to do so.

Additional Points

Looking at the cloud market share graphic referenced earlier, it is painfully clear that Google, Microsoft, and Amazon have a vice grip on the competition. If a smaller player such as IBM, Salesforce, or Oracle wants to increase their market share they need to take drastic steps to improve their competitive positioning. A benefit of owning DigitalOcean is the potential upside of getting acquired. A free cashflow generative business that is a pure play in a quickly growing sector with multiple companies looking to gain market share is a ripe acquisition candidate. While DigitalOcean doesn’t need to be acquired to deliver value to shareholders, the optionality is nice and provides somewhat of a floor on the share price. Some potential acquirers are Oracle, IBM, Salesforce, Cisco, and any other tech company that wants to make a splash in cloud computing.

Digital Ocean’s moat is derived from counter-positioning against hyperscalers and high switching costs. The way to build a moat in this industry is to either be lower cost or different. There is no way that DigitalOcean can compete in cost with the hyperscalers, so from my point of view they have chosen the correct strategy by differentiating themselves and relying on high switching costs keeping their customers in the ecosystem. Their moat isn’t the strongest, but it does exist.

Valuation

DigitalOcean looks like a buy from both a PE basis and a cashflow basis. As a pure play in the cloud space, the market will likely be willing to give them a premium valuation, and it certainly has done so in the past.

DigitalOcean’s management is targeting $1 billion in revenue and 20% FCF margins in 2024. The current diluted market cap is $2.67 billion, so $200 million of FCF values the company at a multiple of 13.36x 2024 FCF. I think this business can trade at 30x FCF in a risk-tolerant environment, especially as a pure play with a sustainable growth rate of over 20% for at least the next few years. 30x 2024 FCF puts the share price at $57.18.

On a PE basis the stock is trading at 21.92x 2023 earnings and 15.16x 2024 earnings. This is around a market multiple, however DigitalOcean is growing much faster than the general market and is in a sector highly valued by investors. We believe that in a risk-on environment DigitalOcean can easily trade at 35x earnings, which puts the share price at $40.60 and $58.80 based on 2023 and 2024 estimates.

Keep in mind that Google’s Cloud unit is still GAAP unprofitable and is growing revenue around the same pace as DigitalOcean is. Many investors in the sector are not expecting near term profitability and may reward a GAAP profitable pure-play company with a much higher multiple than 35 times earnings, especially if DigitalOcean can keep growing revenue at a rate of over 20%.

In this case we have chosen the relatively simple option and our estimated fair value for DigitalOcean is $40.60 (35x 2023 earnings). This assumes that the market becomes more comfortable with risk in 2023, and that DigitalOcean continues to execute well on their long-term plans.

Before making an investment, it’s important for investors to understand what can go wrong. Here are some risks/threats/negatives that investors should be aware of.

Competition from Hyperscalers

The ever-present threat to DigitalOcean are Amazon, Microsoft, and Google. It is unlikely that any of them would be able to buy DigitalOcean because of regulatory scrutiny, so if the SMB cloud market ever became valuable enough the big three would look to crush them. While this threat is very real, by the time DigitalOcean is viewed as a threat by the larger players there will have likely been strong financial returns provided to shareholders, especially from these levels. So while this risk is very real, from an investors point of view there are more immediate concerns such as the debt.

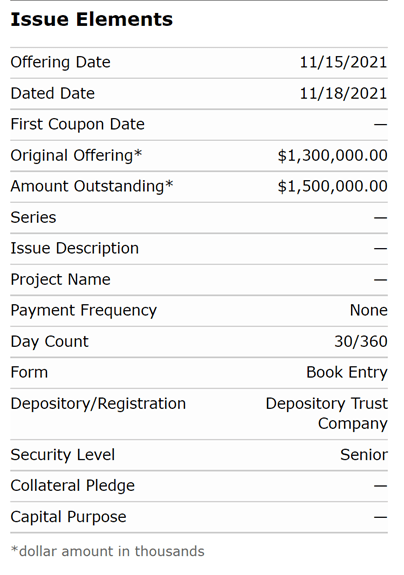

Debt Overhang

In November of 2021 Digital Ocean issued a convertible bond worth $1.3 billion with the option for the bond investors to purchase another $200 million, which they ended up doing. This debt bears no interest, has a convert price of $178.51 a share and last traded around 72 cents on the dollar. This discount is important to note because even though rates have gone up since the debt was issued and the share price is down, this wide of a discount shows that bond investors believe DigitalOcean may have difficulty making the repayment.

FINRA Bond Search

FINRA Bond Search

They used $600 million of the proceeds to buy back stock and $350 million to acquire Cloudways.

The buybacks were executed at an average price of $44.03 a share. It’s easy to say that this move was a bad idea in hindsight, but it was also clearly a bad idea in the moment. Management apparently had a burning desire to use the cash and didn’t want to let it sit on the balance sheet. In an industry that has so much growth potential and competition, additional acquisitions or capex would have been far more beneficial in the long term than share buybacks, even if the buybacks were done at a better price. In such an uncertain macro environment there is also an argument to be made that cash should remain on the sidelines just in case things get ugly. I think it’s fair to say that executing such a large and quick buyback in a tough macro environment and with a sizeable debt load maturing in 2026 amounts to short sighted financial decision making by DigitalOcean’s management. It’s likely that much of the short-term free cash flow will go to paying down this debt, and if it needs to be refinanced it will probably be done at a rate that is less than ideal. This debt is a stain on the fundamental thesis and will be a strain on cashflows for at least the next couple of years.

Customers Outgrowing DigitalOcean

A concern is that customers outgrow DigitalOcean as they grow larger and migrate to a different service provider. While this will undoubtably happen on some scale, Digital Ocean is working to add more services over time with a core focus on simplicity and ease of use. This focus on adding more services combined with the high switching costs will ideally be enough to stop most of their larger customers from leaving over the long term. The good news is that they have a wide customer base, and many of their customers will not need the most cutting-edge solutions.

Lease Concerns

DigitalOcean operates data centers around the world but does not own them outright. They lease space from third-party landlords and invest in technology to make improvements.

DigitalOcean’s Q3 Report DigitalOcean’s Q3 Report

This isn’t so much of current problem as it is a potential one. Once these data center leases are up for renewal, the third parties could squeeze DigitalOcean for higher payments or lease to someone else. This could end up being a drag on margins and introduces a mild amount of business risk.

Cashflow Obligations

Free cashflow will be hampered in the short term by debt repayments, capex, and acquisitions. This is important for investors that are valuing the business on free cashflow, as positive operating cashflow may not translate to cashflows available to equity holders for many years. This is a FCFF vs FCFE debate, so not all investors will care about this.

Conclusion

Overall, we view DigitalOcean as a buy and have a fair value estimate of $40.60 (35x 2023 earnings), which implies 59.40% upside from these levels. The company has the potential to meaningfully exceed expectations over the coming years, and the market may be willing to give them a much higher multiple than we expect. The attractiveness of DigitalOcean to potential acquirers somewhat limits the potential downside for the share price. If investors are comfortable with the risks involved, DigitalOcean can give value focused investors exposure to a sector that has traditionally been expensive on a fundamental basis.

Be the first to comment