piranka

Over the last couple months, I have taken advantage of opportunities created by the selloff in several REIT sectors to start new positions. This includes the industrial REIT Terreno Realty (TRNO) and self-storage REITs National Storage Affiliates (NSA) and CubeSmart (CUBE). One of the sectors I have avoided is the data center sector, which has also seen a significant selloff. I think there are several important questions investors have to answer for themselves. I decided to focus on other opportunities that look more attractive to me, but that doesn’t mean investors should avoid data centers altogether.

Investment Thesis

Many investments had a rough 2022 but shares of Digital Realty (NYSE:DLR) took it on the chin with a decline of more than 40% from the peak. I have been watching from the sidelines, but in 2022 there has been an interesting back and forth between bulls and bears on the data center REIT sector. Bulls point to the cheaper valuation (a price/FFO just over 15x) and a 4.8% yield, while bears, including Jim Chanos, are skeptical that the REITs will be able to perform well with rising costs while competing with major customers. Income investors might be drawn in by the yield approaching 5% and a track record of increases, but I think investors should consider the risks seriously before buying shares or adding to a position. In my opinion, shares of Digital Realty are near fair value today, but I plan to keep an eye on the sector as things progress over the next couple years.

DLR Overview & 10-Q

Digital Realty has an international portfolio of assets and a market cap just under $30B. Approximately two thirds of the portfolio is based in the US (with a heavy 19% concentration on Northern Virginia due to government demand), with rest coming from international exposure, primarily Europe. They also have significant square footage under development, especially in Europe. I wouldn’t be surprised to see the European segment account for a larger portion of revenues in a couple years as these projects finish.

Scanning Digital Realty’s most recent quarterly report is another reason I chose other REIT sectors. Revenue growth, which has been impressive for data center REITs in the past, has been minimal for Digital Realty compared to 2021. FFO/share has also been basically flat in 2022, another reason for caution. One thing that I like about the company’s balance sheet is their low interest rates on borrowing. Most of the debt is fixed rate, and they have an effective interest rate of 2.33%.

While this isn’t a pure play data center REIT, American Tower (AMT) does have some exposure to the data center space after their CoreSite acquisition. However, their data center portfolio only accounts for about 10% of their revenues if I’m remembering correctly, so the vast majority of their revenues comes from cell towers, an investment I view as more attractive today. One of the other things that caught my attention on the data center sector in 2022 was the fact that notorious short seller Jim Chanos of Enron fame has been short the data center REITs, including Digital Realty and Equinix (EQIX).

Jim Chanos & The Bears

Some analysts and investors have pushed back against Chanos’ bearish thesis, but there are points that he makes that are hard to dispute. His biggest concern with the data centers is that they are set to compete against their biggest customers over the next decade, including Amazon (AMZN), Microsoft (MSFT), and Google (GOOG) (GOOGL).

Their three biggest customers are becoming their biggest competitors. And when your biggest competitors are three of the most vicious competitors in the world then you have a problem.

Bulls expect that these major cloud companies will continue to outsource most of their demand for the foreseeable future due to tight supply and long lead times for building new facilities. They also expect the REITs to be able to pass on most of their rising costs with rising rents, but I would also weigh some of the other points made by bearish investors and analysts.

Morgan Stanley (MS) analysts have similar concerns to Chanos, and point to rising costs and low returns on capital. They think that the REITs might not be able to offset these costs by increasing rents and also see the risk of the cloud giants slowing their investments in cloud capacity in 2023. While I’m an interested observer from the sidelines, I’m curious to see how things play out for the sector in coming years. One thing that bulls point to today is a more attractive valuation due to the large selloff in the sector.

Valuation

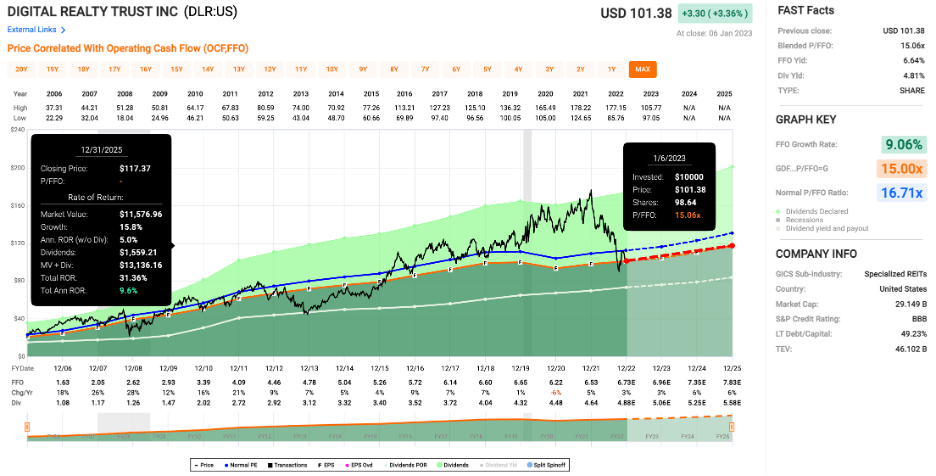

Shares of Digital Realty have taken a steep nosedive since the end of 2021. Shares peaked above $170 with a price/FFO over 27x, where the valuation was far too rich in my opinion (feel free to take this with a grain of salt, hindsight is 20/20). Over the last fifteen years, shares have an average multiple of 16.7x, so most of the selloff was just mean reversion to a better valuation. It was also driven by a selloff in broader markets, but the valuation is more attractive today than it was twelve months ago. Shares now sit just above a price/FFO of 15x, which is more or less fair value in my opinion.

Price/FFO (fastgraphs.com)

With shares down over 40% since the peak, many contributors have turned bullish on Digital Realty. While the cheaper valuation today has set up better forward returns for investors compared to a year ago, I’m still cautious on the REIT overall. I’m no technological genius, but on a conceptual level, I do think the risk of increased competition from the big guys with deep pockets is one that investors should take seriously. Another thing that bulls point to in combination with the cheaper valuation is the 4.8% dividend.

The Dividend

While the yield on Digital Realty briefly touched 7% in 2013, it has pretty consistently traded in the 3-4% yield range in recent years. The yield approaching 5% is near recent highs compared to the last five years. With that yield and the fact that Digital Realty is due for another dividend hike, many investors view the selloff as a buying opportunity. Digital Realty does have a long track record of solid dividend growth, with 17 consecutive years of increases. With the relatively slow FFO/share growth, I’m expecting the dividend growth will be a bit slower moving forward, but the 4.8% yield combined with the dividend growth history is bound to attract income investors.

Conclusion

Data center REITs have been one of the best performing REIT sectors over the last decade as tailwinds from increased demand drove impressive growth. That changed in 2022 as rich valuations and a risk off market caught up to the sector. Many investors are bullish on Digital Realty after the large selloff, which has brought the valuation down to a price/FFO just over 15x and put the yield at 4.8%. However, there are bears out there, including prominent short seller Jim Chanos.

He points out some of the risks, including increased competition from the large cloud companies like Amazon, Microsoft, and Google, as well as rising costs and potential obsolescence risk. I think shares are trading near fair value today, but I would encourage bullish investors to take some time to consider some things that could poke holes in their investment thesis. Either way, I’m just an interested observer, but as someone who spends a fair amount of time analyzing REITs, I will be watching the sector to see how things go over the next couple years.

Be the first to comment