Mina De La O/DigitalVision via Getty Images

It’s simply hard to find a sleep well at night type of stock that gives a meaningful yield, has strong dividend growth and is priced in value range. Yet, these opportunities exist, especially in today’s market, when even high quality companies have seemingly been thrown out with the bathwater.

Such I find the case to be with Digital Realty Trust (NYSE:DLR.PK), which has dropped by an eye-opening 42% over the past 12 months. In this article, I highlight what makes DLR an excellent choice for value and income investors alike.

DLR Stock (Seeking Alpha)

Why DLR?

Digital Realty is the largest global provider of cloud and carrier-neutral data center, colocation, and interconnection solutions. Its international footprint spans across 300+ facilities in over 50 metro areas on 6 continents. This gives DLR the benefits from the so-called “network effect”, as its size and scope enables it to offer its tenants a full array of solutions and connection needs. Its top tenants include Meta Platforms (META), Oracle (ORCL), and Microsoft (MSFT).

One of the reasons for why data center REITs such as DLR have declined in value is due to perceived risks and competition from hyperscale tenants such as Amazon (AMZN), Google (GOOG) (GOOGL), and Microsoft. In fact, some short sellers have argued that value is accruing to the aforementioned cloud companies rather than brick and mortar data centers, with the biggest customers also becoming the biggest competitors.

There are flaws, however, to that short thesis, as the data center space is far from being a zero-sum game. Fellow marketplace contributor Hoya Capital de-bunked the short-thesis in a recent article as follows:

Chanos’ short thesis received significant pushback from data center REITs and the majority of the data center industry’s sell-side analysts, who point out that while Chanos accurately characterizes the overall competitive dynamics over the past five years, the degree to which the cloud is a “zero-sum” game is overstated.

In fact, the pricing power of these data center REITs has meaningfully strengthened in recent quarters as strong absorption and moderating supply growth have sent vacancy rates towards record lows and has started tilting the negotiating leverage back towards the landlords for the first time before the pandemic.

CBRE reported that “demand for capacity more than tripled year-over-year in H1 2022 as companies continued to shift toward hybrid cloud environments… but developers can barely keep up with demand. Among primary markets, almost 75% of under-construction capacity in H1 was already released. Vacancy rates fell in all seven primary markets.”

Meanwhile, Digital Realty doesn’t appear to be slowing down, as revenue grew by 5% YoY to $1.2 billion during the third quarter. Additionally, revenue should continue to grow in the coming quarters, as DLR delivered record quarterly bookings, signing deals that’s expected to generate $176 million of annualized GAAP rental revenue. As a point of reference, this translates to 3.7% revenue growth down the line for DLR.

Looking forward, DLR has plenty of growth runway in the co-location and interconnection business, which is a strong value add to DLR’s customer base. DLR is also one of just a handful of players that can effectively provide these services at scale, due to its worldwide presence and network effect.

This interconnection capability can be a game changes, as it leads to potential for internet of things and artificial intelligence functions. DLR continues to expand this capability, generating strong double-digit returns, as highlighted by management during the recent conference call:

We recently acquired land on the Greek island of Crete to create an interconnection hub in the Eastern Mediterranean to complement our existing hub in Marseille, along with developing hubs in Barcelona and Israel, which will feed additional traffic into Greece, the Balkans, Turkey and Northern Africa. We expect that this highly differentiated project will generate strong double-digit returns while enhancing the value of our existing facilities in the region.

Meanwhile, DLR carries a strong BBB rated balance sheet with a net debt to adjusted EBITDA of 6.4x. While this leverage ratio is slightly higher than the 6.0x level that I prefer to see, it’s not concerning considering the growing nature of the enterprise and the steady nature of its recurring revenues. Moreover, DLR has no issues covering its obligations, as it carries a fixed charge coverage ratio of 5.7x, and has just 17% exposure to floating rate debt.

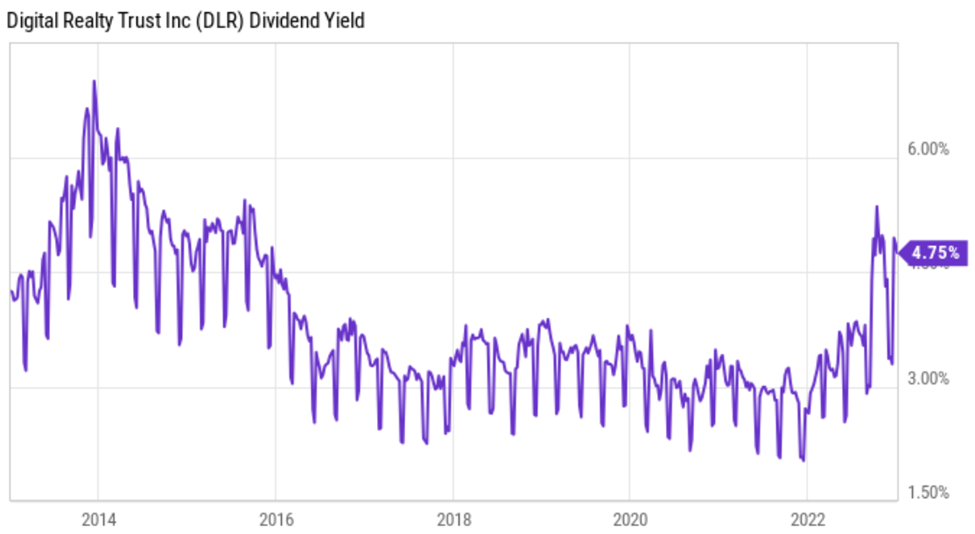

Plus, DLR’s current 4.7% dividend yield sits at one of its highest levels over the past decade. The dividend is well-protected by a 73% payout ratio, based on Q3 Core FFO per share of $1.67. Management has also grown the dividend more or less in line with its long-term growth rate, with a 5-year CAGR of 5.6% and 17 years of consecutive growth.

DLR Dividend Yield (YCharts)

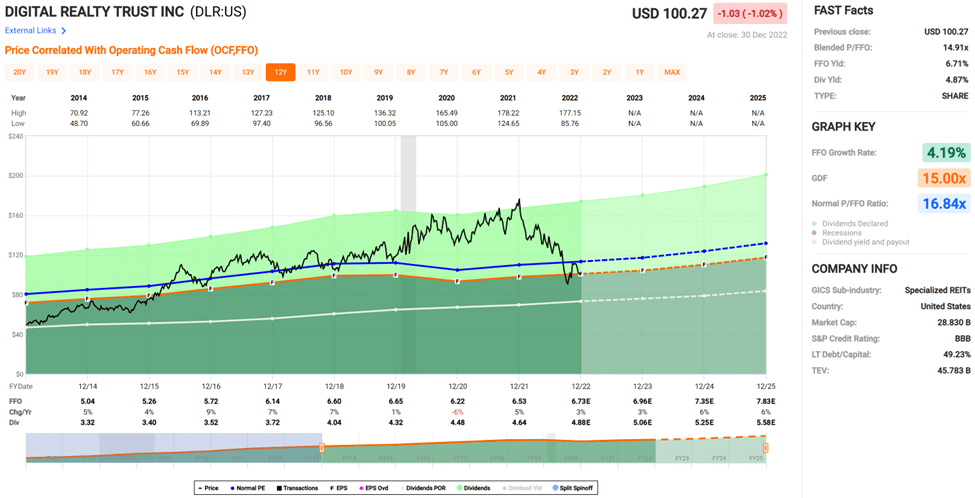

Lastly, I see value in the stock at the current price of $102.77 with a forward P/FFO of 15.3, sitting below its normal P/FFO of 16.8 over the past decade. Analysts have a consensus Buy rating on the stock with an average price target of $125, equating to potentially strong double digit total returns.

DLR Valuation (FAST Graphs)

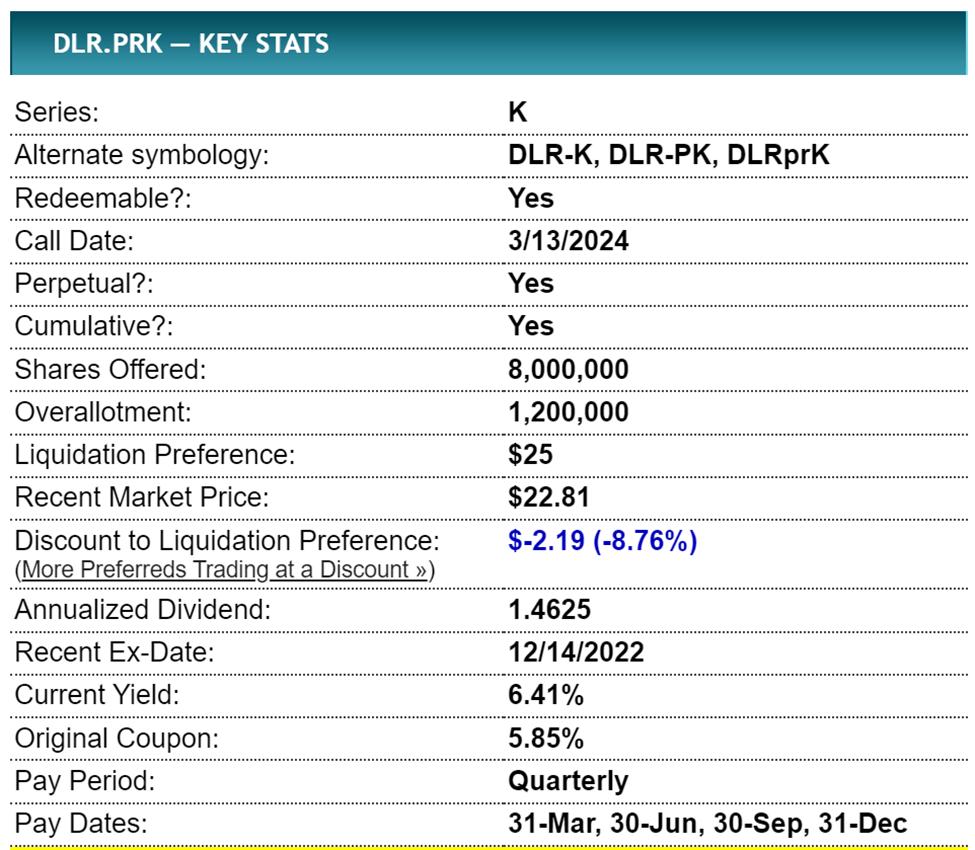

For those investors seeking a higher dividend stream, Digital Realty’s Preferred Series K (NYSE:DLR.PK) can be considered. Its call date is not until March of 2024, and it’s unlikely it will be called at that time should interest rates remain high. For reference, the Series J had a call date in August of 2022 and is still on the market. DLR.PK currently sports a 6.4% dividend yield, which may be appealing for those seeking higher immediate income.

DLR Preferred Series K (Preferred Stock Channel)

Investor Takeaway

Digital Realty’s share price is down materially over the past year. Yet, its business isn’t showing signs of slowing down, and it has a strong future ahead with interconnectivity and co-location services. Meanwhile, it pays a respectable dividend yield and has a strong balance sheet. The current below-normal valuation presents an attractive buying opportunity for value and income growth investors alike.

Be the first to comment