Umnat Seebuaphan/iStock via Getty Images

Digi International Inc. (NASDAQ:DGII), which provides business and services in the Internet of Things sector, is coming off another solid quarter. Even though the tech sector has been under pressure, DGII has defied the odds and continues to grow its business even in the midst of supply constraints and tough economic conditions.

The share price of the company has jumped since hitting its 52-week low of $18.54 on April 27, 2022, and has since more than doubled, to trade at over $41.00 per share as I write.

TradingView

That’s impressive when considering it has been breaking company records in several of its metrics while leaving “tens of millions” on the table as a result of supply constraints.

In this article we’ll look at its latest earnings numbers, its share price movement over the last year, how it’s responding to supply chain issues, and what the next year looks like for the company.

Recent numbers

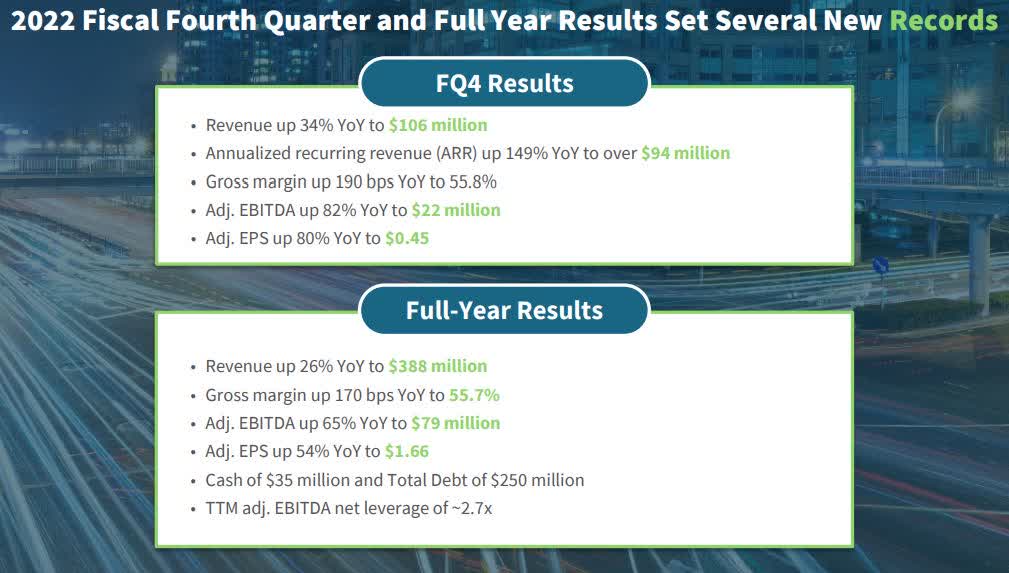

Revenue in the fourth fiscal quarter was $106 million, up 34 percent year-over-year. Full-year revenue was $388 million, a gain of 25 percent.

Gross profit margin in the reporting period was $55.8 percent compared to 53.8 percent last year in the same quarter. Excluding amortization, gross profit margin was 57 percent compared to 55.4 percent year-over-year.

Net income per share was $0.31, up 138 percent from the net income per share of $0.13 last year in the fourth fiscal quarter. Adjusted earnings per share was $0.45 per share, up 80 percent from the same quarter of 2021.

Company Presentation

Breaking down the segment results

IoT Product & Services: In its IoT Product & Services segment, DGII generated revenue of $81 million, up 15 percent year-over-year. That was attributed to growth in its “OEM and console server business units.” Gross profit margin was 53.7 percent of revenues, essentially flat in comparison to the same quarter of 2021. A significant part of that was from supply chain constraints and inflation, as well as customer and product mix.

Management said gross profit margin will probably remain flat in 2023 based upon supply chain issues.

For full-year 2022, revenue in the segment reached a company record of $298 million, up 13 percent from last year in the same reporting period. An increase in sales of console servers and cellular products were the reasons given for the strong performance.

Gross profit margin for the year fell to 53.8 percent, or 90 basis points, for the same reasons mentioned above for the quarter.

IoT Solutions: Revenues in the fourth fiscal quarter for IoT Solutions was $25 million, up 173 percent from last year, which was primarily from the acquisition of Ventus.

ARR in the quarter was $80 million, and gross profit margin jumped to 62.7 percent, or 710 basis points, from growth in its subscription revenue in the reporting period.

Full-year revenue in the segment was $91 million, up 104 percent, again, for the most part driven by the acquisition of Ventus. Gross profit margin in the quarter was 62.0 percent, up 1,210 basis points from a favorable mix associated with recurring revenue.

Supply chain constraints

It’s nothing new to report that supply constraints in the tech sector remain a challenge. The reason I’m focusing on it in regard to DGII is because of the potential it offers for future growth as the company works on acquiring more parts to serve its customers.

CEO Ron Konezny said in the earnings call that the company was “leaving tens of millions of dollars on the table” because of lack of supply. He also noted that demand isn’t an issue for the company, but supply is the major challenge.

This is the major reason it has a huge backlog of $300 million at this time. While this is an obvious headwind for the short-term performance of the company, as the firm heads into 2023, it should be able to work through a lot of that backlog, so what 2022 took away from it, 2023, should at least in part, give back to it.

So, if demand continues to climb and the supply chain improves, it could end up being a strong catalyst for DGII next year.

Among the three major priorities of the company in 2023, one of them is building up more inventory in order to ensure available parts for its customers. The other two are paying down debt in order to shrink the amount of capital used in the current high interest rate environment and continuing to work on integrating Ventus.

Conclusion

DGII has been performing strong in a high interest rate environment that doesn’t usually favor tech companies. But with demand for its products high and a backlog of approximately $300 million, the company is heading into 2023 with some nice tailwinds at its back.

While I’m getting a little cautious because of how quickly and consistently the share price of DGII has jumped, I think over the next year or two the company is going to maintain its growth momentum, even though it could come under pressure in the near term if investors start taking profits.

With the company guiding for revenue growth of 20 percent to 25 percent in the first fiscal quarter, and gross profit margin to remain flat, it does point to continual improvement with the visibility we have today. For the full year, the company sees growth for fiscal 2023 to be about 10 percent, meaning the second half could be slowing down if it can’t fix its supply chain issues.

So how I see it is, the company will probably maintain momentum in the first couple of quarters of fiscal 2023, with the second half slowing down some. Since there is the possibility of the stock correcting because of its recent surge, it could be best to wait for a pullback if considering taking a position in the company, as a lot of its performance appears to be priced in.

If some of the supply constraints are worked out better than expected in the year ahead, DGII is likely to surprise on the upside and deliver better-than-expected numbers.

Be the first to comment