mammuth/E+ via Getty Images

Tough times ahead

Airbnb (NASDAQ:ABNB) pioneered the online short-term rental market and became the household name in the space. Although the business itself is in a great position, with good management and cost discipline, I believe that the company over earned and many tailwinds of the last year are now becoming a headwind. Free Cash Flows exploded over the last year driving valuation multiples down, but multiples only get you that far, what matters is the future performance of the business and I have my doubts that over the short term the performance is sustainable for Airbnb.

TAM

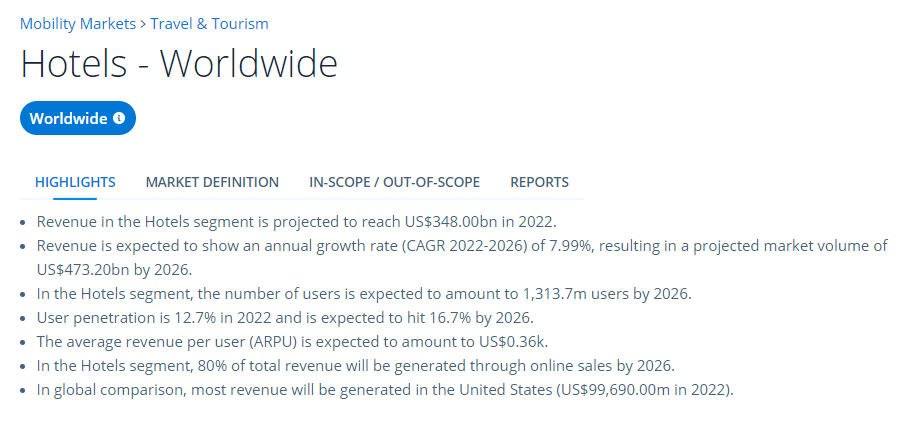

Airbnb estimated its total addressable market (“TAM”) at a gigantic $3.4 trillion, consisting of $1.8t short-term stays, $210b long-term stays and $1.4t experiences. This sounds quite excessive if we take a look at forecasts from Statista regarding the global hotel market: We can see that in 2022 the market is projected to reach $348 billion and to grow to $473 billion, an 8% CAGR, in 2026. I do not understand where this massive $1.5 trillion market besides hotels should come from. Regardless of the exact numbers, there is a lot of runway for growth available for Airbnb, I just don’t like if companies use these excessively inflated TAM estimates.

Hotels – Worldwide statistics (Statista)

Large European exposure

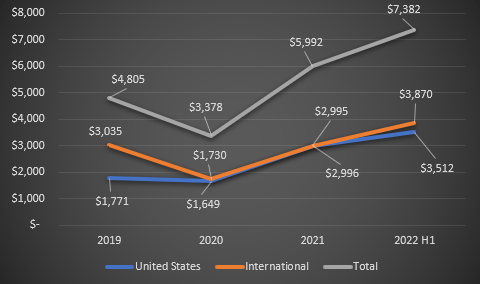

Airbnb only discloses revenues from two regions: the United States and International. We can see that since 2020 both segments have been of around equal size, with International pulling ahead in the first half of 2022.

Airbnb revenue by segment (authors model, Airbnb 10k)

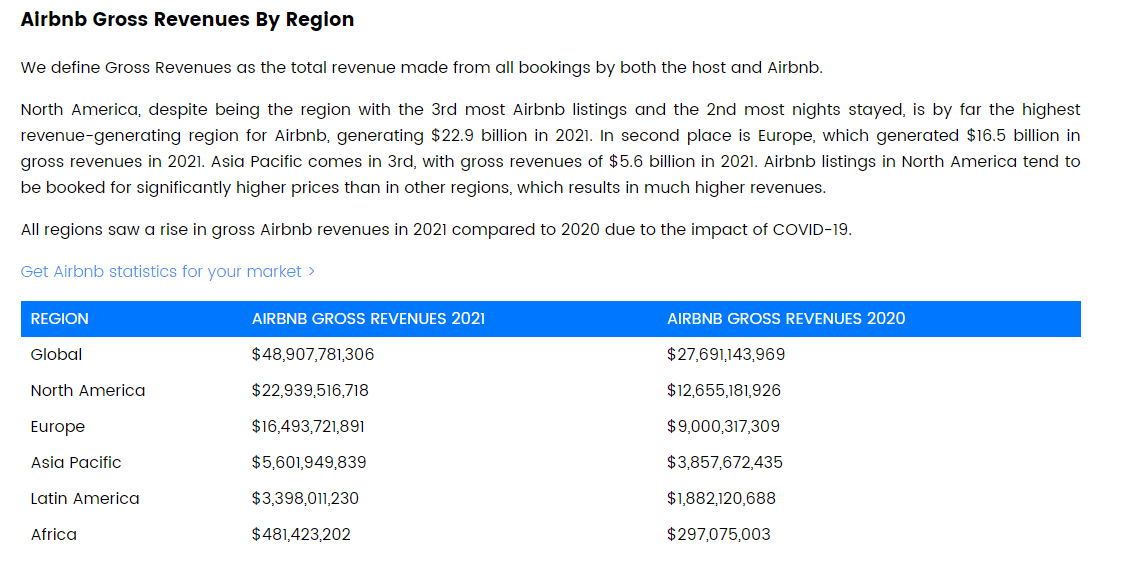

The aggregated International segment needs to be looked at further, for that we’ll take a look at data from AllTheRooms, a data analytics company for short rentals. AllTheRooms uses gross revenues, which include revenues for the hosts and Airbnb. We can see that Europe accounts for 1/3 of Airbnb’s gross revenues and likely also its total revenues, slightly up around 1% compared to 2020.

Airbnb gross revenues by region (all the rooms)

European energy crisis

According to ABC NEWS, the Eurozone is seeing never before seen inflation since the introduction of the Euro. 19 countries reported inflation above 10%, with Energy being the main contributor at a 40.8% YoY increase! Food, alcohol and tobacco also pushed inflation higher at 11.8%. These are not signs of good discretionary spending for the Eurozone. In the last year, we saw a lot of pent-up demand from people who were locked down for over a year without the possibility to travel and go on vacation. This pent-up demand won’t last forever though and at this point, most people probably already had a vacation.

When I talk to fellow Europeans right now, the topic of conversation is much more likely to sound like “We turned down the heating again because we can’t afford to heat the kitchen anymore” than “Have you booked your tickets for our vacation to Paris yet?”.

Bookings from EMEA have declined over the last quarters from 20% growth in Q1 to 11% growth in Q2 and I expect it to flip negative in the remainder of the year due to these headwinds, at least for new bookings.

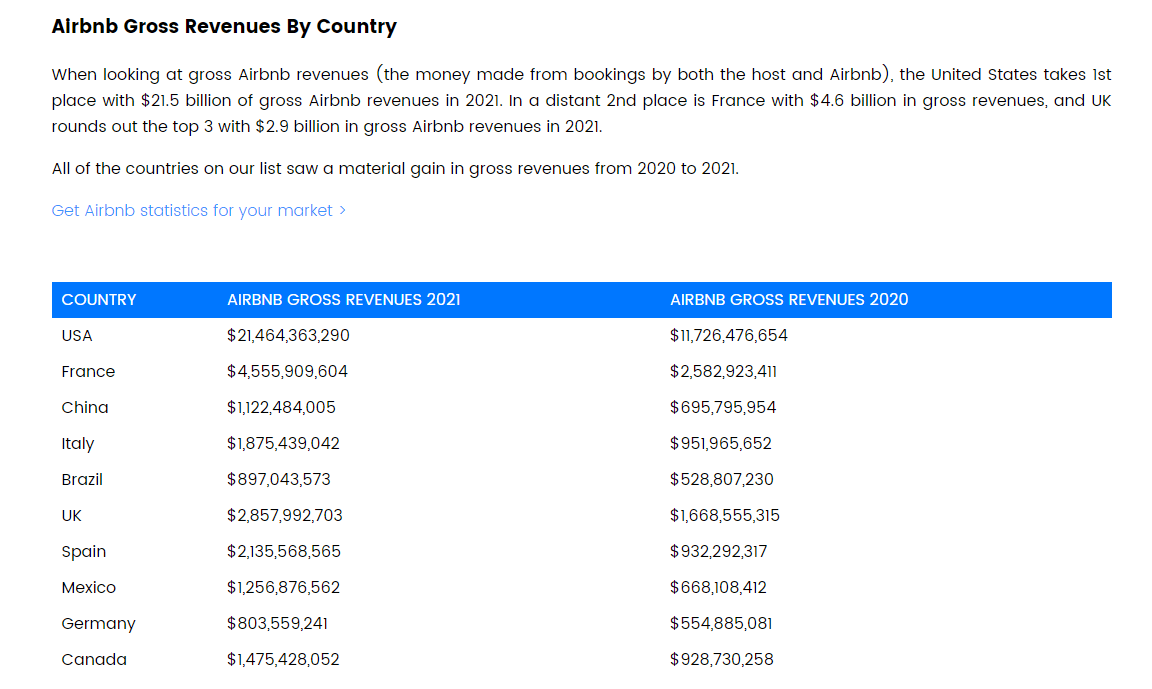

Retreat from the Chinese market

In May Airbnb announced that it will close its domestic China business. Long term this is a good move, but short term it will add another tailwind to revenues amidst the slowing growth of the company. China generated around 2.3% of Airbnb’s gross revenues in 2021 and is a hard market to penetrate for international companies. National companies like Meituan have an easier time in China. A comment from a recent 10K filling:

We will continue to incur significant expenses to operate our business in China, and we may never achieve profitability or sizable supply penetration in that market.

Few things to note: This only refers to the domestic Chinese market, the larger opportunity is Chinese tourists’ international travel, which still is a long-term opportunity for Airbnb. Currently Chinese is experiencing widespread lockdowns because of its ‘Zero Covid’ policy. This limits Chinese international travel as well, another short-term headwind.

Airbnb gross revenue by country (All the rooms)

Is Airbnb over-earning?

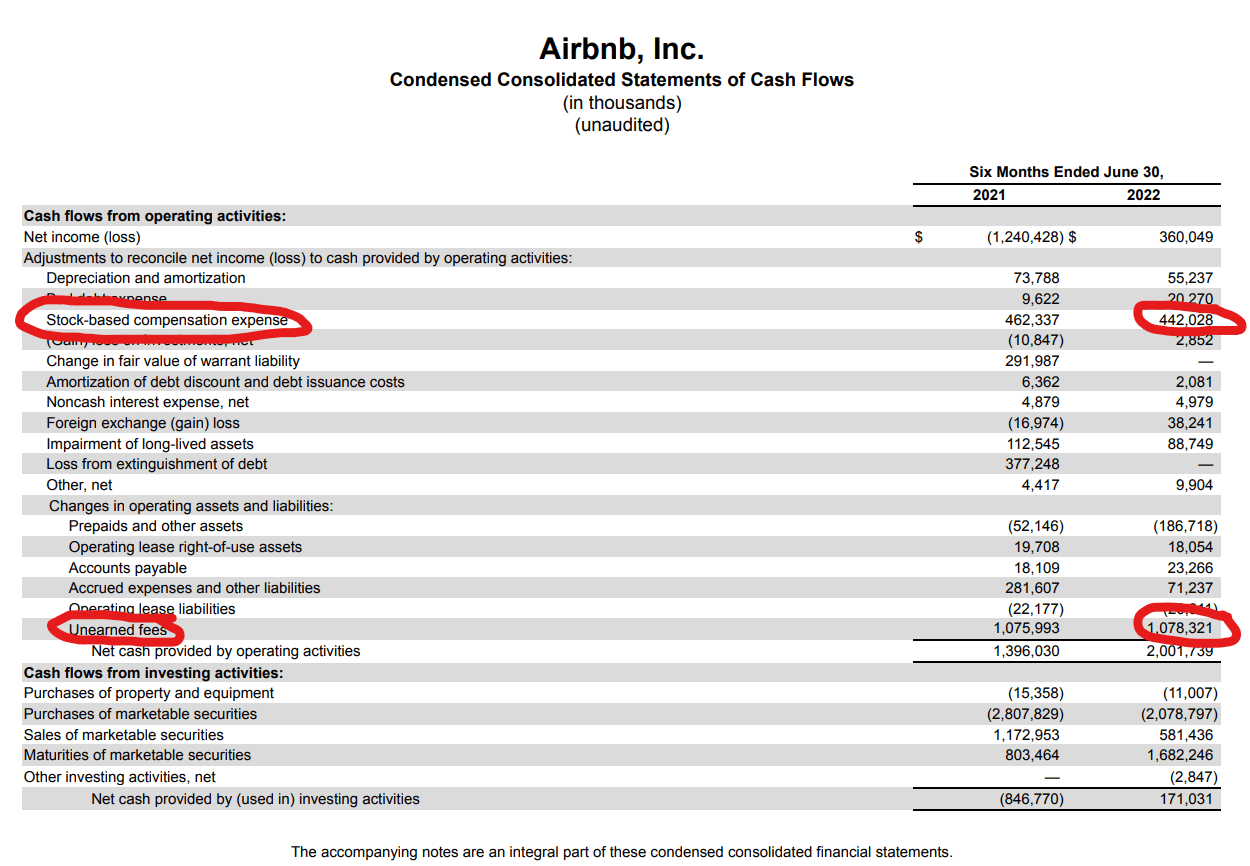

Airbnb is a high-margin business, being an online marketplace with high gross margins (81%) and without the need for expensive capital expenditures. The company has managed to generate $2.77 billion in Free Cash Flows (“FCF”) at a 37% FCF margin. This extremely high FCF margin begs the question of whether or not this is sustainable. If we take a look at the cash flow statement we can see that Airbnb actually was GAAP profitable in the six months that ended June 30 by $360 million, up from a loss of $1.2 billion in the prior year. This was primarily achieved by growing expenses much slower than revenues, the only costs that saw material increases were Sales and marketing and the Cost of revenues were in line with revenue growth. FCF is significantly higher at $2 billion, a difference of $1.64 billion. We can see that the majority of this difference ($1.5b) comes from stock-based compensation (SBC) and unearned fees. I personally am not a fan of including SBC in the FCF, because even though it is not a cash expense, it still is an expense for the shareholders, because they are getting diluted. Unearned fees are deferred revenues, where a guest books a stay and pays part of it upfront. These unearned fees get recognized as revenues once the guest actually stays in the Airbnb. The total outstanding unearned fees on the balance sheet are $1.98 billion, the majority of the $2.77 billion in FCF over the last 12 months. These unearned fees tremendously benefited from the pent-up demand of the last year and I think that in this recessionary environment revenue growth will fall further. Last quarter saw guidance coming in at 25% expected growth, significantly below the 60-70% growth rates over the last years. With Europe (1/3 of revenues) being in a big crisis and the cost of living rising everywhere in the world, I do not see significant growth for Airbnb in the short term.

Airbnb Cash flow statement (Airbnb 10Q)

Regulatory risks

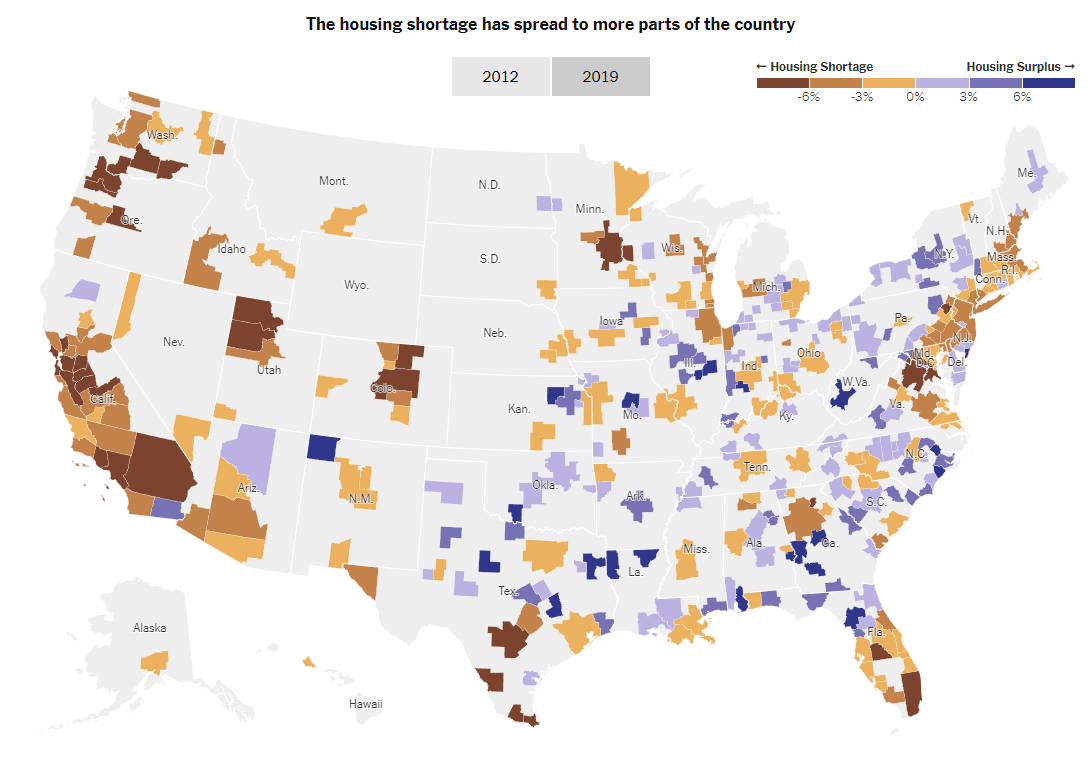

Another key risk is regulation. If we take a look at a map of the USA’s housing shortage and surplus we can see that most densely populated places have shortages of 6% and more. Airbnb and other short-term rentals intensify this shortage by occupying space for rentals that could be used for a family to stay in. This opens the risks for many regulations like they are already present in many cities around the world. Especially in a cost of living crisis with gas prices at all-time highs, I see this as a considerable risk for revenue growth.

USA housing shortage map (New York Times)

Valuation

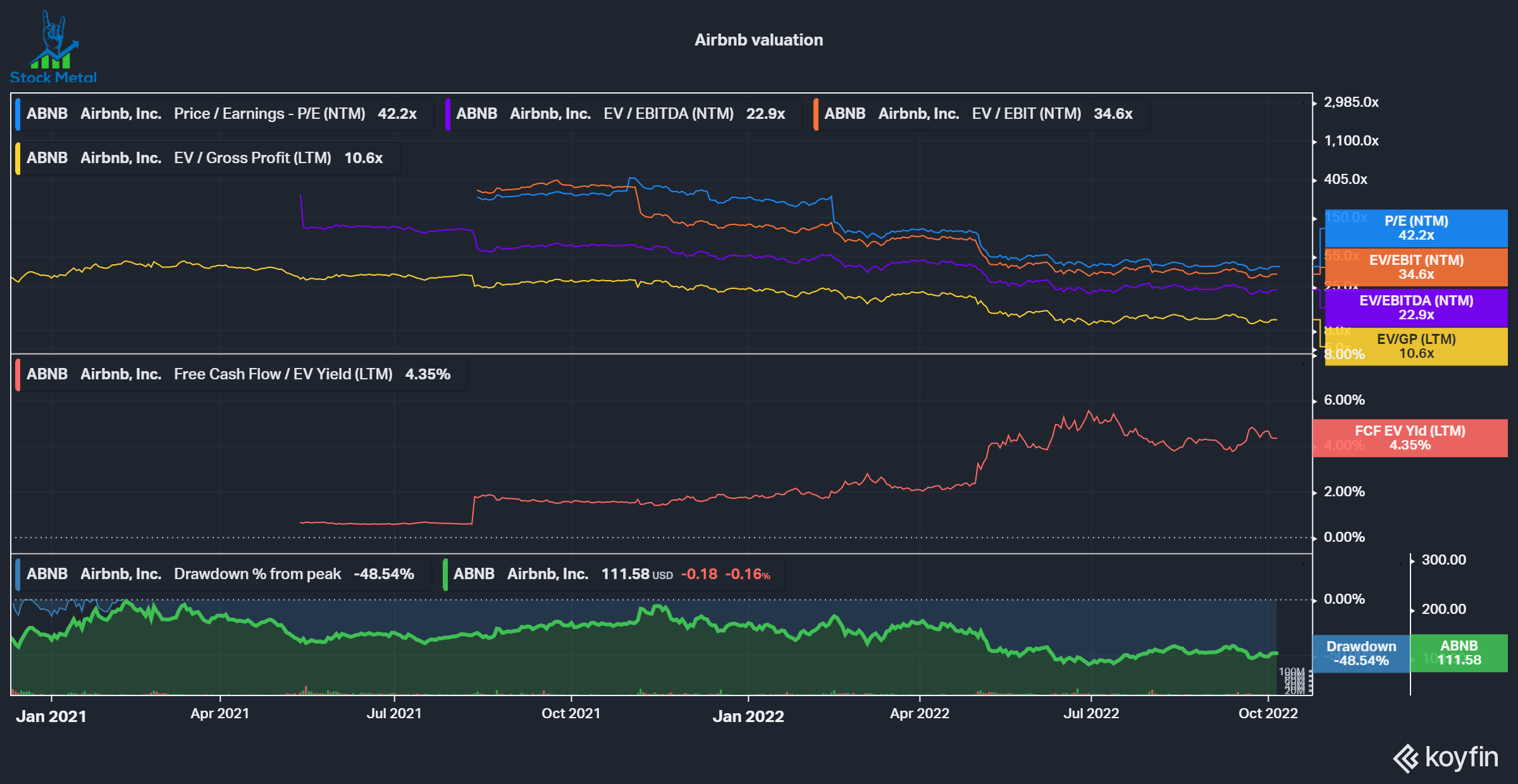

If we look at the valuation multiples for Airbnb we can see that the FCF yield has skyrocketed with the sharp increase in FCF, driven by unearned fees. At these levels, it would seem like a bargain, but as I mentioned previously in this article, I am not confident that these FCF levels are sustainable. On a PE and EV/EBITDA level we can see that the company still is elevated at 42 PE and 23 times EBITDA.

Airbnb valuation (Koyfin)

Risks to my thesis

My short-term sell thesis revolves around Airbnb underperforming in its next quarters, with flattening or even declining growth in Free Cash Flows due to over-earnings in the last year. If the consumer, especially in Europe, turns out to be stronger than I anticipate, then Airbnb might just continue to go up in price. Chinese lockdowns also are a headwind right now, but if the government decides to lift restrictions we could see a large pent-up demand from Chinese citizens who now want to travel again.

Of course, we also have the risk of a sudden change in FED policy, sending the entire market and with it, Airbnb higher.

Short-term bearish, long-term bullish

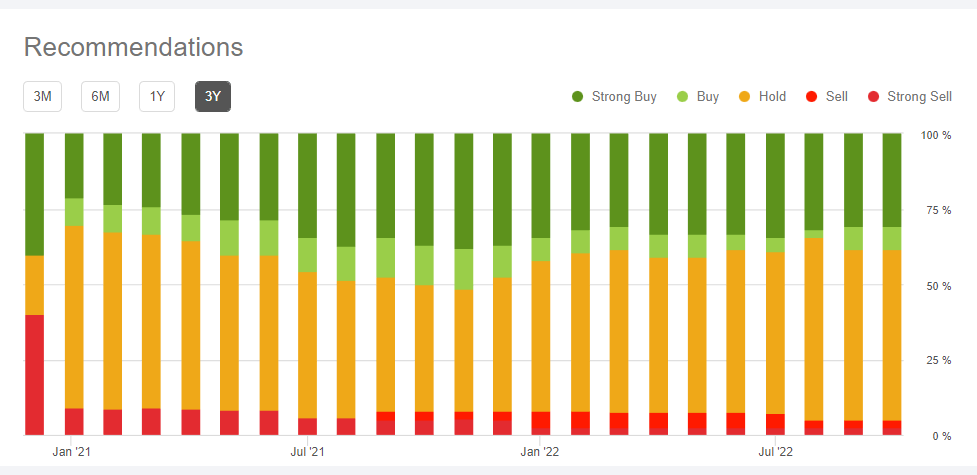

Analysts are still largely positive about Airbnb with an average rating of 3.61 (Buy) and an average price target of $138.59, I am not as optimistic in the short-term and can see the stock price falling under $100 again.

Analyst recommendations for ABNB (Seeking Alpha)

Although Airbnb is in a significant drawdown of 48% from ATH, I believe the stock has further to fall with previous tailwinds becoming potential headwinds in the near future. Let’s be clear, over the long term I do like Airbnb’s business. They created a new niche, pioneered it and became the household name for it. At these levels, I am not a fan of the stock though, but I’ll consider the stock if we see a further correction and the execution stays strong. The company showed great scalability over the last year with margins increasing significantly, driven by slow-growing operating expenses, it will be interesting to see how they perform if business slows down.

Editor’s Note: This article was submitted as part of Seeking Alpha’s best contrarian investment competition which runs through October 10. With cash prizes and a chance to chat with the CEO, this competition – open to all contributors – is not one you want to miss. Click here to find out more and submit your article today!

Be the first to comment