CatLane

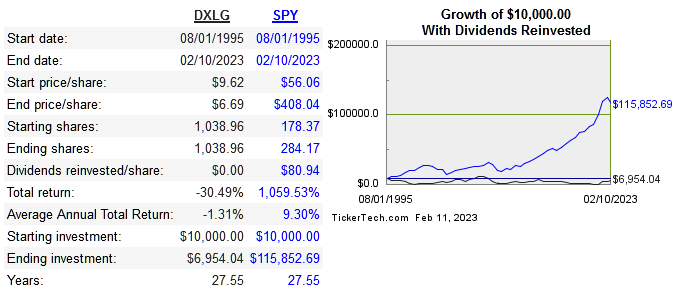

Destination XL Group Inc (NASDAQ:DXLG) is an American apparel retailer that specializes in plus size men’s clothing. They currently operate 287 stores throughout 46 states. It was founded in 1976 and has been publicly traded since 1987. Below is the long term share price performance:

dividendchannel

The market cap peaked in 1993 and the stock has underperformed greatly since then. The global industry is estimated to grow at 4.8% till the end of the decade. The company estimates they can open another 50 new stores over the next few years. Below is the return on capital and earnings metrics:

|

Company |

Revenue 10-Year CAGR |

Median ROE 10 year |

Median ROIC 10-Year |

EPS |

FCF/Share |

|

DXLG |

2.5% |

-12.9% |

-7.3% |

-0.7% |

16.1% |

|

CURV* |

12% |

-15.5% |

2.9% |

n/a |

n/a |

|

-1.4% |

6.1% |

6.1% |

n/a |

n/a |

|

|

4.5% |

7% |

6.7% |

n/a |

n/a |

*3-year

The company is in good financial shape and currently has record high revenue and earnings.

Capital Allocation

The company pays no dividend and has never made significant repurchases, although it currently has approval to spend up to $15 million on repurchases. They’ve also done very little in the way of acquisitions. They have no debt and $23 million in cash balance.

Risk

In this case there are a few numbers that stand out in defining the quality of this business. First, the operating margin is very inconsistent and volatile. Unless I’m looking at a fast growing company, operating profit needs to be stable for me to consider it a long term investment. DXLR has never had more than six consecutive years of making an operating profit, and even when there was a profit, it’s never been very high until recently. I can forgive a lot of fluctuation of net income so long as I’m getting more stability with operating margins and free cash flow. This is absolutely not the case with DXLR.

Second we see that retained earnings are actually negative $83 million. Buffett’s rule for retained earnings makes perfect sense and it can tell you a lot about the history of a business. This rule basically states that a good company should be able to create at least one dollar in market value for every dollar of retained earnings over the long term. So to see negative retained earnings for such a mature, long-running business, this is a sign that they can’t successfully reinvest their profits.

The only way this investment works is for the company to be legitimately turning around and staying that way. I see this as a low probability outcome given the track record.

Valuation

The share price of this company has been on a wild ride even before the pandemic. At the end of 2020, shares got as low as $0.19, only to shoot up to $8.43 one year later. Only six months later, shares were down to $3.42, and since then have now basically doubled. The 5-year monthly beta is 1.46 and I anticipate it getting higher. Below is the price multiples comp:

|

Company |

EV/Sales |

EV/EBITDA |

EV/FCF |

P/B |

|

DXLG |

0.7 |

5.3 |

12.6 |

3.3 |

|

CURV |

0.5 |

3.3 |

24.4 |

-1.6 |

|

EXPR |

0.1 |

6.8 |

-2.3 |

-2.6 |

|

CITI |

0.2 |

4.9 |

3.7 |

1.7 |

Source: quickfs.net

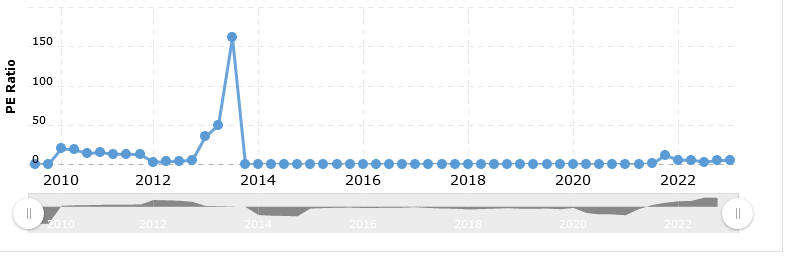

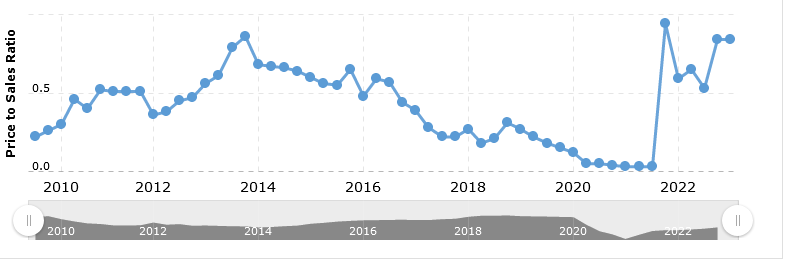

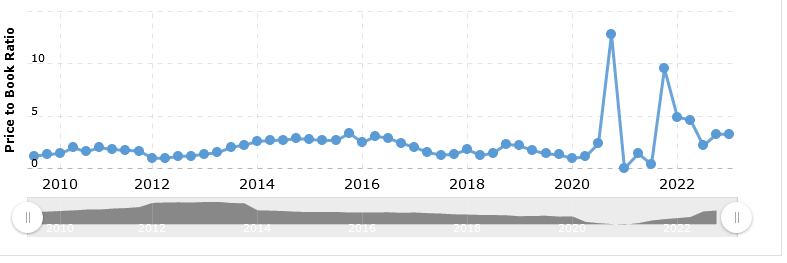

Things look optically cheap as far as multiples for DXLG as well as the peers. This means there is no real discount from a pricing perspective. Next is the historical look at multiples for DXLG:

macrotrends

macrotrends

macrotrends

I actually won’t be using a DCF model for this stock, because I don’t expect them to remain profitable 5+ years from now. Keep in mind that revenue and margins are at all time highs, and they will probably normalize over time. To expect otherwise would mean the company has hit an inflection point and has essentially upgraded in quality.

Conclusion

DXLG can historically be considered a low quality business, but the current version is actually in good financial shape. Revenue and margins are at all time highs, and they have no debt and no history of diluting to raise money. The problem is that the company has a track record of inconsistent profitability, especially at the operating level. I expect mean reversion to bring returns on capital and margins back down.

Even though the multiples are low, they aren’t obviously discounted when compared with peers. This stock is volatile and any potential shareholder needs to be aware of the ride that this stock can take them on. As a long term investor searching for a growth business at a decent price, I will be avoiding DXLG on primarily a fundamental basis.

Be the first to comment